This report presents the drivers[1] of economic earnings [return on invested capital (ROIC), NOPAT margin, invested capital turns, and weighted average cost of capital (WACC)] for our All Cap Index and each of its sectors. This research is based on the latest audited financial data, which is the 2020 10-K for most companies. Price data is as of 3/23/21.

The NC 2000 consists of the largest 2000 U.S. companies by market cap in our coverage. Constituents are updated on a quarterly basis (March 31, June 30, September 30, and December 31). We exclude companies that report under IFRS and non-U.S. ADR companies.

For reference, we analyze the Core Earnings for the entire NC 2000 and each sector in All Cap Index & Sectors: Core Earnings Vs. GAAP Net Income Through 4Q20.

These reports leverage more reliable fundamental data[2] that enables investors to overcome flaws with legacy fundamental datasets. Investors armed with our research enjoy a differentiated and more informed view of the fundamentals and valuations of companies and sectors.

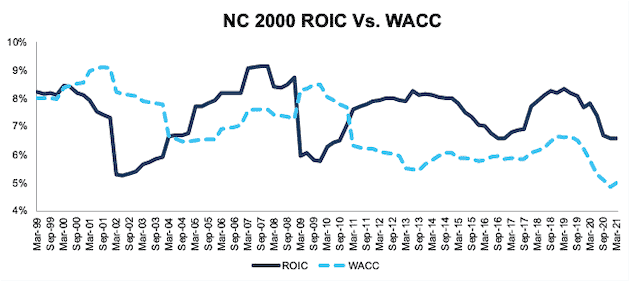

NC 2000 ROIC Falls Significantly in 2020

The NC 2000’s ROIC fell from 7.8% at the end of 2019 to 6.6% as of 3/23/21, the earliest date all NC 2000 companies provided 2020 annual data. See Figure 1. All NC 2000 sectors, except for the Technology and Consumer Non-cyclicals sectors, saw a drop in ROIC year-over-year (YoY) based on 2020 financial data, though some more than others, as we’ll show below.

Figure 1: ROIC and WACC for the NC 2000 From March 1999 – 3/23/21[3]

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period uses price data as of that date and incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

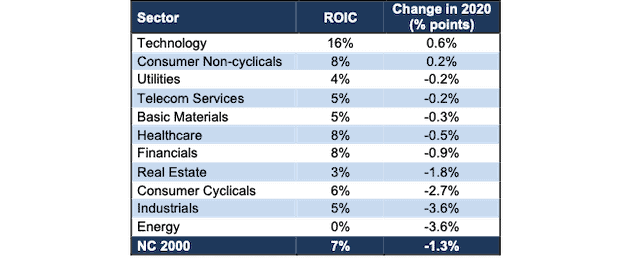

Ranking the NC 2000 Sectors by Change in ROIC

Figure 2 ranks all 11 NC 2000 sectors by the change in ROIC from the end of 2019 to 2020.

Figure 2: ROIC for All NC 2000 Sectors

Sources: New Constructs, LLC and company filings.

Financial data from 2020 10-Ks.

The Technology sector performed best through the COVID-19 pandemic, as measured by change in ROIC. This trend is not surprising given that the global shutdowns accelerated the enterprise and individual shift to cloud and other software solutions.

On the flip side, the Energy and Industrials sectors have the largest drop in ROIC from 2019 to 2020.

Overall, the Technology sector earns the highest ROIC of all sectors, by far, and the Energy sector earns the lowest ROIC.

Details on each of the NC 2000 Sectors

Figures 3-13 compare the ROIC and WACC trends for every sector since March 1999. Appendix I presents the current WACC for each sector.

Appendix II presents the drivers of ROIC: NOPAT margin and invested capital turns for each sector.

Appendix III presents additional ROIC analysis based on different weighting methodologies to adjust for the impact of a firm’s size on its sector and the NC 2000.

