Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life and MarketWatch.com.

This week, we’re putting recent and future tech IPOs in the Danger Zone. Over the past several weeks, we’ve put two recent tech IPOs in the Danger Zone (with positive results), and have seen many others crash and burn in similar ways. Investors seem to not have learned their lesson, and GoDaddy’s (GDDY) IPO on April 1 saw the company’s stock rise over 30% on the first day of trading.

The rush to cash in on easy liquidity is on. Companies are being taken public in the hopes that they’ll be able to cash in on the last of the easy money available before the Federal Reserve raises interest rates later this year.

So why shouldn’t you invest in Tech IPOs?

They’re Often Overvalued

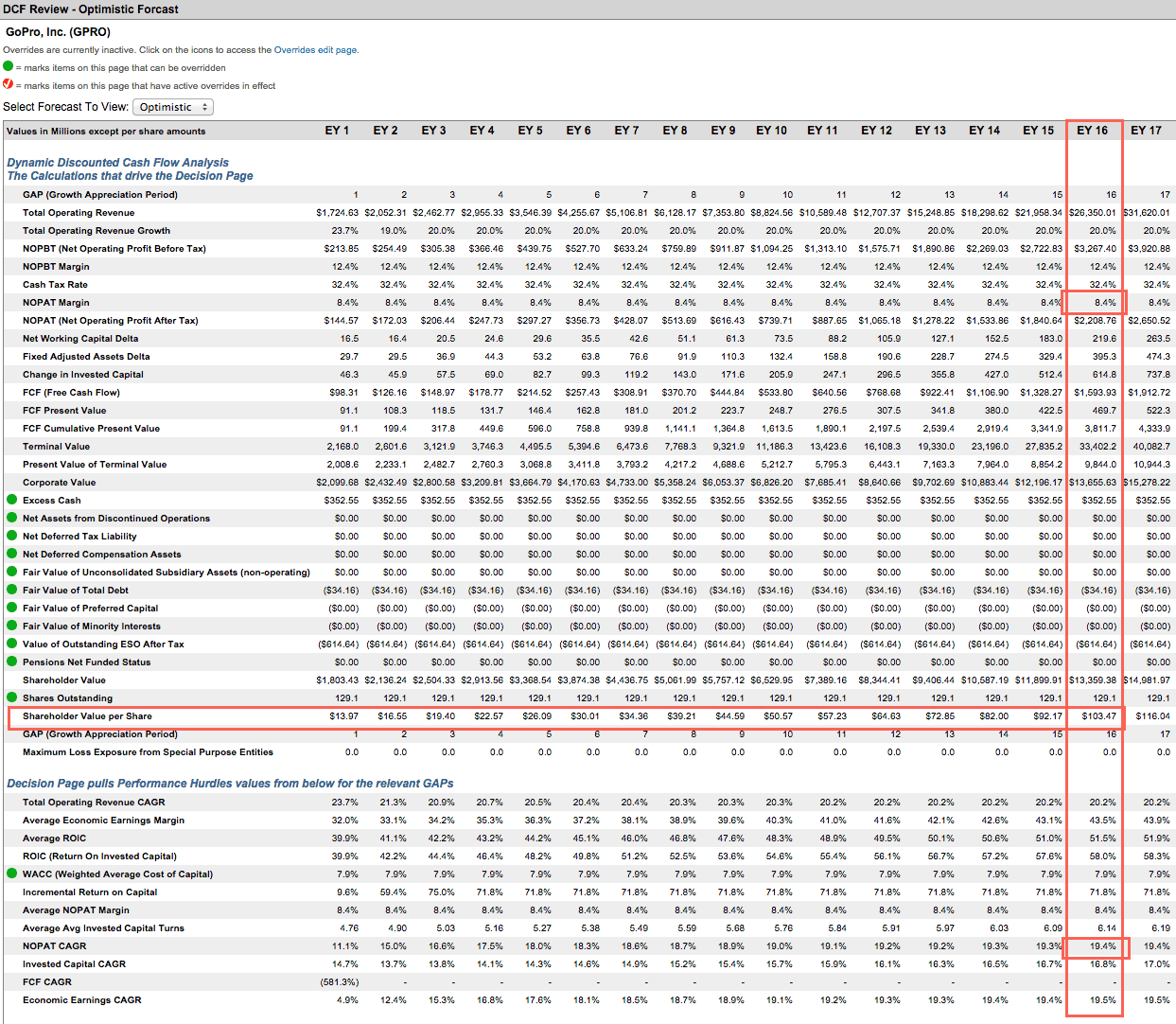

GoPro (GPRO) — Down 55% since October

Even when the financials of these recent Tech IPO companies are good, their stocks are often driven up by Wall Street and media hype. Take GoPro for instance, which sells high-definition personal cameras at a premium price point. GoPro’s strong brand name going into its IPO drove its valuation up much higher than the company could justify financially.

This doesn’t mean that GoPro isn’t financially sound. The company has a return on invested capital (ROIC) of 54%, which puts it in the top quintile of all companies we cover. The company is also growing operating profit (NOPAT) and revenue consistently year over year at rates of 89% and 41%, respectively. Those numbers mean that GoPro is expanding its margins while also expanding sales, a good sign for a young business still in its growth stages.

However, this level of profit growth can’t continue forever, especially with the accompanying margin expansion and investors know that fact. However, the stock’s valuation several months ago implied that this kind of growth would continue almost indefinitely. Specifically, to justify this price, the company would have needed to grow NOPAT by 19% compounded annually for the next 16 years with absolutely no margin compression.

{kind=link}

While the stock has declined since its high of $98/share, GPRO’s current price of $42/share still implies that the company will continue at its current breakneck speed for the next 10 years, even as competitors are coming out of the woodwork. Polarioid, Xiaomi, iON, and Apple have all announced small, high quality video cameras or plans to compete with GoPro’s line for the active/sporty consumer market. Some of these new offerings even boast premium features, like waterproofing.

GPRO dropped big on several weak guidance issuances, which scared already nervous investors. The stock dropped 15% alone on Feb. 5 when GoPro issued guidance above consensus for revenue, but in line with consensus EPS. It seems investors are also aware that the company has no moat, as it declined on new that Apple (AAPL) had patented a “sports camera” system. In addition, when the camera was blamed for Michael Schumacher’s concussion after a skiing accident, the stock dropped 13%.

Why would you invest in a company when events like these can cause you to lose substantial portions of your investment?

