June 23, 20250CommentsDon’t Be Misled by Flawed MetricsThe only way to truly understand the health of the underlying business of a company is to go through the footnotes in the filings. by Hakan Salt, Associate Investment Analyst

May 29, 20250CommentsWhy Footnotes Are More Important Than You ThinkData in the financial statements is most meaningful when you consider the information in the footnotes. by Hakan Salt, Associate Investment Analyst

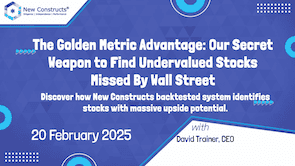

February 21, 20250CommentsThe Golden Metric Advantage: Our Secret Weapon to Find Undervalued Stocks Missed by Wall StreetThere’s a truth about investing that most people overlook. by Kyle Guske II, Senior Investment Analyst, MBA

October 24, 20240CommentsHow to Profit From Expectations InvestingFor over two decades, our research has been digging into financial statements, uncovering metrics that most investors overlook. by Kyle Guske II, Senior Investment Analyst, MBA

September 20, 20240CommentsICYMI: Long Idea Updates, New Danger Zone, New Discovery to Supercharge our Ratings, David’s Latest E-letter & Model Portfolio UpdatesHere's what happened at New Constructs during the week of September 16, 2024. by Kyle Guske II, Senior Investment Analyst, MBA

September 19, 20240CommentsThe Hidden Metric To Find the Best Stocks No One Knows AboutThere's a hidden metric that can reveal the best stocks in the stock market… by Kyle Guske II, Senior Investment Analyst, MBA

September 12, 20240CommentsSector & Industry Fundamentals 2Q24 UpdateWe’ve published an update to our Sector & Industry fundamentals page with 2Q24 data. by Kyle Guske II, Senior Investment Analyst, MBA

September 6, 20240CommentsAll Cap Index & Sectors: Economic Earnings Update For 2Q24 (Free, Abridged)This report is an abridged and free version of All Cap Index & Sectors: Economic Earnings Update For 2Q24. by Kyle Guske II, Senior Investment Analyst, MBA

September 6, 20240CommentsAll Cap Index & Sectors: Economic Earnings Update For 2Q24This report analyzes the Economic Earnings and GAAP earnings of the NC 2000 and its sectors for 2Q24. by Kyle Guske II, Senior Investment Analyst, MBA

August 29, 20240CommentsS&P 500 Economic Earnings: Update For 2Q24 (Free, Abridged)This report is an abridged and free version of S&P 500 Economic Earnings: Update For 2Q24. by Kyle Guske II, Senior Investment Analyst, MBA

August 29, 20240CommentsS&P 500 Economic Earnings: Update For 2Q24This report analyzes the economic earnings and GAAP earnings for the S&P 500 and its sectors through 2Q24. by Kyle Guske II, Senior Investment Analyst, MBA

July 18, 20240CommentsThe Trump Trade No One Is Talking AboutThe Trump Trade that no one else is talking about sees the market losing the liquidity boost that’s driven it up so much the last several years. by David Trainer, Founder & CEO

June 20, 20240CommentsSector & Industry Fundamentals 1Q24 UpdateWe’ve published an update to our Sector & Industry fundamentals page with 1Q24 data. by Kyle Guske II, Senior Investment Analyst, MBA

June 14, 20240CommentsICYMI: All Cap Index & Sector Fundamental Trends, Let’s Talk Long Ideas Webinar-June 20th, New Featured Stocks, Model Portfolio Performance & Model Portfolio UpdatesHere's what's happening at New Constructs. by Hakan Salt, Associate Investment Analyst

June 13, 20240CommentsAll Cap Index & Sectors: Economic Earnings Update For 1Q24 (Free, Abridged)This report is an abridged and free version of All Cap Index & Sectors: Economic Earnings Update For 1Q24. by Hakan Salt, Associate Investment Analyst

June 13, 20240CommentsAll Cap Index & Sectors: Economic Earnings Update For 1Q24This report analyzes the Economic Earnings and GAAP earnings of the NC 2000 and its sectors for 1Q24. by Kyle Guske II, Senior Investment Analyst, MBA

June 5, 20240CommentsS&P 500 Economic Earnings: Update For 1Q24 (Free, Abridged)This report is an abridged and free version of S&P 500 Economic Earnings: Update For 1Q24. by Kyle Guske II, Senior Investment Analyst, MBA

June 5, 20240CommentsS&P 500 Economic Earnings: Update For 1Q24This report analyzes the economic earnings and GAAP earnings for the S&P 500 and its sectors through 1Q24. by Kyle Guske II, Senior Investment Analyst, MBA

March 7, 20240CommentsThe Secret Metric To Find Hidden Gems in the Stock MarketThe truth is, there's a hidden metric that most investors completely overlook. by Kyle Guske II, Senior Investment Analyst, MBA

December 8, 20230CommentsSector & Industry Fundamentals 3Q23 UpdateWe’ve published an update to our Sector & Industry fundamentals page with 3Q23 data. by Hakan Salt, Associate Investment Analyst