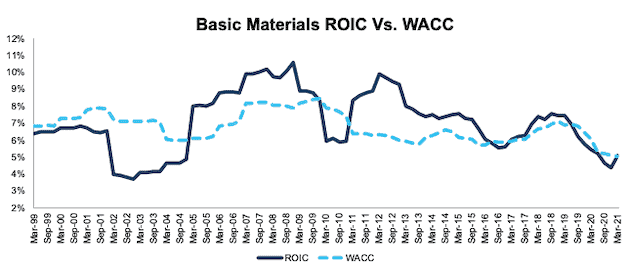

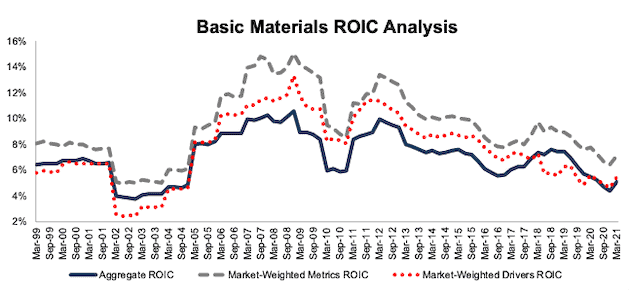

Basic Materials

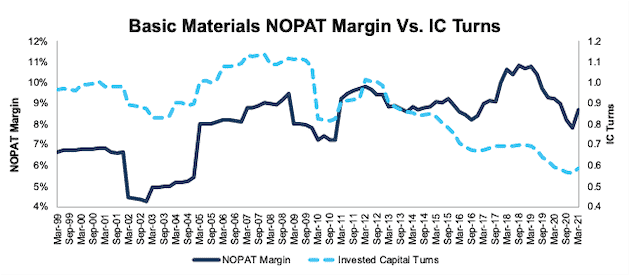

Figure 3 shows the ROIC for the Basic Materials sector has been in a long-term decline since ~2011 and fell 34 basis points YoY in 2020. Basic Materials sector NOPAT margin fell from 9.2% in 2019 to 8.7% in 2020 and invested capital turns were stagnant at 0.59 over the same time.

Figure 3: Basic Materials ROIC vs. WACC: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period uses price data as of that date and incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

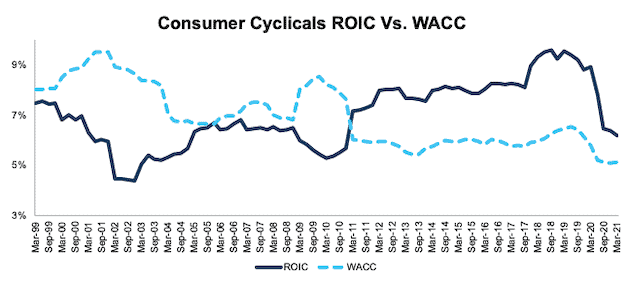

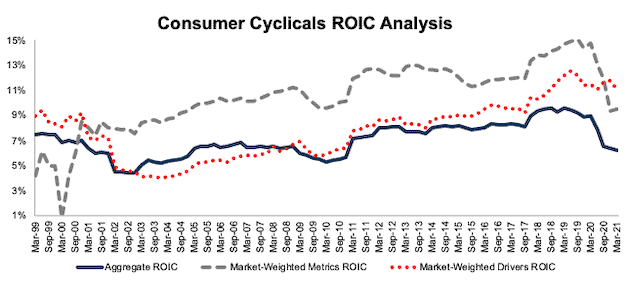

Consumer Cyclicals

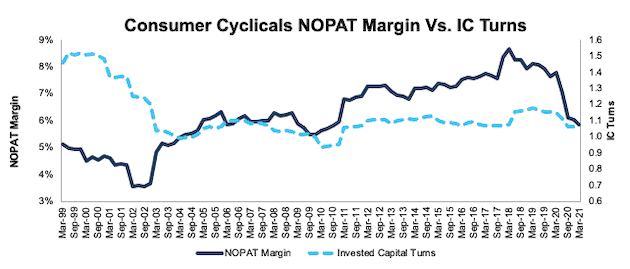

Figure 4 shows the ROIC for the Consumer Cyclicals sector was hit hard by the COVID-19 pandemic and, at 6.2% in 2020, fell to its lowest level since 2010. Consumer Cyclicals NOPAT margin fell from 7.8% in 2019 to 5.9% in 2020 and invested capital turns declined from 1.2 to 1.1 over the same time.

Figure 4: Consumer Cyclicals ROIC vs. WACC: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period uses price data as of that date and incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

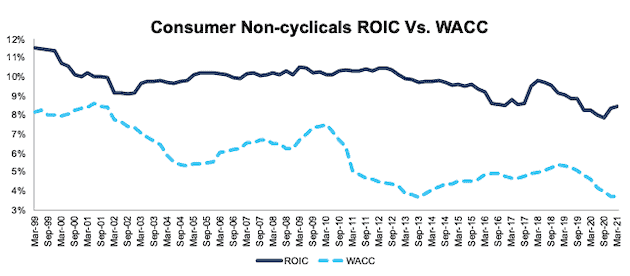

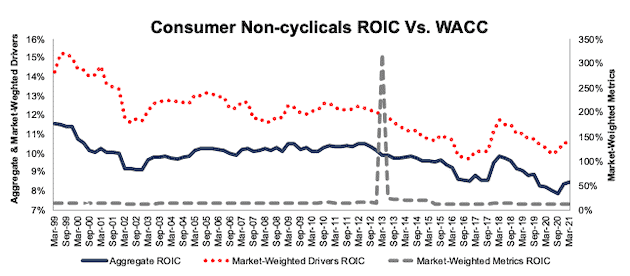

Consumer Non-cyclicals

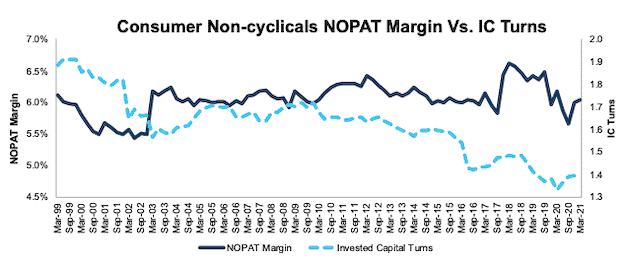

Figure 5 shows ROIC for the Consumer Non-Cyclicals sector slightly rose from 8.2% in 2019 to 8.5% in 2020. Consumer Non-cyclicals NOPAT margin fell from 6.2% in 2019 to 6.0% in 2020 and invested capital turns rose from 1.3 to 1.4 over the same time. Investors only analyzing margins will miss the fact that improved balance sheet efficiency drives ROIC higher for many companies in this sector.

