This report is one of a series on the adjustments we make to convert GAAP data to economic earnings.

Reported assets don’t tell the whole story of the capital invested in a business. Accounting rules provide numerous loopholes that companies can exploit to hide balance sheet issues and obscure the true amount of capital invested in a business.

Converting GAAP data into economic earnings should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

We’ve performed unrivaled due diligence on 5,500 10-Ks every year for the past decade.

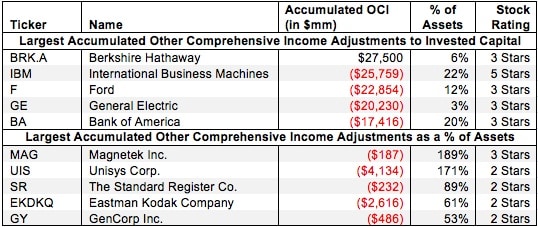

Accumulated other comprehensive income (OCI) are gains and losses that have yet to be recognized, and are excluded from net income. The accumulated OCI item usually appears as a separate line item on the statement of shareholder’s equity. When OCI charges can be recognized, they are removed from OCI, reported on the income statement and recorded in net income.

Most investors would never know that accumulated other comprehensive income distorts GAAP numbers by raising or lowering reported assets and, therefore, distorting assessment of a business’ ability to generate a return on that capital. Examples of items in OCI include: unrealized gains/losses on for-sale securities, derivatives and cash flow hedges; gains and losses from the translation of financial statements of foreign subsidiaries; actuarial gains and losses on benefit plans; and changes in a firm’s revaluation surplus. We remove OCI from our invested capital calculation to (1) better represent the actual capital on hand for management to generate a return on and (2) avoid the noise from the fluctuations of OCI.