Do you ever wonder how disconnected a stock’s valuation can possibly get from the fundamentals of the underlying business?

That question is hard to answer with traditional valuation tools and ratios. But, answering that question is exactly what our reverse discounted cash flow (DCF) model allows us to do for the thousands of stocks we cover.

During a recent Earnings Recap session, we reviewed Affirm (AFRM: $62/share) and did a deep dive into its valuation. The results were shocking. Rarely will you see a stock with a valuation so disconnected from the fundamentals of the business. Let’s get specific

Expectations Investing Analysis on AFRM

As we do for all of our Reverse DCF Case Studies, we use our valuation models to quantify the future performance of the company required to justify its current stock price.

Specifically, our model shows that to justify ~$62/share Affirm would have to:

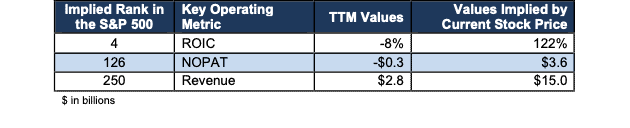

- grow revenue at 26.3% compounded annually for 8 years while also

- improving its return on invested capital (ROIC) from -8% to 122% and

- improving its net operating profit after tax (NOPAT) from $0.3 billion to $3.6 billion.

Let’s put some context around those expectations.

Benchmarking Expectations for AFRM

First, growing revenue at 26.3% CAGR for 8 years means Affirm’s revenue would be $15 billion in 2033. While also growing revenue at a rapid pace, the stock price implies Affirm will also increase its ROIC and NOPAT to very high levels. See Figure 1 for details.

Figure 1: Ranking Affirm’s Expected Cash Flows to the S&P 500

Sources: New Constructs, LLC and company filings.

As we discuss in our latest reverse DCF case study video, we think there are several reasons why the expectations embedded in Affirm’s current stock price are too high.

Competitive Realities

Large revenue growth, like what’s embedded in Affirm’s stock price, implies significant market share gains. We note that market share gains are typically won with lower prices, which are not possible with a company that must also increase its ROIC and NOPAT to very high levels.

In other words, Affirm’s stock price is implying a doubly-incredible future where the company enjoys huge revenue growth and NOPAT and ROIC improvement as well.

Where to Find Good Stocks

We’re not here just to warn you about the bad stocks, we’re here to help you find good ones, too. We provide our proven-superior ratings on over 3,300 stocks. Unlike Wall Street, where 95% of the stocks get a Buy or Hold Rating, less than 15% of our stocks get an Attractive or Very Attractive Rating. We work hard to provide the best fundamental research in the world. We’re constantly providing free training and stock picks to help investors make more money and invest with peace of mind.

Figure 2: How To Find The Right Stocks: The Robo-Analyst Rating System

Sources: New Constructs, LLC and company filings.

We think the MOMO, YOLO, SPAC, NFT, meme stock and meme coin trading ploys are bad for investors, bad for our stock market, and bad for our country. We’re here to give you proven-superior investment research that is good for the long-term health of your portfolio and your peace of mind.

More Expectations Investing Case Studies

Too few investors have the tools to unveil the details behind stock valuations. We make it clear and easy. Math is math. It’s not supposed to be hard. Wall Street wants to keep you in the dark by making you think it is too hard to get the truth about valuation.

We shed light into the dark corners of the market and make them into opportunities to profit.

If you enjoyed seeing what we show for Affirm’s real cash flows as well as the future revenue expectations baked into the stock price, you’ll love our other reverse DCF case studies.

If you’re interested in seeing more examples of how our DCF model works, I recommend checking out the Reverse DCF Case Studies here in our Online Community. To join our Online Community, complete this form.

Our community is free to join as is access to the Reverse DCF case studies.

How To Avoid the Landmines

Whenever stocks get super expensive, it is only a matter of time before they fall back to earth as the law of competition inevitably proves the expectations for future cash flows to be overly optimistic.

We have multiple Model Portfolios, including our Zombie Stocks list, to warn investors of stocks to avoid and alert them to stocks that get our Attractive rating. We also provide best-in-class ratings for stocks, ETFs, and mutual funds.

We hope you enjoy this research. Feel free to share with friends and colleagues!

This article was originally published on February 27, 2025.

Disclosure: David Trainer, Kyle Guske II, and Hakan Salt receive no compensation to write about any specific stock, sector, style, or theme.

Questions on this report or others? Join our online community and connect with us directly.