Most investors know that GAAP earnings are prone to distortion because they include unknown amounts of unusual gains/losses. However, most investors are not aware that legacy metrics like Street Earnings (from Refinitiv) and Operating Earnings (from S&P Global (SPGI)) still miss about $0.45 out of every $1.00 of unusual gains/losses (hidden and reported) – as detailed in section 5.1 of the new paper from HBS & MIT Sloan: Core Earnings: New Data & Evidence. This paper also uses our new, advanced measure of Core Earnings to prove the market is inefficient at reflecting unusual gains/losses buried in footnotes.

Investors armed with our measure of Core Earnings have a differentiated and more informed view of the fundamentals and, therefore, the valuation of markets and stocks.

A New View on Earnings…and Valuation

The precipitous fall expected in 2Q20 earnings significantly understates the true, core earnings of U.S. companies because these earnings metrics are not adjusted for unusual gains/losses.

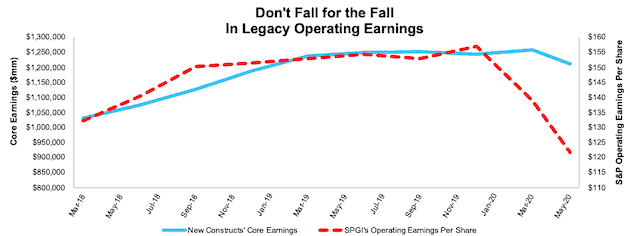

Figure 1 compares the steep fall expected in consensus estimates for S&P Global’s Operating Earnings[1] to our more normal Core Earnings[2]. Specifically, the trailing-twelve-month (TTM) Core Earnings[3] for the S&P 500 show a 2% fall since 2019 while consensus predicts a 22% fall. Investors would be well-served to see through the dip in SPGI’s operating earnings metrics, especially when it comes to valuation, as shown in Figures 3 and 4.

Figure 1: Core Earnings vs. SPGI’s Operating Earnings for the S&P 500: 2018-Present

Sources: New Constructs, LLC, company filings, and S&P Global (SPGI). Note: the most recent periods’ data for SPGI’s Operating Earnings is based on consensus.

Our Core Earnings analysis is based on aggregated quarterly data for the S&P 500 constituents in each measurement period.

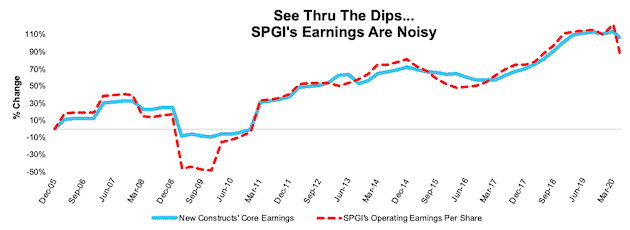

Figure 2 further demonstrates the more normal and reliable nature of our Core Earnings compared to S&P Global’s (SPGI) Operating Earnings over a longer term, including the Financial Crisis.

Figure 2: Core vs. SPGI’s Operating Earnings for the S&P 500 – % Change: 2005 – Present

Sources: New Constructs, LLC, company filings, and S&P Global (SPGI).

Note: the most recent periods’ data for SPGI’s Operating Earnings is based on consensus.

Our Core Earnings analysis is based on aggregated quarterly data for the S&P 500 constituents in each measurement period.

Better Earnings for Valuing the S&P 500

Not only is the market more profitable than Wall Street would have you believe, but it is also cheaper.

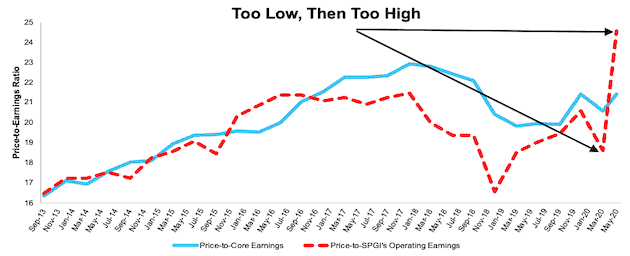

Per Figure 3, analyzing the price-to-earnings (P/E)[4] of the S&P 500 based on our Core Earnings shows how much investors oversold in March and that, despite the recent rebound, the S&P 500 remains very reasonably valued compared to the past few years.