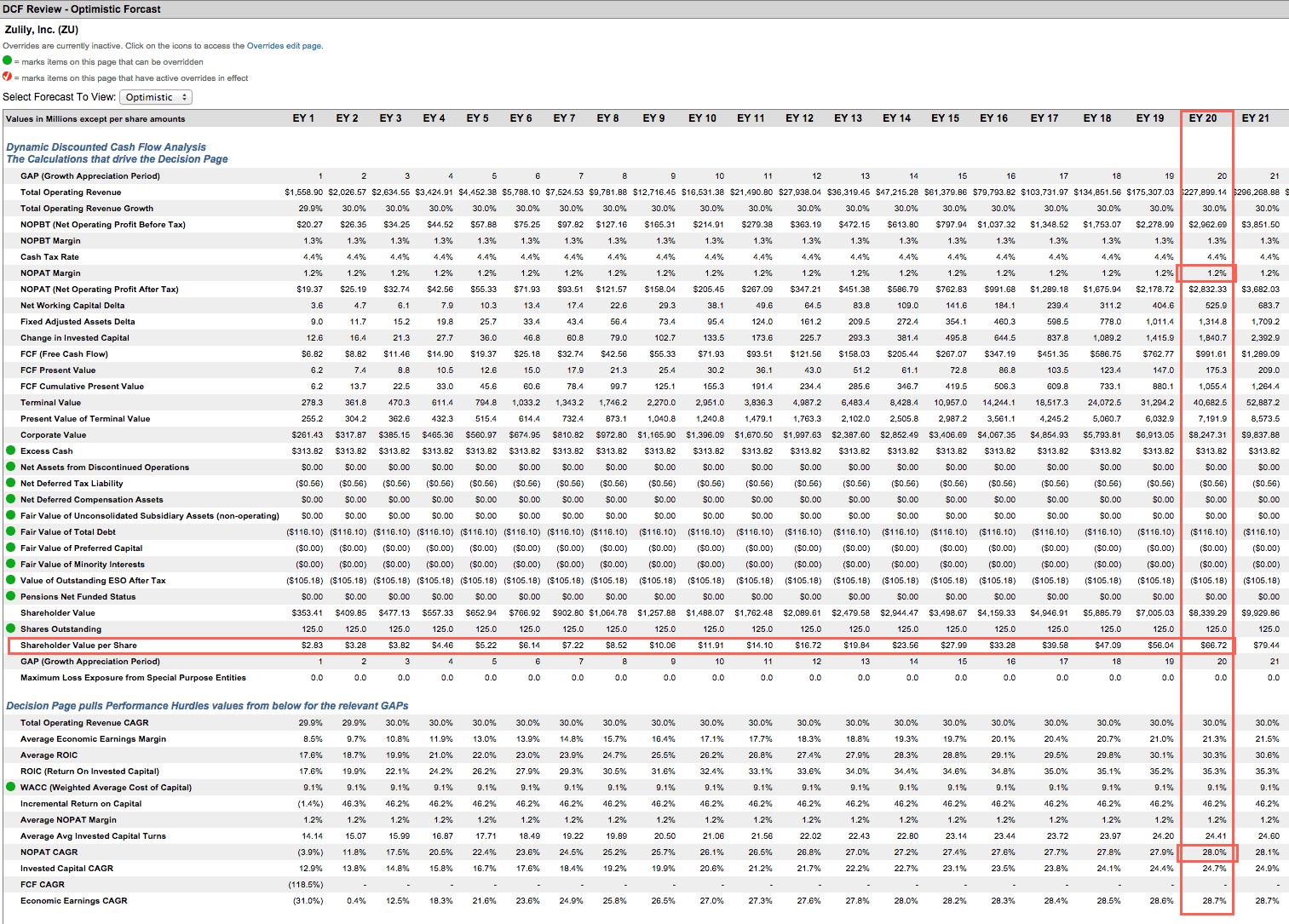

Zulily (ZU) — Down 37% from IPO price and 73% in the past 12 months

Zulily (ZU) is similar to GoPro in that while the company makes money and is financially stable, the stock’s valuation made little sense after its IPO. Zulily sells clothing and baby products to expectant or current mothers and uses social media advertising to drive sales and create a sense of community. The company IPO’d at $22/share in November 2013 and now trades at $14/share.

Much like GoPro, Zulily has an excellent ROIC of 29% and almost doubled its sales in 2014. However, the stock’s top of $68/share in February 2014 implied expectations of 28% annual profit growth for each of the next 20 years, or almost $4 billion in profit! That’s far more than Amazon’s (AMZN) current $304 million.

When Zulily’s growth began to slow and investors came to their senses, the company’s stock tanked and is now down 73% in the past year. However, even at its current price of $14, the company still must grow NOPAT by 19% compounded annually for the next 18 years to justify its valuation. We hope this scenario conveys how incredible ZU’s valuation was just six months ago, and still is today.

{kind=link}

Again, while Zulily is not a bad company, the initial pricing of the IPO made little sense, and the hype surrounding the IPO drove the stock to valuations that were out of touch with reality.

These Companies Often Make Little Business Sense

Wayfair (W) — Down 7% since our call on March 30

Wayfair is one of the world’s largest online retailers dedicated to home décor and products. The company sells furniture, kitchenware, bed and bath products, and other housewares. Wayfair’s “special sauce” is its proprietary technology that mostly eliminates the need for inventory and allows it to ship orders directly from its suppliers.

Wayfair went public in October for $29/share in an IPO that was largely overshadowed by the Alibaba (BABA) IPO. Shares are currently at $31. Not only would you have made little on your initial investment at this point, but you would also have lost 6% since our call last week.

There are common threads amongst all of these IPOs that make them bad investments, and Wayfair is no exception. Wayfair reminded us of Box (BOX) in many ways, and we’ll talk more about Box in a moment. We’re seeing many of the same warnings signs in Wayfair.