Figure 5: Consumer Non-cyclicals ROIC vs. WACC: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period uses price data as of that date and incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

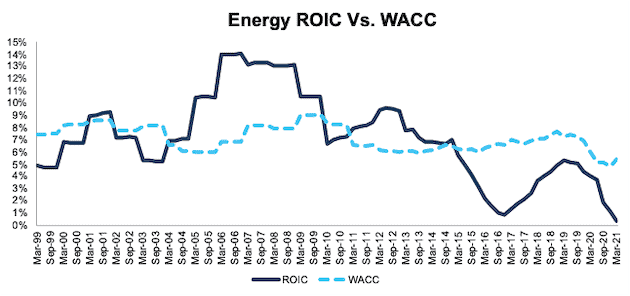

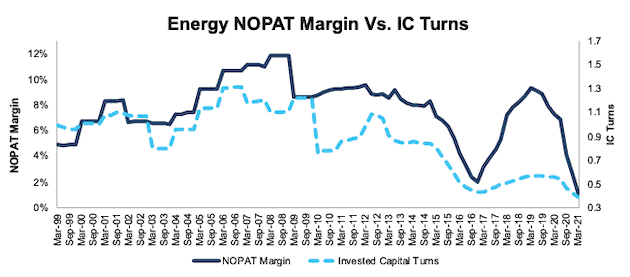

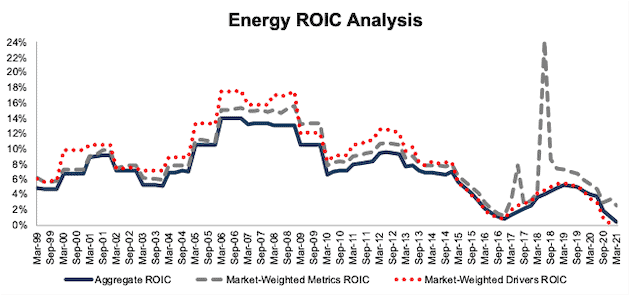

Energy

Figure 6 shows the ROIC for the Energy sector is hit hardest of all sectors as the COVID-19 pandemic combined with increased production from Saudi Arabia and Russia drove oil prices down. The deteriorating ROIC wiped out all the improvement achieved from 2016 to mid-2019. The decline in ROIC is driven by NOPAT margin falling from 7.3% in 2019 to 1.0% in 2020 and invested capital turns falling from 0.55 to 0.39 over the same time.

Figure 6: Energy ROIC vs. WACC: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period uses price data as of that date and incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

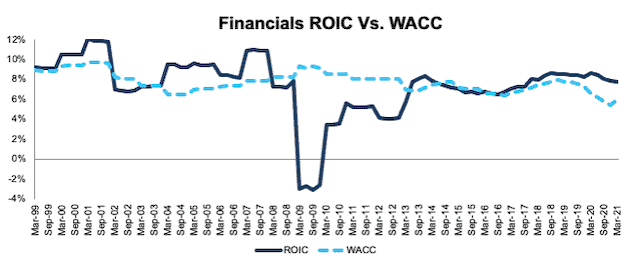

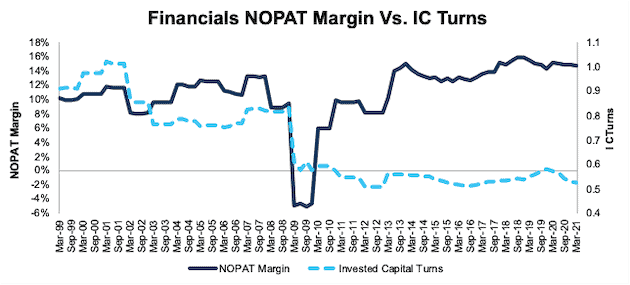

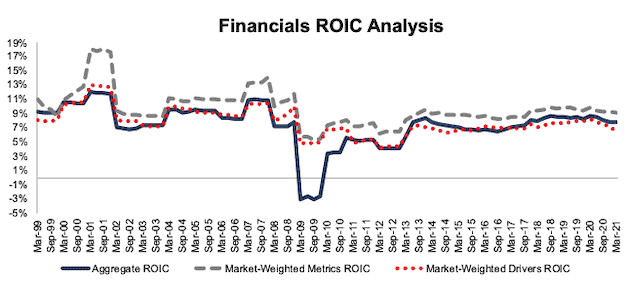

Financials

Figure 7 shows ROIC for the Financials sector declined 93 basis points YoY in 2020 but remains well above the lows of the Financial Crisis. Given the stability in ROIC since 2013, one could argue regulators were successful in turning large Financial firms into “boring”, more stable businesses. Financials NOPAT margin fell from 15.1% in 2019 to 14.7% in 2020 and invested capital turns fell from 0.57 to 0.53 over the same time.

