Our Most Attractive and Most Dangerous stocks for January were made available to the public at midnight on Wednesday. December saw some strong performances from our picks, led by small-cap KKR Financial Holdings (KFN), which gained 35%. On the Dangerous side, Sears (SHLD) declined by 12% while EcoLab (ECL), which was featured last month, was 1% in the red.

January sees 12 new stocks on our Most Attractive list and 11 new stocks fall into the Most Dangerous category.

Our Most Attractive stocks have high and rising return on invested capital (ROIC) and low price to economic book value ratios. Most Dangerous stocks have misleading earnings and long growth appreciation periods implied in their market valuations.

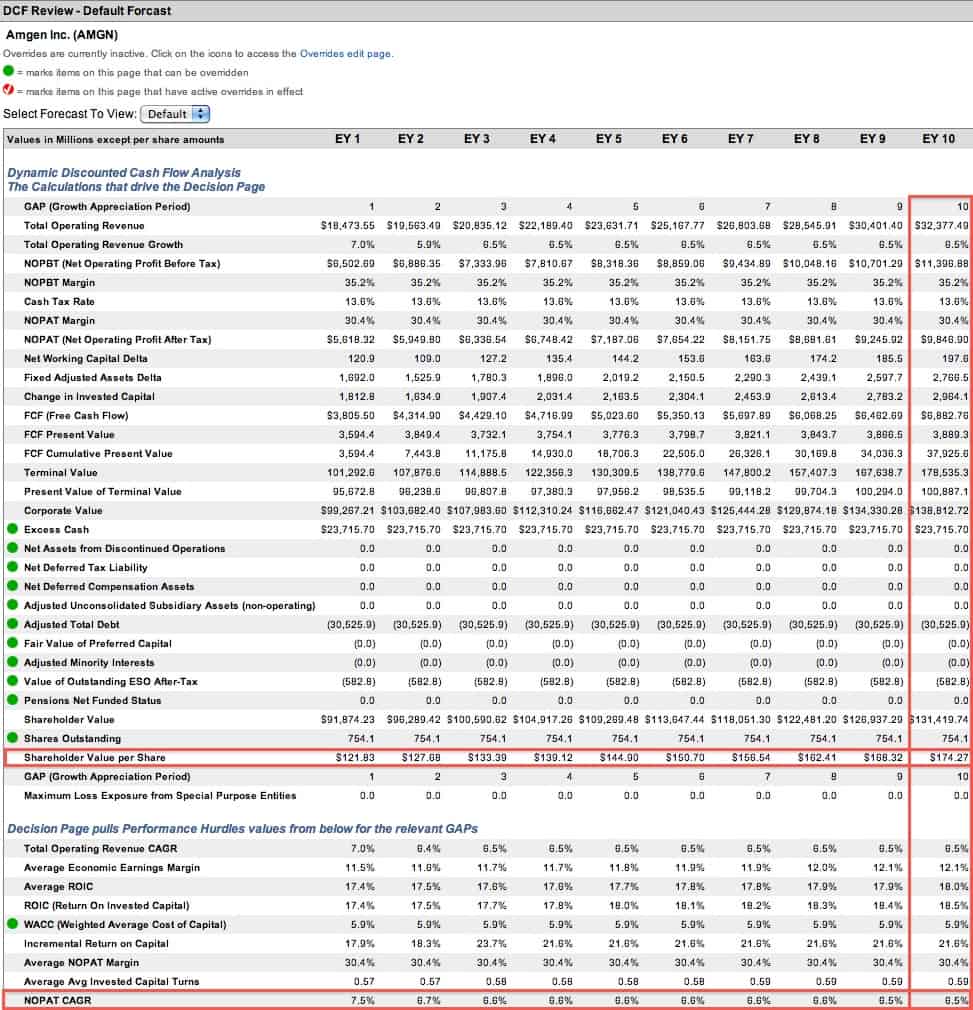

Most Attractive Stock Feature For January: AMGN

Amgen Inc. (AMGN) is one of the new additions to the Most Attractive list this month. AMGN makes the list due to the decrease in rank of other stocks that were ahead of it.

Cash is king, and few companies generate cash flow as effectively and consistently as AMGN. Over the past five years, the company has had a free cash flow of at least $3 billion every year with an average free cash flow yield of 8%.

Investors should also look for a track record of growth, which AMGN definitely has. Over the past decade, AMGN has grown after-tax profit (NOPAT) by 14% compounded annually. Over that time frame the biotech giant has earned a double-digit return on invested capital (ROIC) in every year but one.

Although AMGN spent $10 billion on acquiring Onyx Pharmaceuticals this year, the company still has plenty of cash left with which to fund further research and acquisitions. Some analysts have raised concerns over AMGN’s growth potential going forward, but given the company’s track record it’s hard to believe that growth will come to a complete halt. More importantly, AMGN is such a great value at the moment that very little growth is required to justify the current stock price.

At its current valuation of $117/share, AMGN has a price to economic book value ratio of only 1.1. Currently, the market is predicting that AMGN will grow NOPAT by no more than 10% from its 2012 level for the remainder of its corporate life. Analysts currently expect AMGN to top 10% growth when its annual report comes out in February, so the market’s expectation seems to be overly pessimistic.

Even with moderate growth, AMGN has significant potential upside. If we give AMGN credit for 6.5% NOPAT growth compounded annually for the next 10 years, the stock is worth ~$175/share today. That high potential upside combined with low downside risk makes AMGN one of our Most Attractive stocks this month.