While we expect businesses like Wayfair to burn a little more money in pursuit of such high growth rates, Wayfair’s losses are alarming. The company’s NOPAT declined from -$14 million in 2013 to -$143 million in 2014. These increasing losses caused Wayfair’s ROIC to fall from -24% in 2013 to -76% in 2014.

It’s extremely easy to go on Wayfair, find an item, and find the exact same item offered at a lower price with free shipping on Amazon. In addition, while shipping at Wayfair takes around three days to start and a week to deliver due to the company’s “unique” fulfillment model, Amazon will ship your item in two days flat — guaranteed. Wayfair even admits in its filing on page 13 that its competitors have superior shipping terms.

It seems as if companies are arising to fill niches in the market that don’t even need to be filled. Easy venture capital means that anyone with a somewhat original idea can find funding.

The IPOs are Cash Grabs Not Only for Failing Companies…

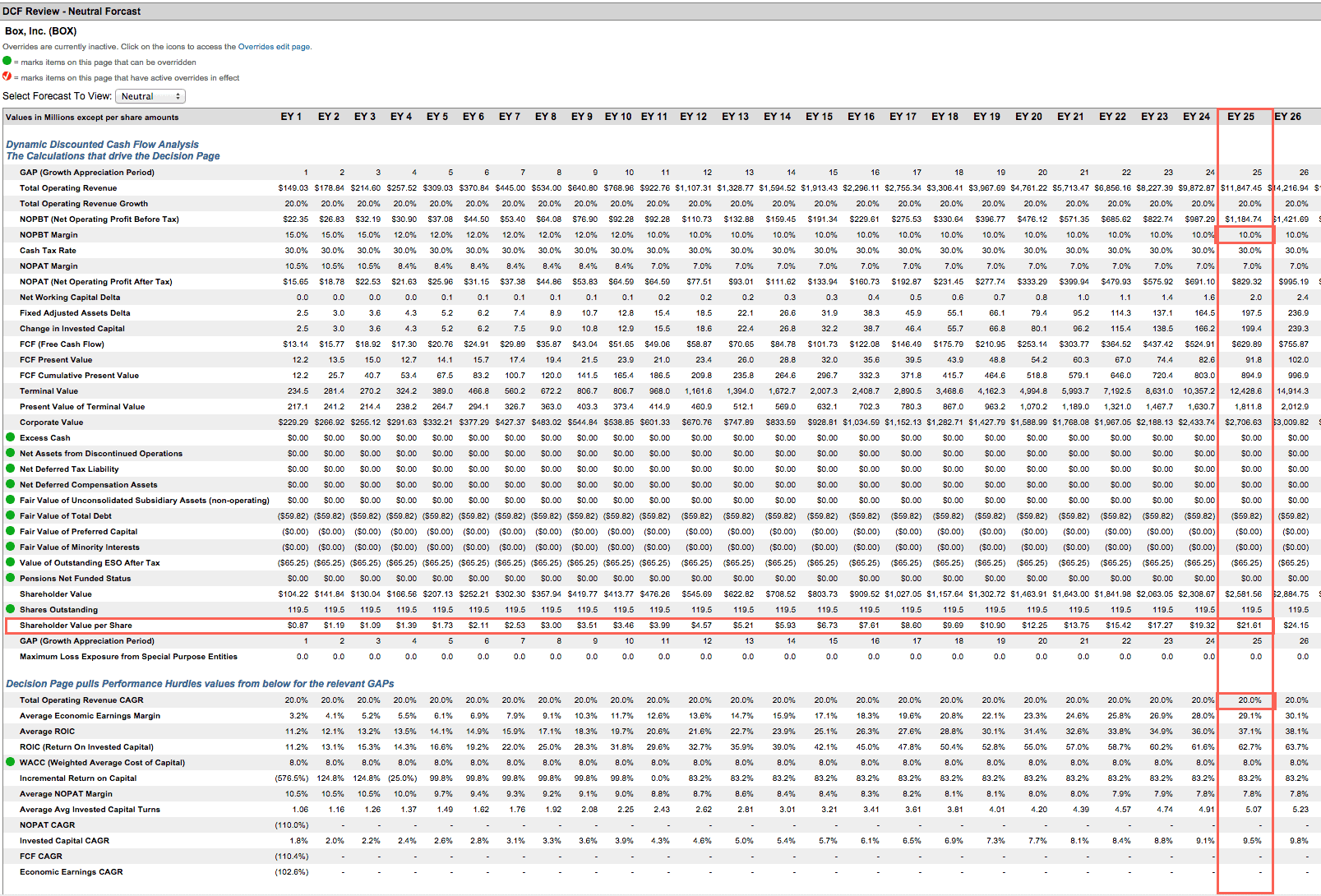

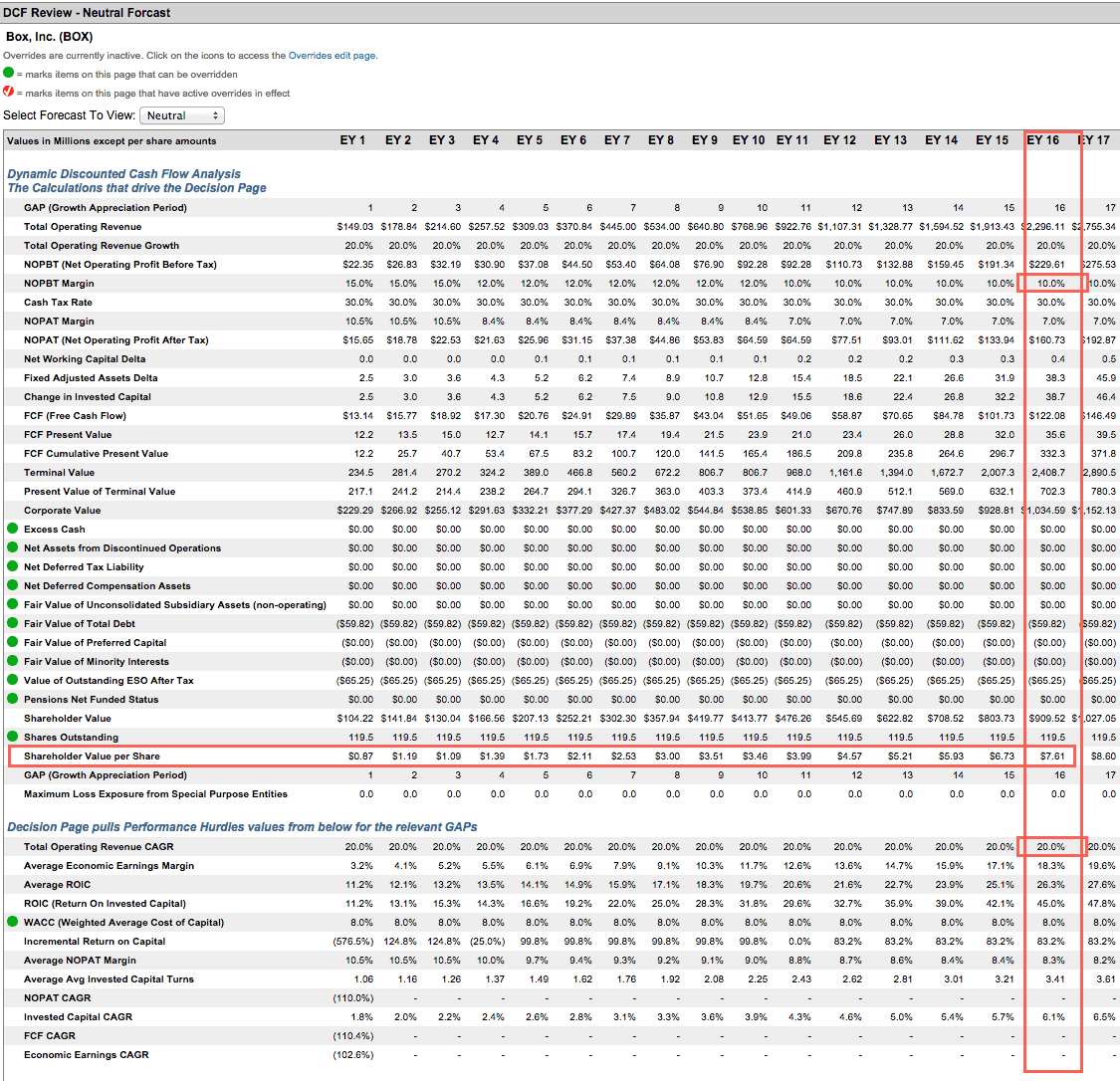

Box (BOX) — Down 18% since our call on Jan. 27

