Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life and MarketWatch.com.

Snow Capital Small Cap Value Fund receives our Very Dangerous rating and its poor holdings and high fees land it in the Danger Zone this week.

The only justification for mutual funds to have higher fees than ETFs is “active” management that leads to out-performance. How can a fund that has significantly worse holdings than its benchmark hope to outperform?

Snow Capital Small Cap Value investors are paying higher fees for stock selection that is much worse than its benchmark, the iShares Russell 2000 Value ETF (IWN).

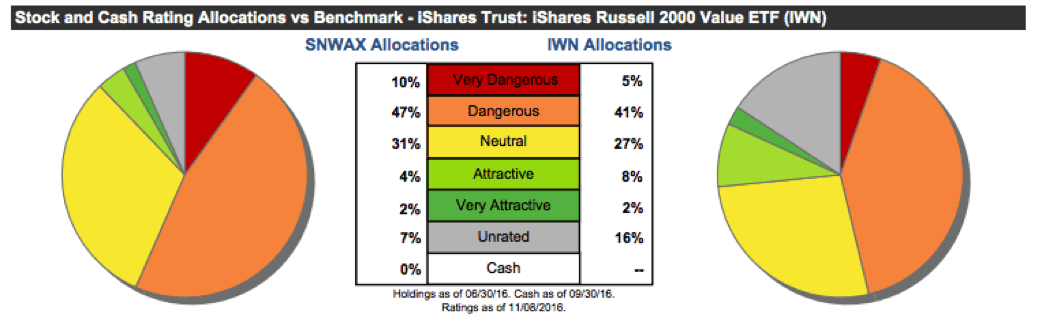

Per Figure 1, Snow Capital Small Cap Value Fund allocates 57% of capital to Dangerous-or-worse rated stocks, compared to IWN’s 45%. On the flip side, IWN allocates more (at 10% of its portfolio) to Attractive-or-better rated stocks than SNWAX, at only 6%.

Figure 1: Snow Capital Small Cap Value Fund Asset Allocation

Sources: New Constructs, LLC and company filings

Furthermore, half of the mutual fund’s top 10 holdings receive our Dangerous-or-worse rating and make up nearly 19% of its portfolio.

If Snow Capital Small Cap Value Fund holds worse stocks than IWN, then how can one expect the outperformance required to justify higher fees?

“Value” Is Misleading Especially When You Can’t See Managers’ Process

We do not understand how this fund can call itself a value fund because the managers allocate too much capital to some of the most overvalued stocks in the market. We know this fact because we analyze each of the fund’s holdings and model the future cash flow expectations embedded in the prices of the individual stock holdings.

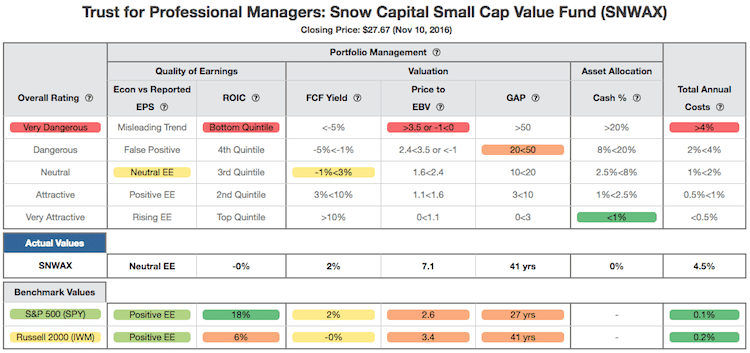

Figure 2 contains our detailed fund rating for SNWAX, which includes each of the criteria we use to rate all funds under coverage. Note that Figure 2 is very similar to our Stock Rating Methodology, because the performance of a fund’s holdings equals the performance of a fund. Unfortunately, the results of this analysis are not positive for investors in Snow Capital Small Cap Value funds.

Figure 2: Snow Capital Fund (SNWAX) Rating Breakdown

Sources: New Constructs, LLC and company filings

Our findings from our discounted cash flow valuation of the fund reveal the market implied growth appreciation period (GAP) is 34 years for the iShares Russell 2000 Value and 27 years for the S&P 500 – compared to 41 years for SNWAX. In other words, the market expects the stocks held by SNWAX to grow economic earnings for seven years longer than the stocks in the Russell 2000 Value and 14 years longer than the stocks in the S&P 500.

This expectation seems even more out of reach when considering the return on invested capital (ROIC) of the S&P is 18%, 5% for the Russell 2000 Value, and 0% for Snow Capital Small Cap Value Fund.

Lastly, the price-to-economic book value (PEBV) ratio for the S&P 500, which includes some of the world’s most successful companies, is 2.6. The PEBV ratio for SNWAX is 7.1. This ratio means that the market expects the profits for the S&P 500 to increase 260% from their current levels versus 710% for SNWAX, per Figure 2 above.

At the end of the day, the high profit growth expectations baked into the valuations of stocks held by Snow Capital Small Cap Value Fund not only makes its “value” classification hard to justify, but also makes valuation risk higher and outperformance less likely.

“Value” is obviously a relative term for this fund. Investors should make sure they agree with Snow Capital’s definition of value before trusting the “value” label.