Figure 7: Financials ROIC vs. WACC: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period uses price data as of that date and incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

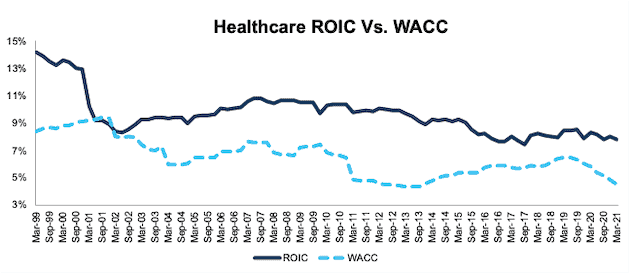

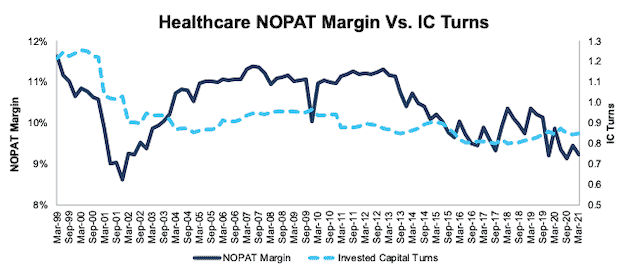

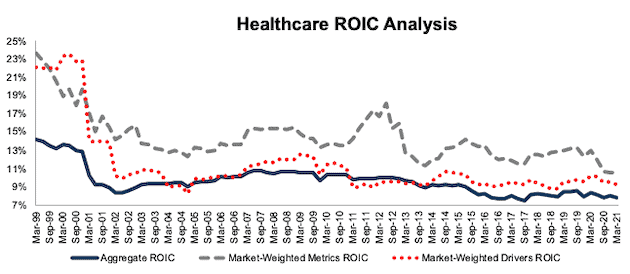

Healthcare

Figure 8 shows ROIC for the Healthcare sector declined 52 basis points YoY in 2020 and has remained relatively stable since the end of 2016. The decline in ROIC is driven by Healthcare NOPAT margin falling from 9.9% in 2019 to 9.2% in 2020. Meanwhile, invested capital turns improved from 0.84 to 0.85 over the same time.

Figure 8: Healthcare ROIC vs. WACC: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period uses price data as of that date and incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

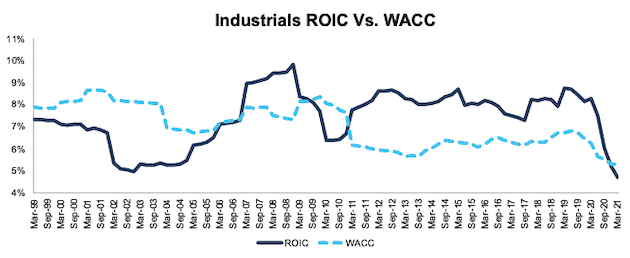

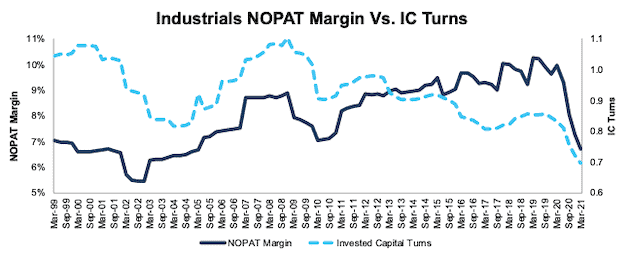

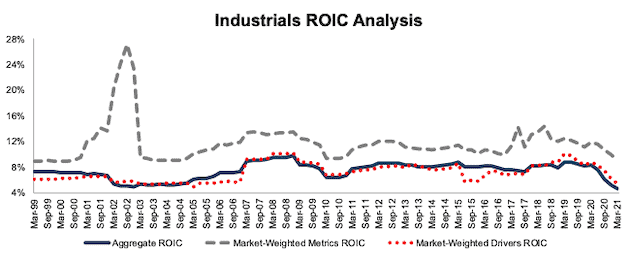

Industrials

Figure 9 shows ROIC for the Industrials sector was the second hardest hit this year and fell 360 basis points YoY in 2020 as the sector bore much of the brunt of the global shutdowns. Industrials NOPAT margin fell from 10.0% in 2019 to 6.7% in 2020 and invested capital turns fell from 0.83 to 0.70 over the same time.