Figure 3: Price-to-Core vs. Price-to-SPGI’s Operating Earnings for the S&P 500: 2013 – present

Sources: New Constructs, LLC, company filings, and S&P Global.

P/E ratios are based on four quarters of aggregated S&P 500 constituent results in each period. More details in Appendix.

In contrast, valuing the S&P based on SPGI’s Operating Earnings suggests the market is more highly valued than any time since the Financial Crisis (see Figure III in the Appendix).

We believe there’s upside left in this market.

Core Earnings Proven More Reliable in the Financial Crisis

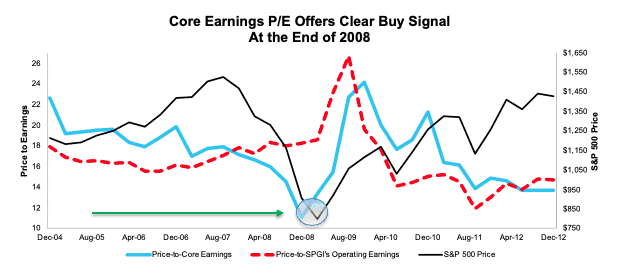

Figure 4 points out the clear buying signal provided by our Core Earnings P/E during the market crash in the Financial Crisis. Figure 3 presents a similar pattern and buying signal. Note the similarity between now and 2008 in the spiking of the P/E based on SPGI’s Operating Earnings compared to the more normal Core Earnings P/E.

Figure 4: Price-to-Core vs. Price-to-S&P Operating Earnings: 2004-2012

Sources: New Constructs, LLC, company filings, and S&P Global.

Note that the SPGI P/E is based on four quarters of aggregated S&P 500 results in each period. Core Earnings P/E is based on annual data.

How You Can Make Money with Our Core Earnings

Passive investing has become a very crowded trade, and now is the best time in many, many years for investors to pick individual stocks, especially those armed with differentiated insight into earnings.

Table 1 lists the stocks with links to reports showing how they are among the most attractive in the market based on strong Core Earnings growth and valuations at historic discounts. Most of these picks have significantly outperformed the S&P 500 and remain undervalued.

We recommend investors consider putting money into these stocks and believe they have even more upside potential than the S&P 500 or any other index.

Table 1: Stock Picks in Today’s Market

| Company | Ticker | Publish Date | Performance vs S&P 500 (as of 6/23) |

| SYSCO Corporation | SYY | 4/15/20 | 14% |

| Simon Property Group | SPG | 4/20/20 | 19% |

| Darden Restaurants | DRI | 4/22/20 | -2% |

| D.R. Horton | DHI | 4/27/20 | 25% |

| Southwest Airlines | LUV | 5/4/20 | 16% |

| Omnicom Group | OMC | 5/6/20 | -10% |

| Hyatt Hotels | H | 5/14/20 | 4% |

| Allstate Corp | ALL | 5/18/20 | -8% |

| JPMorgan Chase & Company | JPM | 5/21/20 | 2% |

| Caterpillar | CAT | 5/27/20 | 0% |

Sources: New Constructs, LLC

You can find more recent reports like these in our Long Ideas.

This article originally published on July 10, 2020.

Disclosure: David Trainer owns SYY, SPG, DHI, LUV, JPM, and H. David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

Appendix I: P/E Ratio Methodology for Core & SPGI’s Operating Earnings

In the analysis above, we calculate the price-to-Core Earnings ratio as follows:

- Calculate a trailing four quarters earnings yield for every S&P 500 constituent

- Weight the earnings yield by each stock’s respective S&P 500 weight

- Sum the weighted earnings yields and take the inverse (1/Earnings Yield)

This method allows us to capture the impact of changes to S&P 500 constituents on a quarterly basis. For example, a company could be a constituent in 2Q18, but not in 3Q18. This method captures the continuously changing nature of the S&P 500 constituency.

We use the earnings yield methodology because P/E ratios don’t follow a linear trend. A P/E ratio of 1 is “better” than a P/E ratio of 30, but a P/E ratio of 30 is “better” than a P/E ratio of -15. In other words, aggregating P/E ratios can result in a low multiple due the inclusion of just a few stocks with negative P/Es.

Using earnings yields solves this problem because a high earnings yield is always “better” than a low earnings yield. There is no conceptual difference when flipping from positive to negative earnings yields as there is with traditional P/E ratios.