Why Expense Ratios Are Misleading: This Fund Is Really Expensive

With total annual costs (TAC) of 4.49%, SNWAX charges more than 99% of Small Cap Value mutual funds. Coupled with its poor holdings, high fees make SNWAX (and the other classes of shares) even more dangerous. More details can be seen in Figure 3, which includes the two additional classes of the Snow Capital Small Cap Value Fund, which also receive our Very Dangerous rating. For comparison, the average TAC of the 264 Small Cap Value mutual funds is 2.33%, the weighted average is lower at 1.6%, and the benchmark, IWN, charges total annual costs of 0.28%.

Figure 3: Snow Capital Small Cap Value Fund’s Understated Costs

Sources: New Constructs, LLC and company filings

Over a 10-year holding period, the 2.79 percentage point difference between SNWAX’s TAC and its reported expense ratio results in 32% less capital in investors’ pockets.

To justify its higher fees, the Snow Capital Small Cap Value Fund must outperform its benchmark (IWN) by the following over three years:

- SNWAX must outperform by 4.20% annually.

- SNWCX must outperform by 3.03% annually.

- SNWIX must outperform by 1.89% annually.

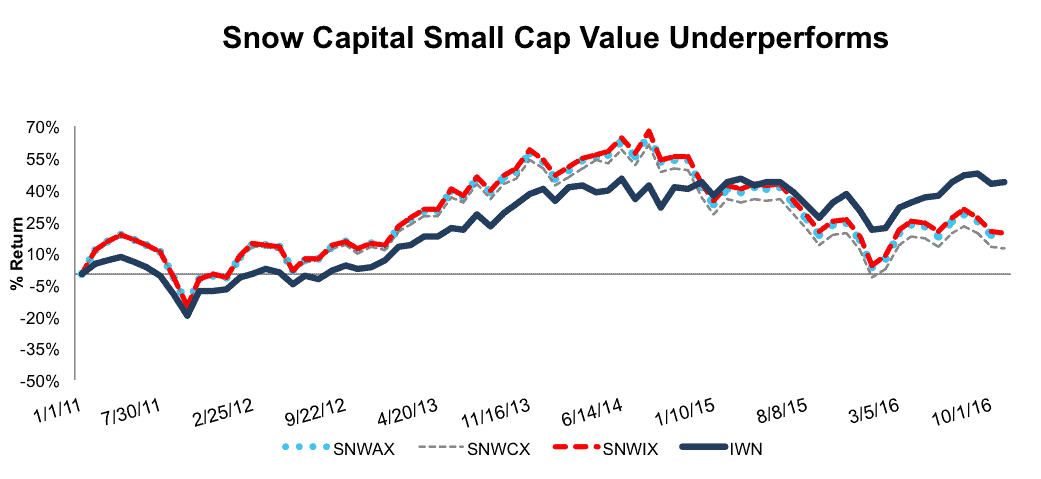

The outperformance that excessive fees require (for investors to get their money’s worth) becomes even harder to justify given that the Snow Capital Small Cap Value Fund has underperformed per Figure 4. Since inception in 2010, SNWAX is up 25%, SNWCX is up 19%, and SNWIX is up 27% Meanwhile, IWN is up 47% over the same time. Figure 3 has more details.

This performance does not assume reinvestment of dividends/capital gains and only represents the price change during the time period, irrespective of dividends or fees. We use the same approach to measuring performance for the benchmark and other funds in order to allow comparability. Ultimately, the underlying fundamentals of Snow Capital Small Cap Value Fund’s holdings don’t warrant such high valuations.

With such high costs and worse holdings than its benchmark, we think it overly optimistic to invest in the belief that these mutual funds will ever outperform their much cheaper ETF benchmark over significant time frames.

Figure 4: Snow Capital Small Cap Value’s Return Vs. IWN

Sources: New Constructs, LLC and company filings.

The Importance of Holdings Based Fund Analysis

The analysis above shows that investors might want to withdraw most or all of the $50 million in Snow Capital Small Cap Value Fund and put the money into better funds within the same style. The top rated Small Cap Value mutual fund is Royce Special Equity Fund (RSEIX, RYSEX, RSEFX) Each of these classes earn an Attractive rating and charge total annual costs of 1.29%, 1.41%, and 1.68% respectively, well below Snow Capital Small Cap Value funds.

Without analysis into a fund’s holdings, investors risk putting their money in funds that are more likely to underperform, despite having much better options available.

More Fund Research That Does A Deep Dive Into Holdings

Each quarter we rank the 10 sectors in our Sector Ratings for ETF & Mutual Funds and the 12 investment styles in our Style Ratings For ETFs & Mutual Funds report. For the fourth quarter of 2016 rankings, a long-term trend continued: in 12 of the past 17 quarters, the Small Cap Value style has ranked last. Within that style, we found a particularly bad fund, one that investors using traditional fund research may believe is an excellent fund.

As we know, past performance is no indicator of future success, which is why the backbone of our ETF and mutual fund ratings is the quality of the holdings. After all, the performance of the holdings drives the performance of the fund.

This article originally published here on November 14, 2016.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, sector, style, or theme.

Scottrade clients get a Free Gold Membership ($588/yr value) as well as 50% discounts and up to 20 free trades ($140 value) for signing up to Platinum, Pro or Unlimited memberships. Login or open your Scottrade account & find us under Quotes & Research/Investor Tools.

Click here to download a PDF of this report.

Photo Credit: Finance Blue (Flickr)