Figure 9: Industrials ROIC vs. WACC: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period uses price data as of that date and incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

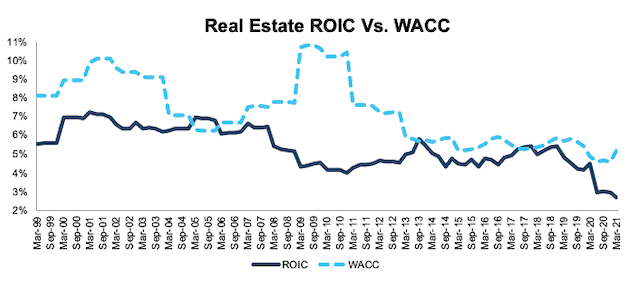

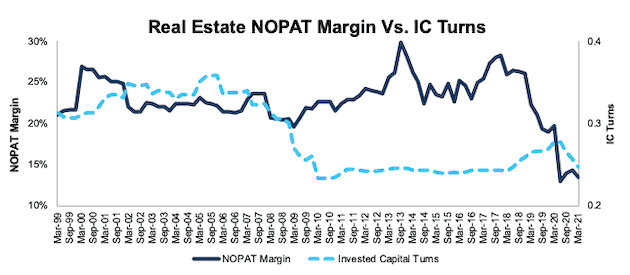

Real Estate

Figure 10 shows ROIC for the Real Estate sector has fallen significantly since 2019. Longer term, the ROIC for the Real Estate sector largely has been in decline since 2000. Real Estate NOPAT margin fell from 19.7% in 2019 to 13.5% in 2020 and invested capital turns fell from 0.23 to 0.20 over the same time.

Figure 10: Real Estate ROIC vs. WACC: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period uses price data as of that date and incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

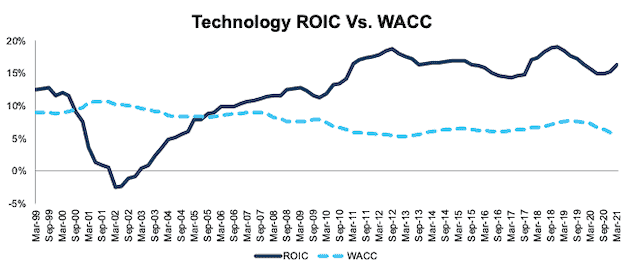

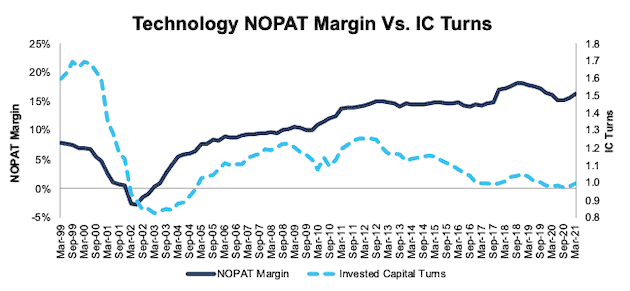

Technology

Figure 11 shows the ROIC for the Technology sector declined since mid-2018 but has turned higher in recent periods. The Technology sector’s 2020 ROIC of 16% is nearly double the next highest sector ROIC. The Technology NOPAT margin rose from 16.1% in 2019 to 16.3% in 2020 and invested capital turns improved from 0.98 to 1.00 over the same time.

Figure 11: Technology ROIC vs. WACC: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period uses price data as of that date and incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

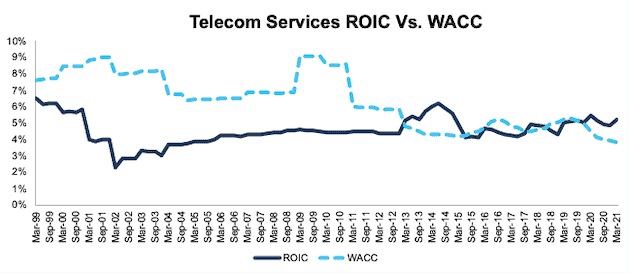

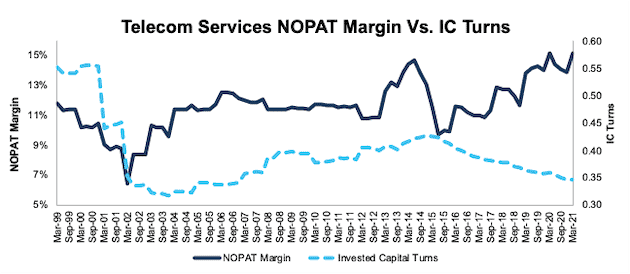

Telecom Services

Figure 12 shows the ROIC for the Telecom Services sector fell 20 basis points YoY in 2020 and remains below its 2014 levels. Telecom Services NOPAT margin improved from 15.1% in 2019 to 15.2% in 2020 and invested capital turns fell from 0.36 to 0.35 over the same time.

