In the wake of 3Q16, Netflix (NFLX) is up nearly 20%. Is this price reaction justified? Have investors gotten too caught up in the “membership beat” or recently lowered expectations? Who’s paying attention to core issues like cash flow and competitive advantage? One thing is for sure; this jump in stock price only exacerbates the already high risk in the stock’s valuation.

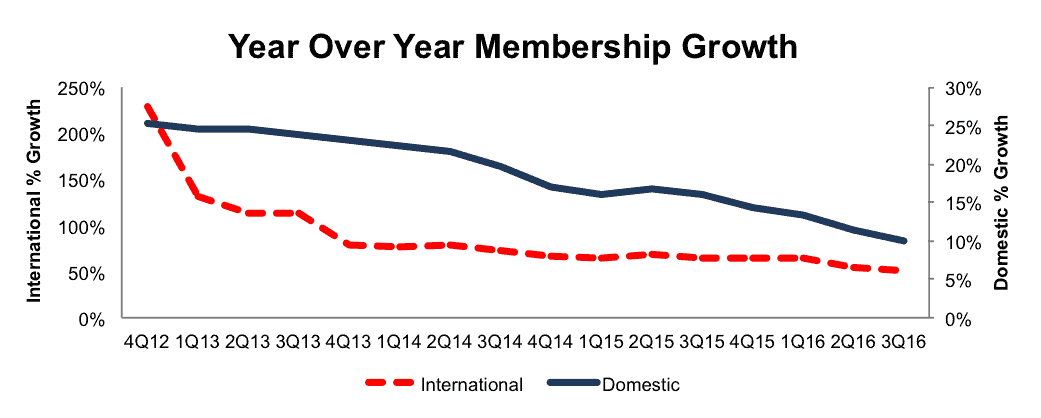

Membership Growth Continues Downward Trend

The headlines immediately after the earnings release centered on Netflix soaring past membership growth estimates. However, this “beat” was largely the product of lowered expectations post 2Q16. In July, Netflix guided for 2.3 million membership additions in 3Q16, which was well below consensus estimates of 3.5 million.

Fast-forward to 3Q16 and Netflix announced 3.6 million member additions, soaring past its lowered guidance but barely surpassing initial consensus expectations. Furthermore, this quarter’s membership growth continues a long-term decline in the year-over-year (YoY) membership growth rate.

Per Figure 1, international members grew 51% YoY in 3Q16, down from 64% in 3Q15 and 72% in 3Q14. Similarly, domestic members grew 10% YoY in 3Q16, down from 16% in 3Q15 and 20% in 3Q14. It’s clear that Netflix’s membership growth rate is slowing, which only makes it harder to justify the stock’s lofty expectations.

Figure 1: Netflix’s Membership Growth Rates

Sources: New Constructs, LLC and company filings.

The “membership beat” was attributed to stronger than expected acquisition impact due to Netflix’s original content. We’ve argued before that the firm’s focus on original content has it operating more like a traditional TV network and 3Q16 only affirms as much. In fact, recent studies show Netflix’s selection of top rated movies has declined over the past two years as the firm increased investment in originals. Netflix cannot afford to maintain a large content library while investing large amounts of capital into originals.

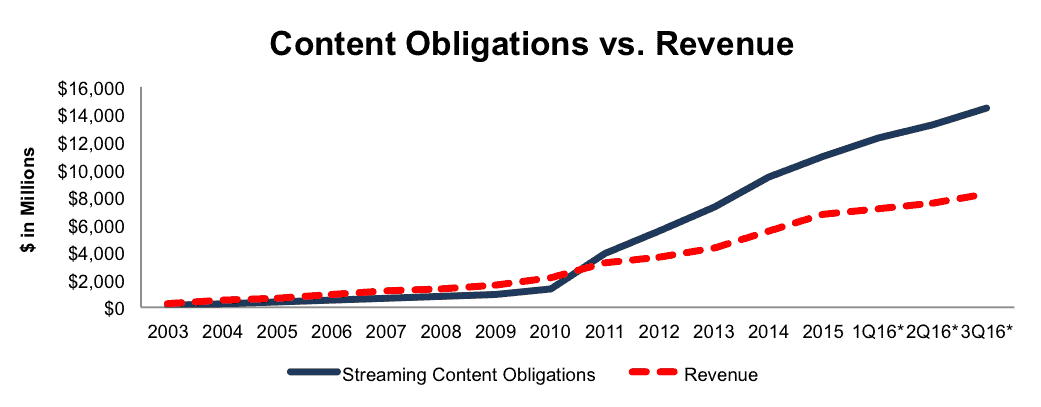

Content Costs Continues to Outpace Revenue Growth

The firms rising costs, coupled with its negative free cash flow (-$1.6 billion in 2015) are not a winning business strategy.

