Check out this week’s Danger Zone interview below with Chuck Jaffe of Money Life and MarketWatch.com.

With its much-hyped IPO last Friday, Box (BOX: $22/share) became the latest entrant into the highly competitive cloud computing and storage space. It’s easy to see why the company went public — it’s bleeding cash at an alarming rate and it needs more. Many investors are placing their bets that Box will supplant Dropbox as the preferred file and document storage service. However, these investors are ignoring the reality of Box’s industry and the danger of its current valuation.

What is Box?

Box offers online file sharing and management services primarily for businesses, but also individuals. The company offers 10 gigabytes of free storage and charges monthly for additional storage. Box also offers a service called OpenBox that links content stored on Box to popular online web applications and services like Twitter, Google Apps, and FedEx. Companies using Box include Proctor and Gamble (PG), Aeropostale (ARO), Emory University and Pandora (P).

How Does it Look on Paper?

If you’re asking how this company looks on paper, the short answer is: not great.

In 2014 Box earned an after-tax operating loss (NOPAT) of -$156 million, worse than the -$108 million the year before. This loss gives Box a return on invested capital (ROIC) of -100%. In other words, for every dollar invested into its business, the Box burns another dollar. Not exactly an encouraging sign for shareholders.

Box has generated some impressive revenue growth over the past several years. In 2013, the company experienced full-year revenue growth of 140%, and 111% growth in 2014. Box’s free cash flow in 2014 was -$126 million, an outflow worth 54% of the company’s pre-IPO assets.

How Does Box Stack Up to the Competition?

So far, Box does not look like a good investment based on its current profitability..But its stock may be a good buy if we can see how the company creates a moat for itself and elevates itself above the competition.

Unfortunately, it’s difficult to see how Box is differentiating itself in the crowded and competitive cloud storage and management sector. Box has some features common to Dropbox, like its free storage options, and some to Google (GOOGL) Drive, like its collaboration tools. Box’s enterprise focus mirrors that of Microsoft’s (MSFT) OneDrive. Privately held Dropbox claims about 300 million users, while Google Drive claims 240 million and OneDrive over 250 million. These user numbers dwarf Box’s 32 million.

What Box claims to do is offer the widest array of options and customization to suit business’ needs. However, this is subjective, and on comparable metrics such as storage space, pricing, supported software integration, and file size limits, there is no clear winner amongst the most popular offerings listed above.

Several competitors, like Google Drive and Microsoft OneDrive, offer comparable storage space, file size, and integration options at less than half the price of Box’s offering. With their vast resources and profitable core businesses, Google and Microsoft have no problem taking lower margins on their cloud storage operations to eat up Box’s market.

Why Doesn’t Revenue Growth Matter?

As is the case with many high-flying cloud software companies, investors in BOX are looking at the company’s extraordinary revenue growth to support the stock’s valuation. This is fine for the time being, but recent trends show that revenue growth is slowing dramatically: growth has dropped from 140% growth year over year in fiscal 2013 to 80% for the first nine months of 2014.

This growth is coming at great cost for Box, as sales and marketing expenses equaled 99% of revenues in the first nine months of 2014. The fact that Box is burning all of its income on acquiring new customers illustrates the extreme uphill battle this company must fight to win over business from its larger, more established competition. Keep in mind that this company already has 32 million users across 44,000 paying organizations, but is still spending a disproportionate amount on sales and marketing.

You May Have Missed These Red Flags

There are a few small concerns that do not materially impact our thesis but that you may want to know about nonetheless. Box has $65 million outstanding employee stock option liabilities and $60 million in total debt, which includes $24 million in off-balance sheet debt. This $125 million total equates to 5% of Box’s current valuation.