Figure 12: Telecom Services ROIC vs. WACC: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period uses price data as of that date and incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

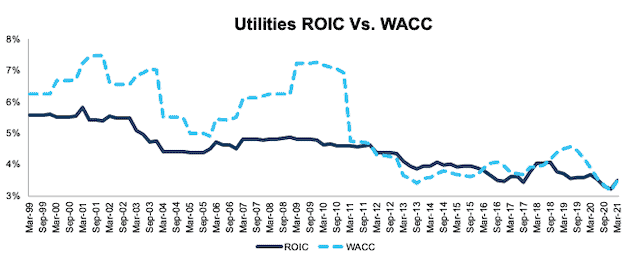

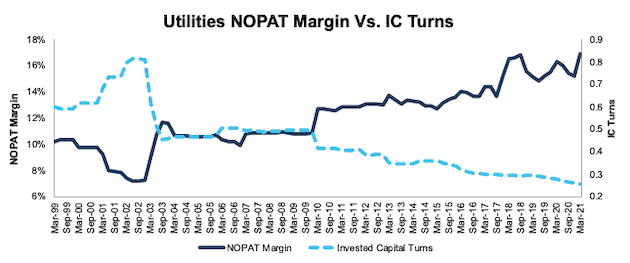

Utilities

Figure 13 shows the ROIC for the Utilities sector fell 18 basis points YoY in 2020 and is in a long-term downtrend. Utilities NOPAT margin improved from 16.3% in 2019 to 16.9% in 2020 and invested capital turns fell from 0.23 to 0.21 over the same time.

Figure 13: Utilities ROIC vs. WACC: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period uses price data as of that date and incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

This article originally published on April 15, 2021.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

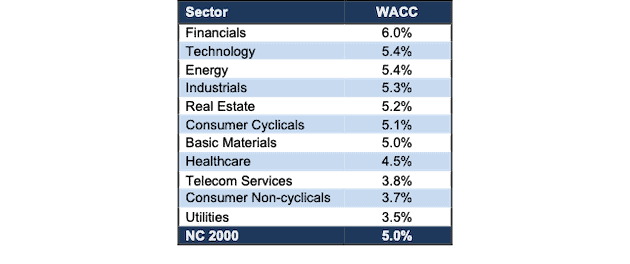

Appendix I: WACC for Each Sector and NC 2000

This appendix shows the WACC for the NC 2000 and each sector in 2020, based on prices as of 3/23/21 and financial data from 2020 10-Ks.

We derive the sector and NC 2000 WACCs by solving for WACC in the economic earnings formula:

(ROIC-WACC)*Average Invested Capital = Economic Earnings

translates to

WACC = ROIC - Economic Earnings/Average Invested Capital

We calculate Economic Earnings, NOPAT and Invested Capital according to the Aggregate methodology described in Appendix III.

Figure 14: WACC by Sector – as of 3/23/21

Sources: New Constructs, LLC and company filings.

Prices as of 3/23/21, financial data from 2020 10-Ks.

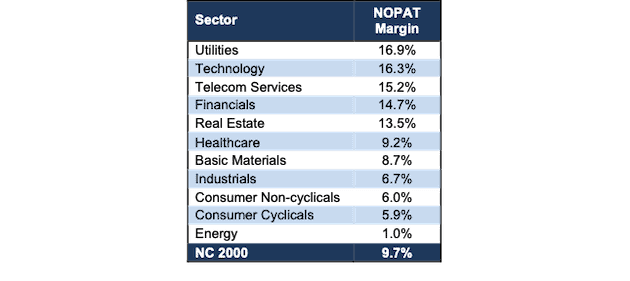

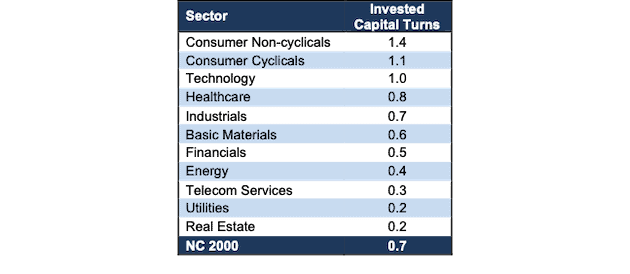

Appendix II: NOPAT Margin and Invested Capital Turns Since 1998

This appendix shows the two key drivers (DuPont model) of ROIC – NOPAT margin and invested capital turns – for each sector going back to 1998. We sum the individual NC 2000/sector constituent values for revenue, NOPAT, and invested capital to calculate these metrics. We call this approach the “Aggregate” methodology. More methodology details in Appendix III.

Figure 15 ranks all 11 sectors by NOPAT margin based on financial data from 2020 10-Ks.

Figure 15: NOPAT Margin by Sector – Financial Data From 2020 10-Ks

Sources: New Constructs, LLC and company filings.

Financial data from 2020 10-Ks.

Figure 16 ranks all 11 sectors by invested capital turns based on financial data from 2020 10-Ks.

Figure 16: Invested Capital Turns by Sector – Financial Data From 2020 10-Ks

Sources: New Constructs, LLC and company filings.

Financial data from 2020 10-Ks.