We’ve long warned about the alarming rate at which Netflix’s streaming content obligations are growing. With a stated goal of releasing more original content in 2017 than 2016, Netflix’s costly productions will continue to add to its already large content obligations. Since 2010, content obligations have grown 49% compounded annually while revenue has grown 25% compounded annually, per Figure 2. At the end of 3Q16, content obligations totaled $14.4 billion and have grown faster than revenue YoY in five of the past six years. It’s clear that competition has helped to bid up prices for licensed content, while Netflix’s large investment in originals keeps pushing content obligations higher.

Figure 2: Content Obligation Growth Outpaces Revenue

*Revenue from the trailing twelve months

Sources: New Constructs, LLC and company filings

With the increased costs of originals, it should come as no surprise that Netflix announced it expects to raise additional debt in the coming weeks.

Margins Are Worth Watching

When we first placed Netflix in the Danger Zone in November 2013, we noted that the company’s margins were facing pressure from the decline in DVD memberships (most profitable segment) and the exorbitant costs of expanding internationally. In 3Q16, Netflix’s international contribution margin was -8%, which means the international segment has been unprofitable for 19 consecutive quarters.

While the international segment has been inching closer to the breakeven point recently, it still falls well short of the expectations implied by the stock price.

NFLX Valuation Remains Unrealistically Optimistic

Investors’ willingness to overlook the firm’s fundamentals and focus on headline earnings beats has allowed NFLX to soar. However, without a meaningful improvement in the economics of the business, NFLX remains one of the most overvalued stocks in the market. Even if Netflix maintains pre-tax margins (3.6%) and can grow NOPAT by 22% compounded annually for the next decade, the stock is worth only $24/share today – an 80% downside.

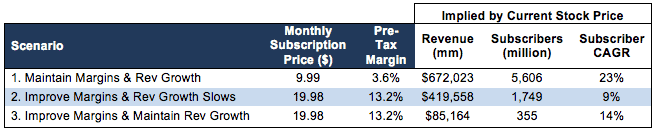

To further illustrate just how overvalued NFLX remains, we quantify three scenarios for the improvement in margins, subscribers, and/or revenue that is required to justify NFLX’s current price of $118/share. For reference, Netflix currently has just under 87 million members.

Scenario 1: If we assume that Netflix maintains its current price structure, its current pre-tax margins (3.6%), and can grow revenue by consensus estimates in EY1 & EY2 and by 26% thereafter (average of last five years), the company must grow NOPAT by 24% compounded annually for the next 20 years to justify its current price of $118/share. In this scenario, Netflix would generate $672 billion in revenue (20 years from now), which at current subscription prices implies the company’s user base will be 5.6 billion. The world population is estimated to be 7.4 billion.

Scenario 2: If we assume that Netflix adopts a strategy that improves margins by doubling prices but at the expense of revenue growth, the current expectations are still overly optimistic. If Netflix can increase pre-tax margins to 13.2% (highest in company history, 2010), and grow revenue by 13% (half the five year average), the company must grow NOPAT by 16% compounded annually for 34 years to justify its current price. In this scenario, Netflix would be generating over $419 billion in revenue 34 years from now, which at double current subscription prices implies the company’s user base will be 1.7 billion.

Scenario 3: Even if we assume Netflix is able to drastically improve margins through price increases without any impact on revenue growth, shares are still overvalued. If Netflix can achieve 13.2% pre-tax margins and grow revenue by consensus estimates in EY1 & EY2 and by 26% thereafter, the company must grow NOPAT by 38% compounded annually for the next 11 years to justify the current price. In this scenario, Netflix would generate over $85 billion in revenue 11 years from now, which at double current subscription prices implies the company’s user base will be 355 million.

Each of these scenarios also assumes Netflix is able to grow revenue and NOPAT without spending on working capital or fixed assets, an assumption that is unlikely, but allows us to create unquestionably optimistic scenarios. For reference, NFLX’s invested capital has grown on average $926 million (14% of 2015 revenue) per year over the last five years. No matter which way you look at this stock’s valuation, NFLX is priced beyond perfection. Given the litany of challenges facing the company, the downside risk to this stock looms large.

Figure 3 summarizes three potential scenarios for the profit growth needed to justify $118/share.

Figure 3: Valuation Scenarios for NFLX

Sources: New Constructs, LLC and company filings.

This article originally published here on October 18, 2016.

Disclosure: David Trainer, Kyle Guske II, Kyle Martone, and Sam McBride receive no compensation to write about any specific stock, sector, style, or theme.

Scottrade clients get a Free Gold Membership ($588/yr value). Login or open your Scottrade account & find us under Quotes & Research/Investor Tools.

1 Response to "Netflix: Look Past the Headline “Beat”"

David

Thorough analysis as always. NFLX is certainly defying traditional metrics. One reason might be that is simply the limited float and high short interest. The other reason could be its discounting a strategic acquisition. The ATT-TWX speculation might have fueled some of the move yesterday. With a EV of $55B not including the off-balance sheet debt it seems way to rich for what it is. Another factor might be the model evolves into something more than just movie delivery.