How Box Can Justify its Valuation

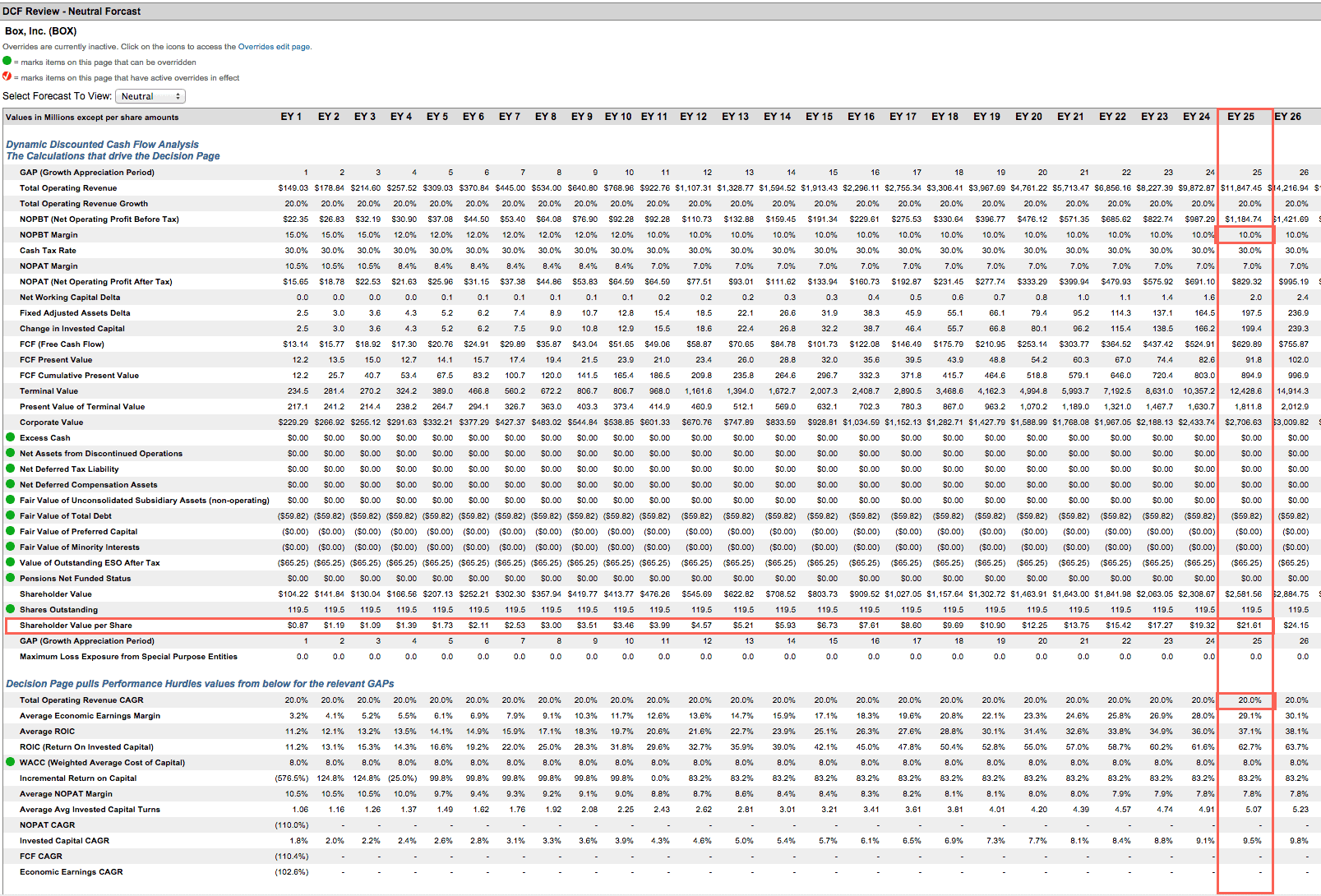

To justify its current valuation of $22/share, Box must increase its pre-tax margins to 10% (from their current level of -127%) and grow revenue by 20% compounded annually for the next 25 years. Under this scenario, Box would be earning an average ROIC of 37%, greater than that of Google, Amazon and IBM. There is no reason to make such a risky bet on this company with so many other good tech companies out there.

