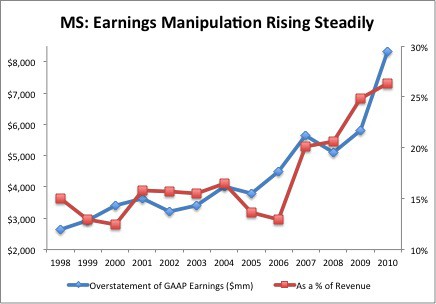

[…] There are many ways that companies can manipulate accounting rules to overstate their earnings, but there is only one place to find out how they do it: the financial footnotes. Nowhere on Morgan Stanley’s income statement do you see that they included $821 million in unusual and non-recurring income in their operating earnings. Nowhere on their balance sheet do you see that the company carries over $5.4 billion in off-balance sheet debt. For more details on how we determine Morgan Stanley’s true earnings, click here. […]

[…] There are many ways that companies can manipulate accounting rules to overstate earnings, but there is only one place to find out how they do it: the financial footnotes. For example, nowhere on Morgan Stanley’s income statement do you see that the company included $821 million in unusual and non-recurring income in its operating earnings. Nowhere on the balance sheet do you see that the company carries more than $5.4 billion in off-balance sheet debt. For more details on how we determine Morgan Stanley’s true earnings, click here. […]

[…] and Morgan Stanley (MS – dangerous rating). Click here for my recent article on C and here for the article on MS. As noted above, there are a number of attractive-or-better-rated stocks […]

Add Morgan Stanley to the list of firms benefiting from SFAS No. 159 in 3Q11. All but two cents of their $1.15 EPS in 3Q11 came from SFAS No. !59.

And the stock is up on the strong quarterly earnings?

What?

Richard Shaw

April 30, 2013

I know this was written a while ago, but it looks like Morgan Stanley is currently overbought.

5 replies to "Sell Morgan Stanley Before It Sells You Down the River"

[…] There are many ways that companies can manipulate accounting rules to overstate their earnings, but there is only one place to find out how they do it: the financial footnotes. Nowhere on Morgan Stanley’s income statement do you see that they included $821 million in unusual and non-recurring income in their operating earnings. Nowhere on their balance sheet do you see that the company carries over $5.4 billion in off-balance sheet debt. For more details on how we determine Morgan Stanley’s true earnings, click here. […]

[…] There are many ways that companies can manipulate accounting rules to overstate earnings, but there is only one place to find out how they do it: the financial footnotes. For example, nowhere on Morgan Stanley’s income statement do you see that the company included $821 million in unusual and non-recurring income in its operating earnings. Nowhere on the balance sheet do you see that the company carries more than $5.4 billion in off-balance sheet debt. For more details on how we determine Morgan Stanley’s true earnings, click here. […]

[…] and Morgan Stanley (MS – dangerous rating). Click here for my recent article on C and here for the article on MS. As noted above, there are a number of attractive-or-better-rated stocks […]

Add Morgan Stanley to the list of firms benefiting from SFAS No. 159 in 3Q11. All but two cents of their $1.15 EPS in 3Q11 came from SFAS No. !59.

And the stock is up on the strong quarterly earnings?

What?

I know this was written a while ago, but it looks like Morgan Stanley is currently overbought.

http://www.tradersdirect.com/stocks/11347/morgan_stanley/