It’s easy to see why Box (BOX) went public — it’s bleeding cash at an alarming rate and it needed more. Many investors are placing their bets that Box will supplant Dropbox as the preferred file and document storage service. However, these investors are ignoring the reality of Box’s industry and the danger of its current valuation. Box is down 18% since our call on Jan. 27.

In 2014 Box earned a NOPAT of -$156 million, worse than the -$108 million the year before. This loss gives Box a ROIC of -100%. In other words, for every dollar invested into its business, the Box burns another dollar. Not exactly an encouraging sign for shareholders.

It’s difficult to see how Box is differentiating itself in the crowded and competitive cloud storage and management sector. Box has some features common to Dropbox, like its free storage options, and some to Google (GOOGL) Drive, like its collaboration tools. Box’s enterprise focus mirrors that of Microsoft’s (MSFT) OneDrive as well. Privately held Dropbox claims about 300 million users, while Google Drive claims 240 million and OneDrive over 250 million. These user numbers dwarf Box’s 32 million.

To justify its current valuation of $18/share, Box must increase its pre-tax margins to 10% (from their current level of -127%) and grow revenue by 20% compounded annually for the next 24 years. Under this scenario, Box would be earning an average ROIC of 36%, greater than that of Google, Amazon and IBM. There is no reason to make such a risky bet on this company with so many other good tech companies out there.

{kind=link}

Even if we lower expectations, it’s not a bright picture. If Box can increase its margins to 10% and grow revenue by 20% compounded annually for the next 16 years, the company is worth less than $8/share, a 56% downside.

{kind=link}

Box’s industry has a low barrier to entry and just about every large tech company is dipping their toes into this water. The problem with this scenario is that Box’s valuation would imply incredibly high barriers to entry, as indicated by the high ROICs and sustained revenue growth in the above scenarios.

During the tech bubble, there was a practice known as “IPO flipping.” Financial institutions, which received the lion’s share of IPO allocations, would sell when they felt like the stock had run its course. The unloading of all of these shares into the open market creates a demand-supply imbalance, and share prices fall. There are new rules limiting how quickly institutions can dump their shares, but this still appears to be a likely catalyst for not only Box but also for our next company on this list…

…But Also for Insiders and Private Equity Firms

GoDaddy (GDDY) — The next to crash?

