Some sort of fiduciary rule is coming. Whether it comes from the Department of Labor, the SEC, the CFP Board or individual state regulators, advisors need to be prepared to show they are unequivocally acting in the best interests of clients.

While plenty of attention has been paid to fulfilling the Duty of Loyalty, there is no official guidance on how to fulfill the Duty of Care or how to prove there is adequate diligence to support investment recommendations.

Despite the lack of regulatory guidance for fulfillment of the Duty of Care, there is plenty of common-sense guidance from thought leaders such as wealthmanagement.com, MarketWatch, Michael Kitces and Kim O’Brien, CEO of Americans for Annuity Protection. They all agree that research that fulfills the Duty of Care should be:

- Comprehensive: Incorporate all relevant publicly available data (e.g. 10-Ks and 10-Qs), including the footnotes and MD&A.

- Objective: Clients deserve unbiased research.

- Transparent: Client should be able to see how the analysis was performed and the data behind it.

- Relevant: There must be a tangible, quantifiable connection to stock, ETF or mutual-fund performance.

If one were to ask John Q. Public if he thinks the research behind the recommendations he gets should meet these standards, he’d say “yes”. He’d probably be shocked to learn that most research does not already meet these standards.

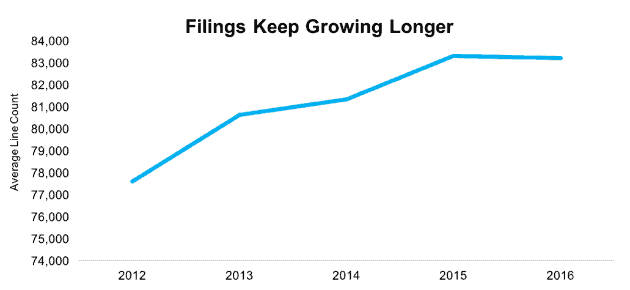

John Q. Public probably does not realize how difficult it is to produce research that meets these four standards with any kind of scale and consistency. 10-K and 10-Q filings are massive, dense documents with critical information buried deep in the financial footnotes. As Figure 1 shows, the average annual 10-K filing in 2016 contained over 83 thousand lines of text (or about 200 pages) and the length of filings just keeps growing.

Figure 1: Diligence Keeps Getting Harder

Sources: New Constructs, LLC and company filings.

That said, John Q. Public doesn’t want to hear hand-wringing over how difficult the job is. As long as it is possible, he deserves research that fulfills the Fiduciary Duty of Care.

What’s more, advisors deserve this quality of research too. In our meetings with advisors across the country, we consistently hear how worried they are about how to show regulators they’ve done their diligence. Advisors need to trust that the research on which they base their recommendations is of the highest standard so they can focus on their clients’ specific goals and needs.

Fortunately, as detailed in a recent white paper from Ernst & Young, emerging new technologies make it possible to deliver research that meets the four standards cost effectively and at scale.

Accordingly, the advisors who delay embracing fulfilment of the fiduciary duty of care risk losing market share to those that already have. For those that remain skeptical, we provide further explanation of each of the standards to underscore the self-evident nature of their importance to fulfillment of the Duty of Care.

- Comprehensive

It’s no secret[1] that corporate managers often exploit a large number of accounting loopholes to manipulate earnings per share (EPS). As a result, advisors have a fiduciary responsibility to analyze more than EPS. Only by reading through the financial footnotes and management discussion and analysis (MD&A) can advisors close accounting loopholes and assess the true profitability of a company.

Despite the importance of reading 10-K’s and 10-Q’s, many traditional research providers don’t do this work. One sell-side analyst even recently admitted he hadn’t realized that a bank he covered stopped filing reports with the SEC two months before. This lack of diligence is how you end up with 21 out of 23 sell-side analysts telling investors to buy or hold Valeant Pharmaceuticals (VRX) the day before it drops by 50%.

Research that meets the Duty of Care needs to account for all the information in financial filings. Research that does not take into account all the information from 10-K’s and 10-Q’s puts investors at undue risk.

Warren Buffett says he reads 500 pages of 10-K’s every day. Jim Chanos was able to spot the Enron fraud by looking at its 10-K’s and 10-Q’s. The most successful investors know that diligence matters.

- Objective

Can an investment recommendation truly be objective if it’s based on sell-side research that involves numerous conflicts of interest?

The same concerns apply to fund research, where the research providers are often paid largely by the funds they cover. Investors deserve truly unbiased research that is not influenced by relationships with the companies and funds under coverage.

- Transparent

Advisors need to prove to clients and regulators that they’re fulfilling fiduciary duties. Clients are in need of convincing as roughly two-thirds of investors don’t trust the financial services industry to act in their best interest.

Client education is the key for advisors to overcome this mistrust. Advisors who help clients understand their decision-making process and are open about the data and analysis behind their recommendations can reap long-term rewards. By getting clients more engaged in the process, advisors increase the probability of keeping clients committed to their investment plan through good times and bad.

Fiduciaries need to be transparent enough to back up their investment research and recommendations with key details and the assumptions that drive them in real-time, not just when a regulator asks about them.

- Relevant

Take a hypothetical advisor that reads every 10-K and 10-Q and then only buys stock in the companies with the highest proportion of the letter “e” in their filings. This process would be comprehensive, objective, and transparent, but it would not be relevant to long or short-term performance of the investment.

Without a tangible, relevant link to long and short-term performance, an investment process is incomplete. With all the focus on sentiment, technical research, macro themes and other pure trading strategies, fundamentals can be overlooked. Advisors and investors that ignore fundamental research are doing themselves a disservice, as research has found that even technical-based strategies can improve with the use of fundamental analysis.

Though fundamentals need not represent 100% of the driver for investment decisions, they should not be 0%. Fundamentals matter, and investing without proper analysis of them puts clients at undue risk.

This article originally published on October 25, 2017.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] In a 2015 survey, CFO’s said they believe 20% of companies intentionally misrepresent their earnings.

Click here to download a PDF of this report.

Photo Credit: Pixabay (Pexels)