Valeant Pharmaceuticals (VRX: $33/share) fell 51% yesterday and the stock still has further to fall. While direct share holders stand to lose the most, certain fund investors face significant downside risk as well. These investors may not realize the risk they’re taking due to the shortcomings of traditional fund research, which doesn’t focus on fund holdings.

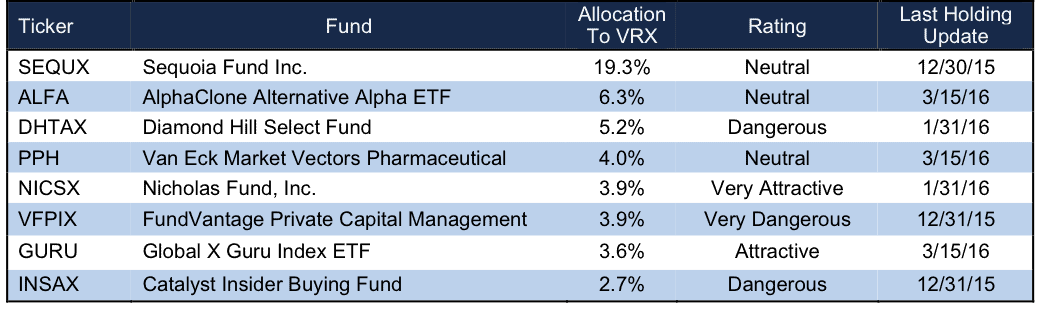

By analyzing each holding of a fund, we provide investors with deeper insight into the risk/reward of funds. Our predictive ratings for ETFs and mutual funds give investors a different perspective as they are based on the quality of the fund’s holdings. Figure 1 shows the 10 ETFs and mutual funds that allocate significantly to VRX and could pose a risk to investors’ portfolios.

Figure 1: Funds With Exposure To and Risk of Decline from Holding VRX

Sources: New Constructs, LLC and company filings

Sequoia Fund (SEQUX) allocates just below 25% of its assets to Valeant. Diamond Hill Select Fund (DHTAX), FundVantage Private Capital Management Value Fund (VFPIX), and Catalyst Insider Buying Fund (INSAX), earn a Dangerous-or-worse rating in part because of their poor holdings like VRX, but also because each fund charges investors high total annual costs.

It’s not all negative though. Nicholas Fund (NICSX) and Global X Guru Index ETF (GURU) earn an Attractive-or-better rating because the quality of the entirety of holdings makes up for their allocation to VRX.

The takeaway is: Buying a fund without analyzing its holdings is like buying a stock without analyzing its business and finances. Those who bought VRX based on trust in the company non-GAAP earnings did not understand the firm’s true finances, which showed Valeant was not a good business. Without analyzing each holding, inventors are taking on unnecessary risk when investing in ETFs or mutual funds.

What Makes VRX Such A Poor Holding?

Valeant had been in a bit of a limbo lately, as investors awaited the long delayed 4Q15 results. The company finally released its earnings today and the results were to be expected if you heeded our previous warnings.

In the release, the company recognized the significant issues it faces after the termination of its relationship with Philidor, the cancellation of almost all price increases, and underperformance in several of its business lines. Not only did Valeant report weak results for 4Q15, but looking forward, the company guided for revenue ($2.3-$2.4 billion vs. $2.8-$3.1 billion expected) and earnings ( $1.30-$1.55/share vs. $2.35-$2.55/share expected) to come in significantly below expectations.

Adding even more uncertainty, Valeant also revealed that it faces a risk of default if it is unable to file its 10-K with the SEC by April 29, which would break its reporting covenant in its bond indentures. The initial filing was due February 29 but has been delayed while Valeant investigates its business relationship with Philidor. Valeant is already in the process to extend deadlines for filing it 10-Q for the first quarter of 2016.

Has The House Of Cards Finally Collapsed?