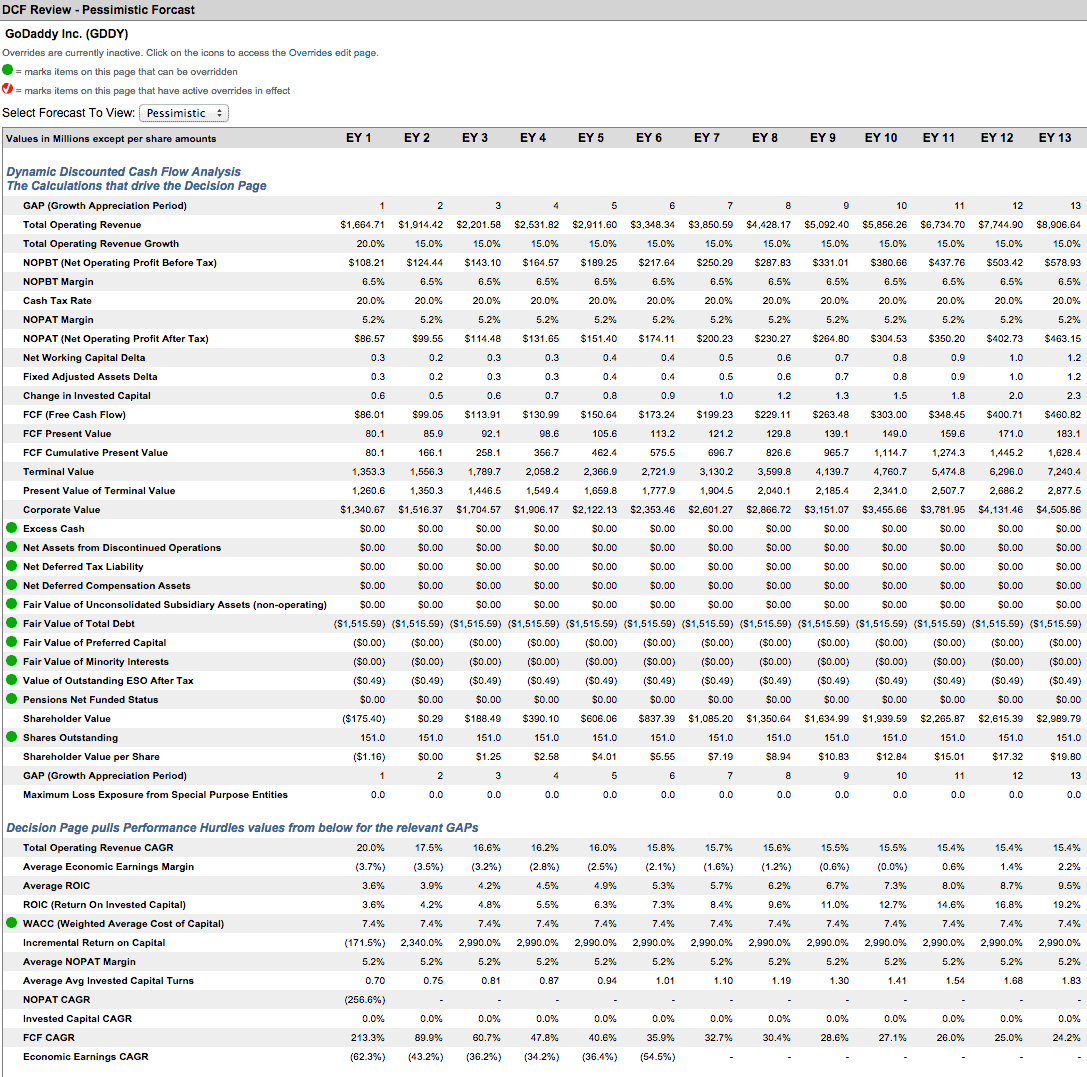

In comparison to the other companies on this list, GoDaddy most resembles GoPro and Zulily. It has decent fundamentals and should become profitable in the near future, but the stock’s valuation is just too high to justify buying in at these levels.

This is GoDaddy’s third attempt at an IPO. The last time the company tried to go public in 2006, it failed not because of lack of interest but because the CEO couldn’t abide by the SEC’s mandatory quiet period, which is a regulatory condition placed on companies to keep them from hyping their own stock. Essentially, because the CEO couldn’t drive up the valuation of his company and his existing stake after the IPO, he didn’t see any point in going public.

The company is currently nearing break-even after being in business for 18 years, and NOPAT rose from -$124 million in 2012 to -$55 million in 2014. We think GoDaddy may become profitable in the near future.

However, you should take a read at the incentives for previous owners below, and decide for yourself if you want to take a bite out of this stock at its current valuation.

In 2011, three private equity funds — KKR, Silver Lake and TCV — acquired around 69% of GoDaddy for an estimated $2.5 billion. These funds offered GoDaddy’s stock to the public in an “Up-C structure,” in which investors will be offered stock in the new company after it has bought the assets of the old company, Desert Newco.

This complicated structure will provide tax benefits for the funds mentioned above and will lower GoDaddy’s tax liability by creating an intangible asset on the balance sheet of the new company. This structure involves higher IPO costs that will be reduced by the expected proceeds of the IPO. The burden for the IPO is essentially being shifted from the owners of the company to investors,

In addition, the company’s S-1 showcases other favorable terms for existing stakeholders:

- CEO Bob Parsons will receive a $3 million services-agreement termination fee, per the Wall Street Journal.