These two tables show how rare it is for a sector to have both high margins and capital turns. Utilities, the highest margin sector, has the second-worst invested capital turns. Consumer Non-cyclicals, the sector with the highest invested capital turns has the third lowest margin. The Technology sector has both high margins and invested capital turns, which is why that sector leads the market in ROIC by a wide margin.

Figures 17-28 compare the NOPAT margin and invested capital turns trends for the NC 2000 and every sector since March 1999.

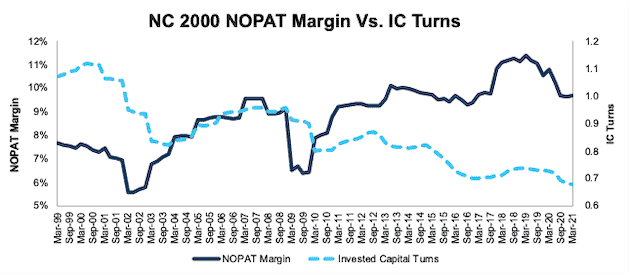

Figure 17: NC 2000 NOPAT Margin and IC Turns: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 18: Basic Materials NOPAT Margin and IC Turns: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 19: Consumer Cyclicals NOPAT Margin and IC Turns: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 20: Consumer Non-Cyclicals NOPAT Margin and IC Turns: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 21: Energy NOPAT Margin and IC Turns: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 22: Financials NOPAT Margin and IC Turns: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 23: Healthcare NOPAT Margin and IC Turns: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 24: Industrials NOPAT Margin vs. IC Turns: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 25: Real Estate NOPAT Margin Vs. IC Turns: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 26: Technology NOPAT Margin Vs. IC Turns: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 27: Telecom Services NOPAT Margin Vs. IC Turns: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 28: Utilities NOPAT Margin vs. IC Turns: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Appendix III: Analyzing ROIC with Different Weighting Methodologies

We derive the metrics above by summing the individual NC 2000/sector constituent values for revenue, NOPAT, and invested capital to calculate the metrics presented. We call this approach the “Aggregate” methodology.

The Aggregate methodology provides a straightforward look at the entire sector, regardless of market cap or index weighting and matches how S&P Global (SPGI) calculates metrics for the S&P 500.

For additional perspective, we compare the Aggregate method for ROIC with two other market-weighted methodologies:

- Market-weighted metrics – calculated by market-cap-weighting the ROIC for the individual companies relative to their sector or the overall NC 2000 in each period. Details:

- Company weight equals the company’s market cap divided by the market cap of the NC 2000/its sector

- We multiply each company’s ROIC by its weight

- NC 2000/Sector ROIC equals the sum of the weighted ROICs for all the companies in the NC 2000/each sector

- Market-weighted drivers – calculated by market-cap-weighting the NOPAT and invested capital for the individual companies in the NC 2000/each sector in each period. Details:

- Company weight equals the company’s market cap divided by the market cap of the NC2000/its sector

- We multiply each company’s NOPAT and invested capital by its weight

- We sum the weighted NOPAT and invested capital for each company in the NC 2000/each sector to determine the NC 2000/sector’s weighted NOPAT and weighted invested capital

- NC 2000/Sector ROIC equals weighted NC 2000/sector NOPAT divided by weighted NC 2000/sector invested capital

Each methodology has its pros and cons, as outlined below:

Aggregate method

Pros:

- A straightforward look at the entire NC 2000/sector, regardless of company size or weighting in any indices.

- Matches how S&P Global calculates metrics for the S&P 500.

Cons:

- Vulnerable to impact of by companies entering/exiting the group of companies, which could unduly affect aggregate values despite the level of change from companies that remain in the group.

Market-weighted metrics method

Pros:

- Accounts for a firm’s size relative to the overall NC 2000/sector and weights its metrics accordingly.

Cons:

- Vulnerable to outsized impact of one or a few companies, as shown below in the Consumer Non-cyclicals sector. This outsized impact tends to occur only for ratios where unusually small denominator values can create extremely high or low results.

Market-weighted drivers method

Pros:

- Accounts for a firm’s size relative to the overall NC 2000/sector and weights its NOPAT and invested capital accordingly.

- Mitigates potential outsized impact of one or a few companies by aggregating values that drive the ratio before calculating the ratio.

Cons:

- Can minimize the impact of period-over-period changes in smaller companies, as their impact on the overall sector NOPAT and invested capital is smaller.

Figures 29-40 compare these three methods for calculating NC 2000 and sector ROICs.

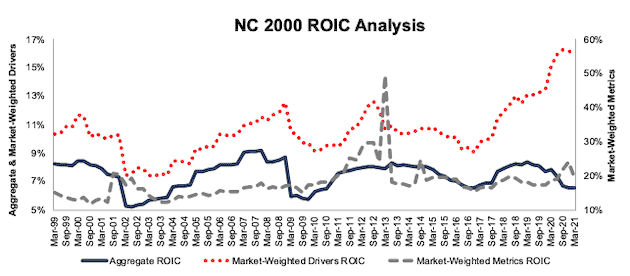

In Figure 29, we chart the market-weighted metrics version of ROIC on its own axis to highlight the differences in the aggregate and market-weighted drivers versions of ROIC.

