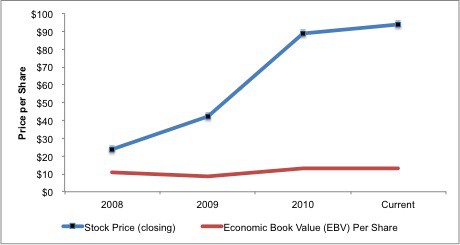

VMW’s valuation has its head in the clouds.

This stock is a great short in most any scenario and is especially attractive in the event of a global economic slowdown led by a recession in Europe.

As an adult, Halloween tends not to be that scary for me usually.

But after last week’s stock market rally in the face of the deteriorating situation in Europe and the rest of the world, I am afraid…for the stock market and am reminded of fall/winter 1999.

Mr. Bogle, an invaluable voice of reason for investors over many years, suggests that there is too much speculation in our equity markets.

His comments jibe entirely with my post, Rise of the Speculative Movement.

Here is a free copy of our report on GE for Ask Matt readers. This report provides details behind Matt’s analysis of GE in his recent article in USA Today. Click here for our report: General Electric (GE) Neutral Risk/Reward Rating.

Great interview this am with Dagan McDowell and Ashley Webster about my recent article: "The Fed’s Bazooka: Revealed As Final Policy Firepower in Jackson Hole".

Too much of the rhetoric surrounding S&P’s downgrade of US debt misses the largest and most important point made by S&P’s bold move: the U.S. financial situation is very bad and getting worse with no reconciliation in sight.

It is difficult to deny the poor credit quality of an entity that grossly overspends its revenues, has a mountain of debt (most of which matures within the next few years) and has taken no meaningful steps toward remedying the situation?

By quibbling over S&P’s procedures and calculations, the Treasury and White House reveal that they have no solid rationale for disagreeing with the downgrade.

The paramount innovation in the Federal Reserve’s statement yesterday was that it will keep interest rates low until at least the middle of 2013.

Did anyone really expect the Fed to announce it would raise rates anytime in the near future?

The market decline experienced thus far is closer to its beginning rather then its end. Today’s refreshing market rise is likely just a flash in the pan.

The market needs to go down again before it can sustain any future rise.

Here is a free copy of our report on Berkshire Hathaway, Inc. (BRK.A) for Ask Matt readers. This report provides details behind Matt’s analysis of BRK.A in his recent article in USA Today.

Here is a free copy of our report on KRO for Ask Matt readers. This report provides details behind Matt’s analysis of KRO in his recent article in USA Today.

Click

While I cannot predict what WikiLeaks will leak about some major banks, I have a hunch that one of the revelations might be from a special New Constructs report provided to the Senate Banking Committee’s Subcommittee on Securities, Insurance, and Investment.

Contrary to nearly every headline you read about monetary policy these days, I believe it is quite possible the Fed Chairmen Ben Bernanke is performing quite well and much better than any of his recent predecessors. In fact, I think he is directing monetary policy with unprecedented precision and skill.

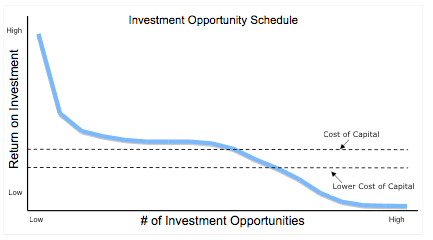

Maintaining artificially low interest rates or excessive money supply does permanent damage to economies in the medium and long-term because it delays creative destruction, the process of replacing low-return investments with higher-return investments. To help illustrate this point, I present the “Investment Opportunity Schedule” in Exhibit 1

The Risk/Reward of the entire S&P 500 gets our Neutral Rating. Our recently published Index Benchmark report on the S&P 500 offers unique insights into the underlying profitability and valuation of all the companies comprised by this index. It also offers benchmarks for (1) investors considering buying ETFs or Index Funds based on the S&P 500 and for (2) comparing individual stocks to the S&P 500.

In another excellent expose "Wall Street Proprietary Trading Under Cover", Michael Lewis exposes Wall Street's plan to exploit loopholes in the laws and regs to continue proprietary trading, the activity that was the primary downfall of Bear Stearns and Lehman Brothers.

At a time when most of the public believes political leadership to be weak, we should not focus on finding scapegoats but rather on assuming accountability to help fix problems.

For anyone who questions whether or not the rules of the game are controlled by those wuith the most money not the most ability, look no farther than Wall Street's compensation.