- KKR, TCV, and Silverlake will keep their stakes in GoDaddy and will receive $26 million to terminate their management agreement with the company.

It becomes easy to see this IPO as an opportunity for private equity to exit and take a payday while IPO appetites are high due to excess liquidity. These private equity firms and insiders got what they wanted, as the stock popped 30% on the first day of trading. These companies have been milking GoDaddy for some time, as each received a portion of a $350 million dividend back in May 2014, which pushed GoDaddy’s debt up to $1.5 billion.

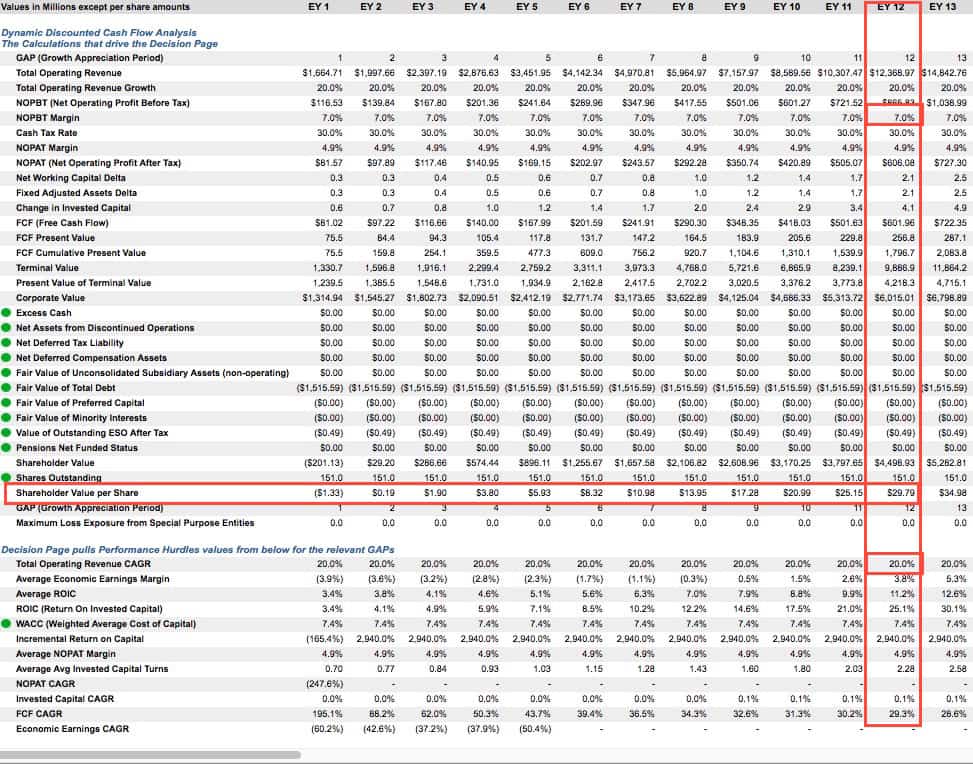

All told, to justify its current valuation of $27/share, GoDaddy must immediately achieve pre-tax margins of 7% (equal to that of Web.com, its closest competitor) and grow revenue by 20% compounded annually for the next 12 years. This is a level of growth only a handful of companies have been able to achieve.

{kind=link}

If GoDaddy can still achieve the same margins but grow revenue at a slightly more realistic 15% compounded annually over the next 12 years, the stock is worth $17/share, a 37% downside. We see this kind of expectation adjustment happening within the next year.

{kind=link}

Despite These Disasters, the IPOs are Still Coming

Etsy (ETSY), an online arts and crafts marketplace is going public with a $1.8 billion valuation and “behavioral matchmaking” dating site Zoosk both plan to go public later this year. Hopefully investors will have learned their lesson from these examples in the past 12 months that we’ve just discussed and learn to look for the warning signs that continually repeat themselves during tech IPOs.

Disclosure: David Trainer and André Rouillard receive no compensation to write about any specific stock, sector, or theme.

Photo credit: Parker Anderson