Netflix (NFLX: $325/share) stock dropped 11% on Thursday, July 18 after the company reported its lowest quarterly subscriber growth numbers in three years, and its first domestic subscriber loss since 2011. These disappointing subscriber numbers show that Netflix’s investment in original content has failed to deliver the sustainable competitive advantage required to justify its valuation. The loss of licensed content, increased competition, and higher prices in the future mean investors should expect more disappointing subscriber numbers going forward.

We think the stock will fall dramatically farther as more investors realize the company has no chance of coming close to achieving the future cash flows baked into $325/share.

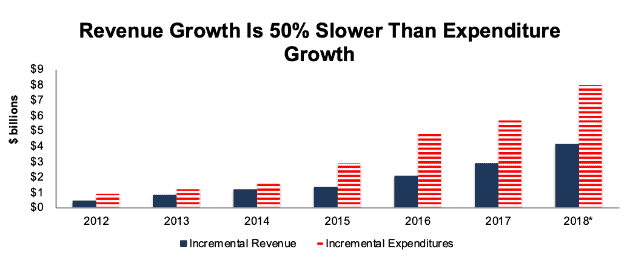

Huge New Content Spending Not Adding Enough Subscribers

Netflix spent $13 billion on content last year, with 85% of new spending earmarked for originals. For that much money, they should be more than just “on track” to have originals be the majority of viewing in every category. The company acknowledged in the most recent quarter that its original content hasn’t driven enough growth. From the Q2 2019 investor letter:

“We think Q2’s content slate drove less growth in paid net adds than we anticipated.”

Rather than acknowledge the limitations of their strategy, however, Netflix appears determined to throw more money at the problem. Netflix hasn’t given a specific content budget for 2019, but they expect content costs to continue growing at a similar trajectory, which would put the company on pace to spend $17.5 billion this year. As Figure 1 shows, Netflix’s revenues are not growing fast enough to cover its rising expenses.

Figure 1: Subscriber Growth Is Not Enough to Cover New Content Spending

Sources: New Constructs, LLC and company filings.

As a result of rising content costs, Netflix has been forced to raise its prices, which only serves to make the upcoming streaming services from Disney, Warner Media, and NBC Universal more viable. The company noted that subscriber growth missed forecasts by a larger amount in regions with price increases, so it’s clear that higher prices are already impacting subscriber numbers.

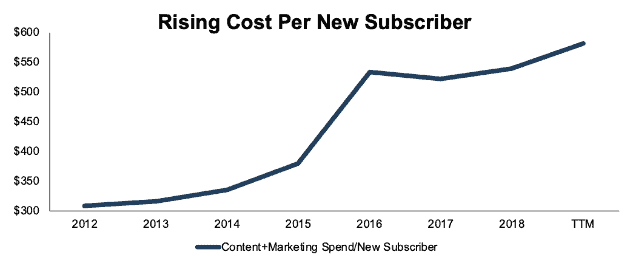

Figure 2 shows that Netflix’s cost to acquire new subscribers continues to rise. In 2012, the company spent $308 on marketing and additions to streaming content for each new subscriber. By 2018, that number rose to $539, an increase of 10% compounded annually. After Q2 2019, the cost to acquire a new subscriber is up to $581 TTM.

Figure 2: Content and Marketing Spending Per New Subscriber: 2012-TTM

Sources: New Constructs, LLC and company filings.

For a user paying the standard price of $13/month in the US, it takes almost 4 years to pay back that acquisition cost. Given that Netflix’s subscriber growth is now coming solely from international markets, where prices are lower, the payback period will be even longer for most new subscribers.

This trend is undoubtedly the wrong direction for Netflix. The firm’s content strategy causes it to lose more money and grow subscribers at a slower rate. It seems that it is only a matter of time before investors lose patience with Netflix’s egregious cash burn when it is not translating into progress toward eventual profitability.

To maintain credibility, Netflix management needs to tell us how, exactly, it will make money. Enough with the number of Instagram followers. Give investors something tangible that creates confidence that there’s a chance future profits can match or exceed the expectations baked into the current valuation of the stock. Otherwise, it is time to sell the stock.

Still Reliant on Licensed Content – Which It Is Losing

Ever since Netflix launched its first original series with House of Cards in 2013, the streaming service has put its original content front and center. Executives cherry pick impressive stats for their originals (without giving access to comprehensive viewing data), and their quarterly reports regularly feature charts showing the Instagram followers of young actors launched to fame through Netflix originals.

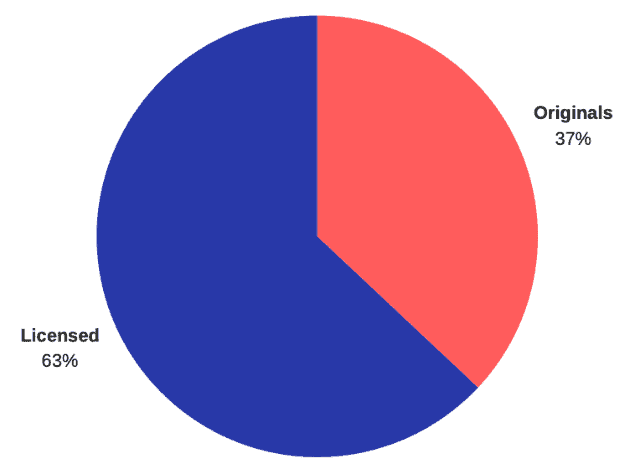

Given all this emphasis on originals, it might come as a surprise that licensed content accounts for nearly 2/3 of viewing hours on Netflix. Despite spending billions of dollars on original content, Netflix still relies heavily on classic shows like The Office, Friends, and Grey’s Anatomy.

