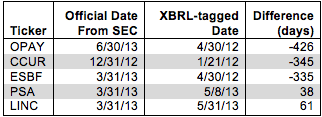

The potential utility of XBRL as a tool for regulators to fight fraud and investors to better analyze companies makes its numerous flaws that much more of a shame. I can only hope that the SEC realizes the value of XBRL and makes a commitment to ensuring the accuracy and validity of XBRL data.

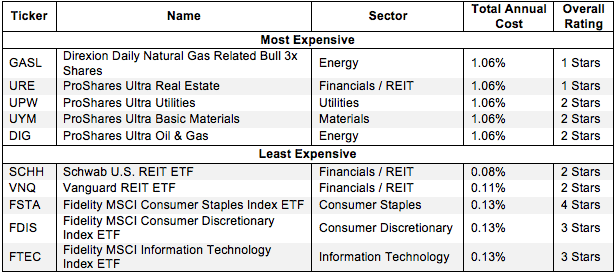

Picking from the multitude of sector ETFs is a daunting task. In any given sector there may be as many as 44 different ETFs, and there are at least 183 ETFs across all sectors.

Fund holdings affect fund performance more than fees or past performance. A cheap fund is not necessarily a good fund. A fund that has done well in the past is

The Small Cap Value style ranks last out of the twelve fund styles as detailed in my Style Rankings for ETFs and Mutual Funds report. It gets my Dangerous rating, which is based on aggregation of ratings of 15 ETFs and 236 mutual funds in the Small Cap Value style as of October 24, 2013.

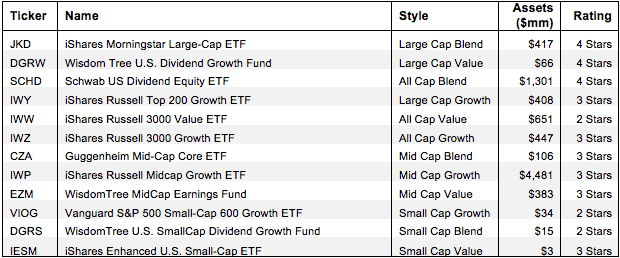

The Small Cap Blend style ranks eleventh out of the twelve fund styles as detailed in my Style Rankings for ETFs and Mutual Funds report. It gets my Dangerous rating, which is based on aggregation of ratings of 24 ETFs and 629 mutual funds in the Small Cap Blend style as of October 24, 2013.

The Small Cap Growth style ranks tenth out of the twelve fund styles as detailed in my Style Rankings for ETFs and Mutual Funds report. It gets my Dangerous rating, which is based on aggregation of ratings of 11 ETFs and 441 mutual funds in the Small Cap Growth style as of October 23, 2013.

The Mid Cap Value style ranks ninth out of the twelve fund styles as detailed in my Style Rankings for ETFs and Mutual Funds report. It gets my Dangerous rating, which is based on aggregation of ratings of 12 ETFs and 190 mutual funds in the Mid Cap Value style as of October 22, 2013.

The Mid Cap Growth style ranks eighth out of the twelve fund styles as detailed in my Style Rankings for ETFs and Mutual Funds report. It gets my Neutral rating, which is based on aggregation of ratings of 10 ETFs and 360 mutual funds in the Mid Cap Growth style as of July 16, 2013.

Today, I had the pleasure of meeting with a very smart and attentive group of Vanderbilt undergrads as part of the Managerial Studies Visiting Executive Program.

The Mid Cap Blend style ranks seventh out of the twelve fund styles as detailed in my Style Rankings for ETFs and Mutual Funds report. It gets my Dangerous rating, which is based on aggregation of ratings of 16 ETFs and 324 mutual funds in the Mid Cap Blend style as of October 18, 2013. Prior reports on the best & worst ETFs and mutual funds in every sector and style are here.

The Large Cap Value style ranks second out of the twelve fund styles as detailed in my Style Rankings for ETFs and Mutual Funds report. It gets my Neutral rating, which is based on aggregation of ratings of 45 ETFs and 765 mutual funds in the Large Cap Value style as of October 18, 2013. Prior reports on the best & worst ETFs and mutual funds in every sector and style are here.

The Large Cap Growth style ranks fourth out of the twelve fund styles as detailed in my Style Rankings for ETFs and Mutual Funds report. It gets my Neutral rating, which is based on aggregation of ratings of 22 ETFs and 657 mutual funds in the Large Cap Growth style as of October 17, 2013. Prior reports on the best & worst ETFs and mutual funds in every sector and style are here.

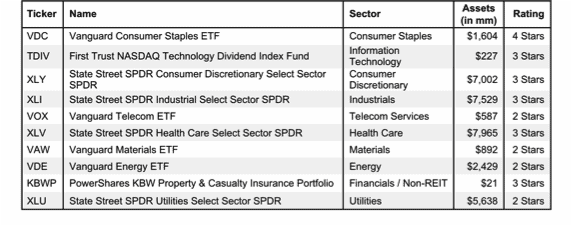

Consumer Discretionary mutual fund managers and ETF providers are in the Danger Zone this week. They do the worst job of picking stocks out of all the sectors. The quality of the funds and ETFs in the Consumer Discretionary sector is the worst of all sectors compared to the quality of the stocks available to them.

The Large Cap Blend style ranks first out of the twelve fund styles as detailed in my Style Rankings for ETFs and Mutual Funds report. It gets my Neutral rating, which is based on aggregation of ratings of 33 ETFs and 908 mutual funds in the Large Cap Blend style as of October 17, 2013. Prior reports on the best & worst ETFs and mutual funds in every sector and style are here.

The All Cap Value style ranks fifth out of the twelve fund styles as detailed in my Style Rankings for ETFs and Mutual Funds report. It gets my Neutral rating, which is based on aggregation of ratings of 2 ETFs and 238 mutual funds in the All Cap Value style as of October 17, 2013. Prior reports on the best & worst ETFs and mutual funds in every sector and style are here.