For all periods in the above analysis, we calculate the price-to-SPGI’s Operating Earnings ratio by summing the preceding 4 quarters of Operating Earnings per share and, then, dividing by the S&P 500 price at the end of each measurement period.

Figures I and II show the price-to-Core Earnings ratio using TTM data for the companies in the S&P 500. Price-to-SPGI’s operating earnings are always calculated in the manner defined above because we do not have access to TTM Operating Earnings data for S&P 500 constituents. In these Figures, we calculate the price-to-Core Earnings ratio as follows:

- Calculate a TTM earnings yield for every S&P 500 constituent

- Weight the earnings yields by each stock’s respective S&P 500 weight

- Sum the weighted earnings yields and take the inverse (1/Earnings Yield)

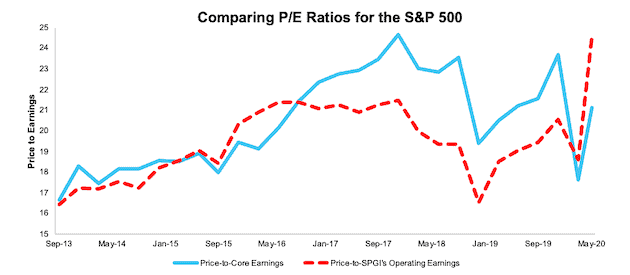

Figure I: Price-to-Core vs. Price-to-SPGI’s Operating Earnings: TTM 9/30/13 – present

Sources: New Constructs, LLC, company filings, and S&P Global.

Note that the Core Earnings P/E ratio is aggregating the TTM results for constituents in each period.

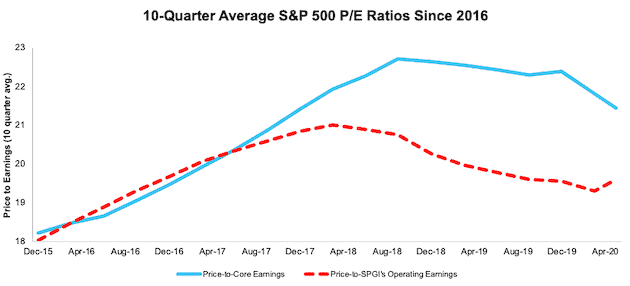

Figure II: Price-to-Core vs. Price-to-SPGI’s Operating Earnings: TTM 10 Quarter Average

Sources: New Constructs, LLC, company filings, and S&P Global.

Note that the Core Earnings P/E ratio is aggregating the TTM results for constituents in each period.

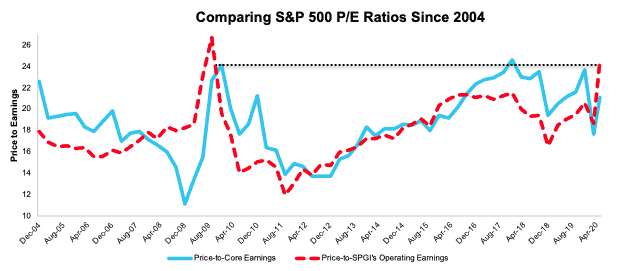

Figure III compares the price-to-Core Earnings and price-to-SPGI’s Operating Earnings ratios dating back to 2004. SPGI’s Operating Earnings suggest the S&P 500 is more highly valued than it has been since the Financial Crisis.

Figure III: Price-to-Core vs. Price-to-SPGI’s Operating Earnings: Since 2004

Sources: New Constructs, LLC, company filings, and S&P Global.

Note that the SPGI P/E is based on four quarters of aggregated S&P 500 results in each period. Core Earnings P/E is based on annual data.

[1] We think SPGI’s Operating Earnings provide the best available comparison for our Core Earnings. We can compare with any other metrics.

[2] For 3rd-party reviews on the benefits of adjusted Core Earnings, historically and prospectively, across all stocks, click here and here.

[3] Our Core Earnings data is based on all 10-Q and 10-K filings for S&P 500 constituents as of 5/26/2020. Since then, an immaterial number of companies (18) companies have filed a new 10-K or 10-Q with the SEC. Contact us at support@newconstructs.com for access to the source data behind this research.

[4] The methodology for calculating an apples-to-apples price-to-Core Earnings and price-to-SPGI’s Operating Earnings is in Appendix I.