Figure 3: Licensed Content Use Dominates Original

Source: 7Park Data

As legacy media companies pull these shows to launch their own streaming services, Netflix could lose much of its value to consumers just as the competition heats up.

What Happens When It Loses Shows That Drive Majority of Viewing Hours?

Netflix maintains that the company won’t face significant blowback from the upcoming loss of licensed content. From the company’s 2Q 2019 investor letter:

“From what we’ve seen in the past when we drop strong catalog content (Starz and Epix with Sony, Disney, and Paramount films, or 2nd run series from Fox, for example) our members shift over to enjoying our other great content.”

However, the content that Netflix has lost in the past doesn’t compare to the titles they’re about to lose. As Figure 4 shows, licensed content from companies that will soon launch their own streaming services represent 3 of the top 4 streaming series on Netflix for November 2018.

Figure 4: Most Streamed Shows on Netflix in the U.S. for November 2018

Source: 7Park Data

Netflix reportedly paid $100 million to keep Friends on its service for 2019, more than triple its previous licensing fee of $30 million. While that’s a hefty price tag, Figure 4 shows just how critical the classic sitcom is to Netflix’s subscriber base. Even though it’s been off the air almost 15 years, it still gets watched more than the vast majority of Netflix’s new releases.

Unfortunately for Netflix, it can’t keep Friends forever. Warner Media – now a part of AT&T (T) – plans to launch HBO Max in 2020, where Friends will stream exclusively. Disney (DIS), which owns Grey’s Anatomy, will also launch its streaming service in 2019, while NBC Universal (CMCSA) announced it will remove The Office from Netflix in 2021.

What happens to Netflix when it loses the shows that drive the majority of its viewing hours? Not only do licensed shows account for 63% of viewing hours, as recently as 2017 over 40% of Netflix subscribers in the U.S. almost exclusively watched licensed content. Even if that number has been cut in half over the past year, that still leaves 1 in 5 domestic Netflix subscribers (almost 12 million people) that almost never engage with the roughly 700 original TV shows the company produced last year.

In fact, the sheer number of Netflix originals might be making the licensed content problem even worse. Research suggests that when consumers are presented with an overwhelming array of content, they tend to retreat to the programs that are most familiar to them.

This tendency represents a big problem for Netflix. Outside of Stranger Things, the streaming service doesn’t have any tentpole franchises with widespread name recognition and appeal. Netflix’s lack of recognizable, familiar content will put it at a disadvantage to Disney+ and other new streaming services with extensive back catalogs of classic movies and TV shows.

If Netflix is already losing subscribers in the US now, how does it expect to maintain its user numbers going forward as the competition increases significantly?

Spending More Money Won’t Make the Licensed Content Problem Go Away

Even though Netflix was early to recognize the risk of media competitors pulling their licensed content the company now seems reluctant to acknowledge that its original content strategy has not solved the problem. On the company’s 4Q 2018 earnings call, Chief Content Officer Ted Sarandos said:

“The vast majority of the content that is watched on Netflix are our original content brands.”

As the statistics we cited above show, this answer is simply untrue. Sure enough, CEO Reed Hastings quickly stepped in to correct Sarandos, clarifying:

“In unscripted (i.e. reality TV) now, it’s our first category, where a majority of the viewing is a branded original, in the other categories we’re climbing, not yet at a majority, but on track for it.”

Netflix is already losing subscribers domestically and seeing slower growth internationally due to its price hikes. Now, it’s about to lose some of its most valuable content and face several formidable new challengers. It’s hard to see how the company maintains the growth and profitability necessary to justify its valuation.

Figure 5: Subscriber Growth Is Slowing Down

Sources: Netflix 2Q 2019 Shareholder Letter

At its current valuation, Netflix can’t afford a further slowdown in subscriber growth. As our reverse DCF model shows, Netflix needs to reach ~500 million subscribers (roughly triple its current count) to justify its valuation. In order to hit that target, the company would need to maintain its 2018 growth (~30 million new subscribers) for the next 12 years. Given that its subscriber additions are already declining (see Figure 5), this scenario seems unlikely.

The negative reaction to this earnings report shows that the market is finally starting to understand the limitations of Netflix’s business model and the unrealistic expectations implied by its valuation.

This article originally published on July 18, 2019.

Disclosure: David Trainer, Sam McBride and Kyle Guske II receive no compensation to write about any specific stock, sector, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

Click here to download a PDF of this report.

Photo Credit: Tim Reckmann (Flickr)