{kind=link}

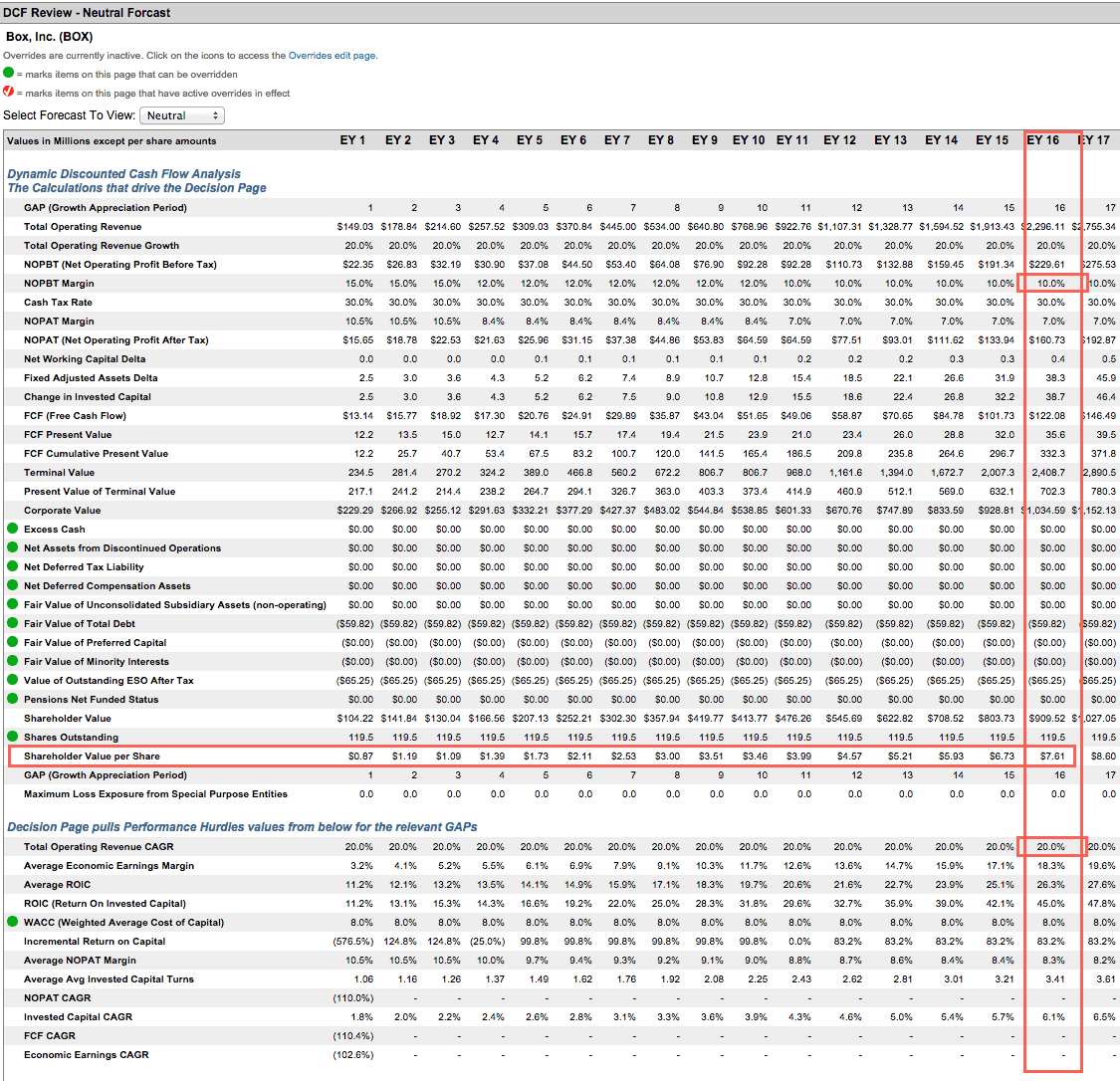

Let’s lower our expectations a bit. If Box can increase its margins to 10% and grow revenue by 20% compounded annually for the next 16 years, the company is worth less than $8/share, a 65% downside.

{kind=link}

Box’s industry has a low barrier to entry, and just about every large tech company is dipping their toes into this water. The problem with this scenario is that Box’s valuation would imply incredibly high barriers to entry, as indicated by the high ROICs and sustained revenue growth in the above scenarios.

In many ways, Box’s IPO reminds us of the tech bubble. Capital is cheaper than ever in the current interest rate environment, and this company’s IPO is an example of how reckless some investors can be when capital is this free-flowing.

Catalyst is Coming This Year

During the tech bubble, there was a practice known as “IPO flipping.” Financial institutions, which received the lion’s share of IPO allocations, would sell when they felt like the stock had run its course. The unloading of all of these shares into the open market creates a demand-supply imbalance, and share prices fall. There are new rules limiting how quickly institutions can dump their shares, but this still appears to be a likely catalyst for BOX.

In addition, as soon as there is more transparency about when interest rates will rise, there will be a substantial decline in interest in BOX shares as money becomes more expensive.

Low Likelihood of Acquisition, Buyback, or Dividend

It’s possible that any of Box’s large competitors, such as Google, Microsoft, or IBM, will acquire it. This seems unlikely at the moment and probably would have happened before Box went public and valuations soared. Any potential buyers will surely wait for a drop in the company’s price before making a bid.

As the company has no excess cash, we feel that there is little risk of Box instituting an irresponsible dividend or buyback at this point in time.

Short Interest and Insider Transactions

There is no short interest or insider transaction data available at this time.

Disclosure: David Trainer and André Rouillard receive no compensation to write about any specific stock, sector, or theme.

Click here to download a PDF of this report.

Photo credit: TechCrunch