{kind=link}

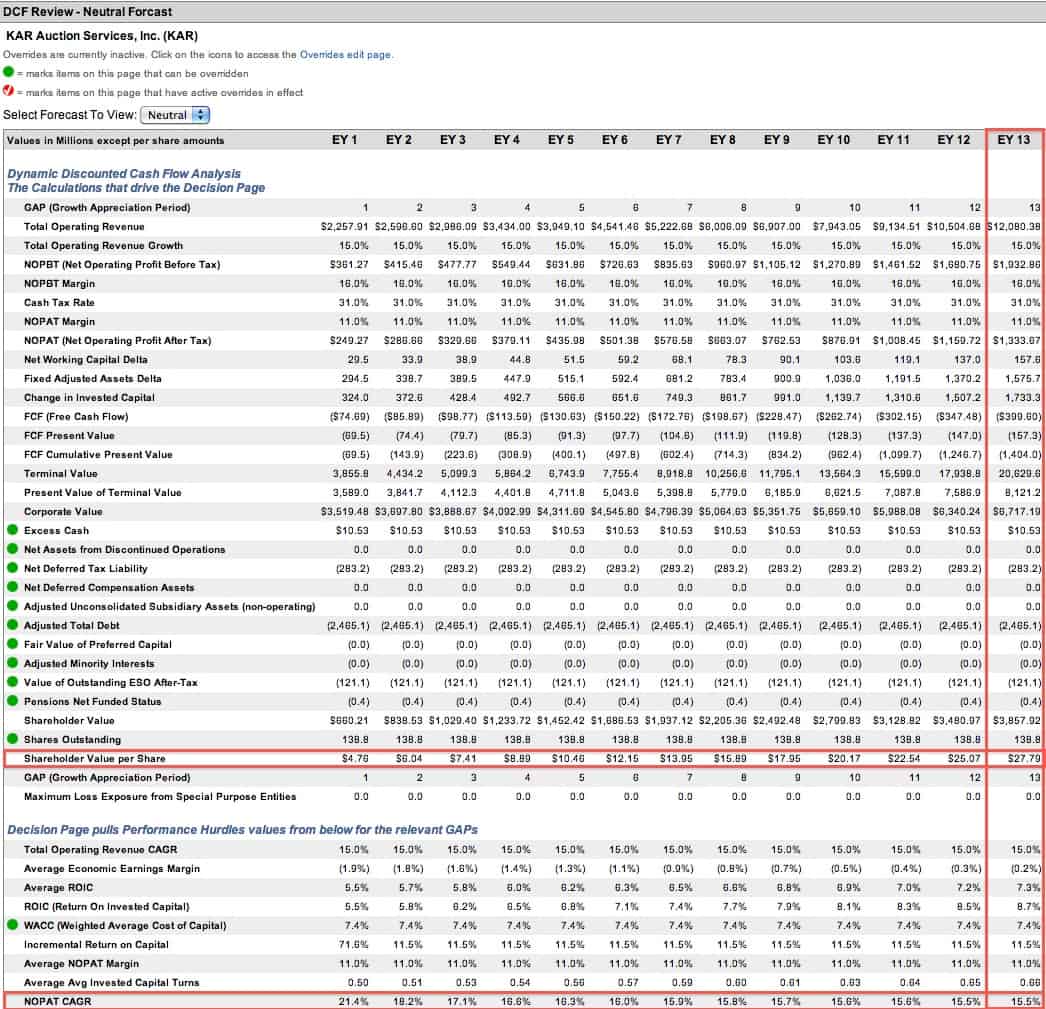

Most Dangerous Stock Feature For January: KAR

KAR Auction Services (KAR) is one of the new additions to the Most Dangerous list this month. KAR increased by 8% in December, which took it from being merely overvalued to being expensive enough to be one of our Most Dangerous stocks.

Operationally, KAR offers little for investors to get excited about. In the four years since its IPO, the highest ROIC KAR has earned was 6% in 2011, which still fell well short of its weighted average cost of capital (WACC) of 8%.

From 2010 to 2012, KAR’s NOPAT declined by a total of 8%. That trend appears to be reversing in 2013 as the used car market recovers, but the fluctuating nature of its profitability should be a concern for investors.

Another concern for investors should be the debt that KAR carries both on and off its balance sheet. KAR has $2.5 billion in adjusted total debt, which includes $600 million in off-balance sheet debt from operating leases. While KAR’s debt is not significant enough to hamper its ability to operate, it does subtract from the value to shareholders. KAR’s debt, along with smaller employee stock option and deferred tax liabilities, push its economic book value (or no-growth value) below $0. In other words, without major profit growth, KAR’s equity value is zero. Given its stock is nearly $30/share, dangerously high expectations are built into its valuation.

Specifically, KAR’s current valuation of ~$29/share implies that it will grow NOPAT by 16% compounded annually for 13 years. I’m not sure that even the most ardent bull would make the argument that KAR, or any used car business, is going to grow that rapidly for such a long time.

{kind=link}

I don’t see any apparent downside catalysts for KAR at the current moment, but due to its expensive valuation I expect it to lag the market and plunge rapidly on any bad news. Meanwhile, any upside from a growing used car sales market is already priced into the stock.

The Most Dangerous Stocks report for January can be purchased here, while the Most Attractive Stocks can be purchased here. To gain access to these reports one week earlier each month, e-mail us at subscriptions@newconstructs.com to request a subscription.

Sam McBride contributed to this report.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.