Note the impact on the market-weighted metrics version of ROIC for the entire NC 2000 from Lorillard (LO) in 2013, when the firm’s ROIC was more than 36,000%.

Figure 29: NC 2000 ROIC Methodologies Compared: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 30: Basic Materials ROIC Methodologies Compared: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 31: Consumer Cyclicals ROIC Methodologies Compared: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Note the impact on the market-weighted metrics version of ROIC for the Consumer Non-cyclicals sector from Lorillard (LO) in 2013, when the firm’s ROIC was more than 36,000%.

This outlier caused the Consumer Non-cyclicals sector’s ROIC to increase from 15% to 321% in just one period, before falling to 24% one period later.

Figure 32: Consumer Non-cyclicals ROIC Methodologies Compared: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 33: Energy ROIC Methodologies Compared: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 34: Financials ROIC Methodologies Compared: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 35: Healthcare ROIC Methodologies Compared: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

Figure 36: Industrials ROIC Methodologies Compared: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

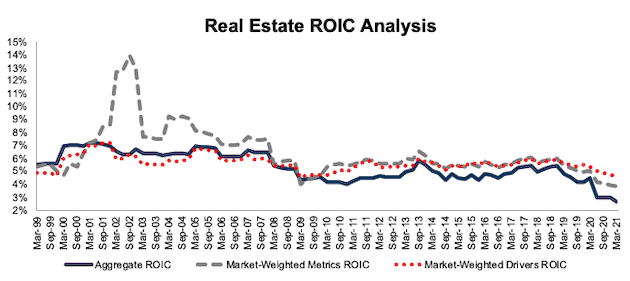

Figure 37: Real Estate ROIC Methodologies Compared: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

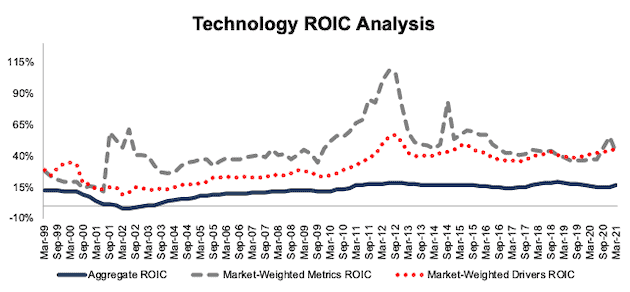

Figure 38: Technology ROIC Methodologies Compared: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

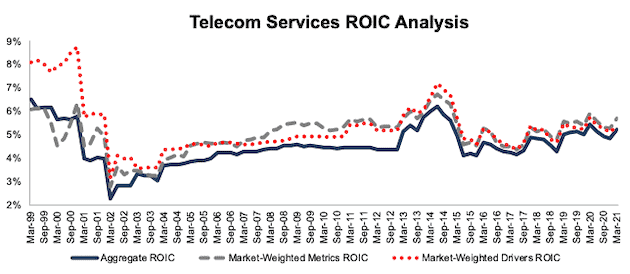

Figure 39: Telecom Services ROIC Methodologies Compared: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

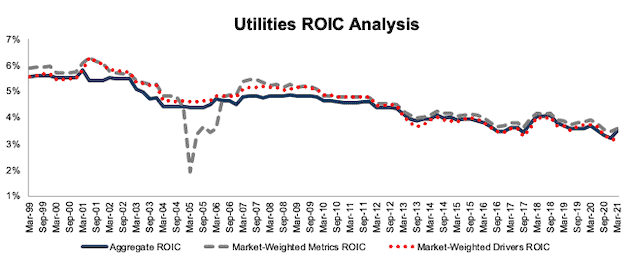

Figure 40: Utilities ROIC Methodologies Compared: March 1999 – 3/23/21

Sources: New Constructs, LLC and company filings.

The March 23, 2021 measurement period incorporates the financial data from 2020 10-Ks, as this is the earliest date for which all the 2020 10-Ks for the NC 2000 constituents were available.

[1] We calculate these metrics based on SPGI’s methodology, which sums the individual NC 2000 constituent values for NOPAT and invested capital before using them to calculate the metrics. We call this the “Aggregate” methodology. Get more details in Appendix III. See Appendix I for details on how we calculate WACC for the NC 2000 and each of its sectors.

[2] For 3rd-party reviews, including The Journal of Financial Economics, on our more reliable fundamental data, historically and prospectively, across all stocks, click here and here.

[3] We use stock prices from 3/23/21 because that is the date when all the 2020 10-Ks for the NC 2000 constituents were available.

2 replies to "All Cap Index & Sectors: ROIC Vs. WACC Through 4Q20"

Hello

Very interesting and well documented research.

Do you haven more recent ROIC and WACC figures? And a Global approach?

Tnx

Han van Rhee

Hi Hans:

Yes, we have the data as of the latest filings.

Our coverage focus is on US exchanges, and we are moving to Global coverage very soon.