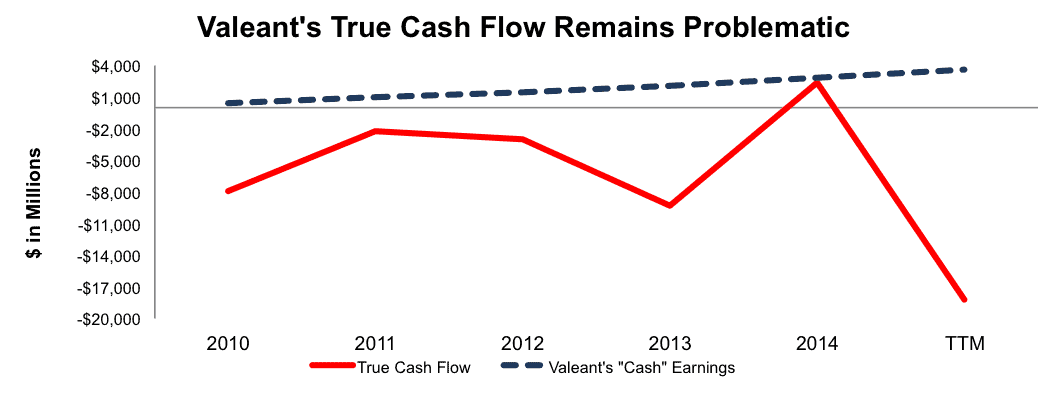

As early as June 2014, we pointed out Valeant was presenting itself in a misleading way. Ultimately, the company was relying on non-GAAP metrics to present its cash flow as highly positive, when in fact, the true cash flows of the business have been highly negative. This contrast between cash flow calculations is a topic of much debate between bears and bulls of Valeant and really gets at the heart of why non-GAAP metrics continually fail investors when analyzing a company. Analysis using Valeant’s reported “Cash Earnings” weren’t getting a true picture of the company, as can be seen in Figure 2.

The company’s non-GAAP “cash earnings” have grown from $421 million in 2010 to $3.55 billion over the latest trailing-twelve months (TTM). In reality, free cash flow has been highly negative with a cumulative -$38.4 billion in losses over the same time frame. Cumulative non-GAAP earnings during the same time are $11.2 billion.

Figure 2: True Cash Flow Provides True Picture of Valeant

Sources: New Constructs, LLC and company filings

Valeant uses non-GAAP metrics to make its business look better than it is according to corporate accounting rules (i.e. GAAP) while burning through cash at an unsustainable and alarming rate.

Non-GAAP Doesn’t Pay Down Debt

As seen above Valeant’s true cash flow is not only much lower than Valeant would have investors believe, it is also largely negative. While management can prop up shares by touting non-GAAP results, those results don’t help pay debt covenants because the true cash flow is not available. Debt covenants may soon become just another issue in the already long list if Valeant defaults on its bond indentures. We already know Valeant has raised significant capital, as its debt has increased from $372 million in 2009 to $30 billion over the last twelve months. Without a sale of assets, one has to wonder how well Valeant can service such debt because it won’t be happening with non-GAAP “cash earnings.”

Warning Signs Were All Around

The warning signs at Valeant have long been in clear view, if you looked past the positive analyst sentiment, excellent non-GAAP results, and management rhetoric.

- In June 2014, we noted that Valeant was presenting its business in a misleading way to bolster its takeover attempt of Allergan.

- Valeant claimed it was undervalued passed on P/E ratios when in fact the company was comparing its adjusted P/E to the unadjusted P/E of industry and market peers.

- Additionally, Valeant claimed its previous acquisitions were value creating when in fact the company’s return on invested capital (ROIC) has been in decline for quite some time. From 2009 to the last twelve months, Valeant’s ROIC has fallen from 15% to 5%.

- In July 2014, Valeant made our list of companies with the most misleading non-GAAP earnings. According to GAAP, Valeant lost $866 million in 2013, but by their non-GAAP metrics the company earned $2 billion. This disconnect stems primarily from excluding the costs related to its acquisitions. Does it make sense to exclude the costs related to how you grow your business from how you measure profits? We find that fishy.

- We revisited the non-GAAP red flag again in November 2015,and the story had only gotten worse.

- In February 2016, we placed Valeant in the Danger Zone. After today’s share price decline, VRX is down 57% since our report.

Stock Remains Overvalued, Even After 40% Decline

After such a drastic price decline, one might think VRX is a bargain. Not even close. Those purchasing Valeant now would be buying a highly overvalued stock with a long history of misleading accounting. These are not exactly the characteristics of a quality investment.

In order to justify its current price of $36/share, the company would need to grow NOPAT by 15% compounded annually for the next 8 years. In this scenario, Valeant would be generating $29 billion in revenue, greater than AstraZeneca’s (AZN) 2015 revenue.

Even in an ideal scenario, in which Valeant focuses on internal growth and not destructive acquisitions, VRX still has significant downside. If Valeant can grow NOPAT by 9% compounded annually for the next decade, the stock is worth $23/share today – a 36% downside.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Click here to download a PDF of this report.

Photo Credit: lendingmemo (Flickr)