For the week of 7/13/20-7/17/20, we focus on the Earnings Distortion Scores for 44 companies.

Our Earnings Distortion Scores[1] empower investors to make smarter investments with superior data as well as defend against management efforts to obfuscate financial performance.

Our proprietary measure of earnings distortion (as featured on CNBC Squawk Box) leverages proprietary data featured in Core Earnings: New Data & Evidence. This paper shows that our adjusted core earnings are:

- more accurate than “Operating Income After Depreciation” and “Income Before Special Items” from Compustat, owned by S&P Global (SPGI) and

- remove significant bias from IBES Street Earnings from Refinitiv, owned by owned by Blackstone (BX) and Thomson Reuters (TRI).

COVID-19 is not disrupting our data collection and research. Our Robo-Analyst is more effective than ever.

Weekly Earnings Distortion Insights

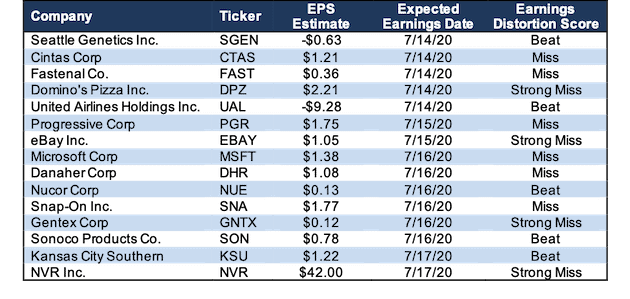

Figure 1 contains the 15 largest (by market cap) companies that earn a “Beat”, “Miss”, or “Strong Miss” Earnings Distortion Score and are expected to report the week of July 13, 2020.

Figure 1: Earnings Distortion Scorecard Highlights: Week of 7/13/20-7/17/20

Sources: New Constructs, LLC and company filings

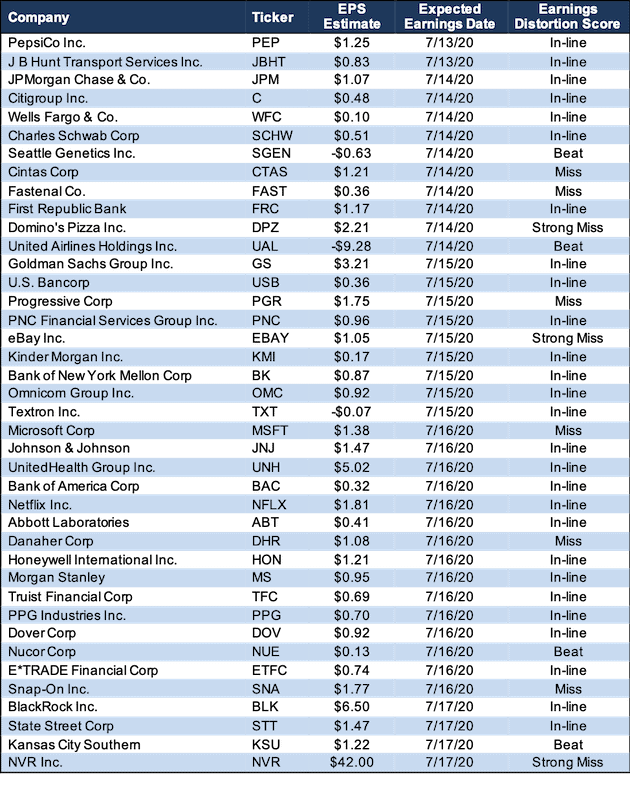

The appendix shows the Earnings Distortion Scores for all the S&P 500 companies, plus those with market caps greater than $10 billion, that are expected to report the week of July 13, 2020.

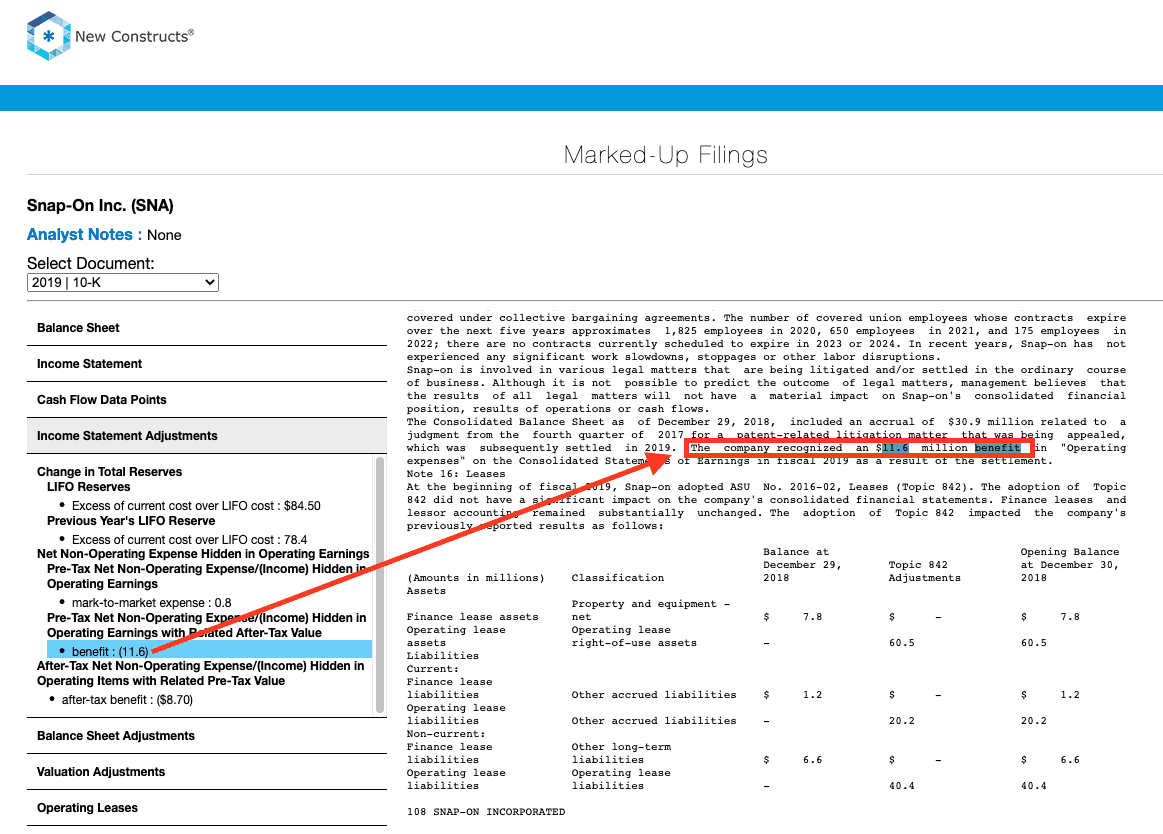

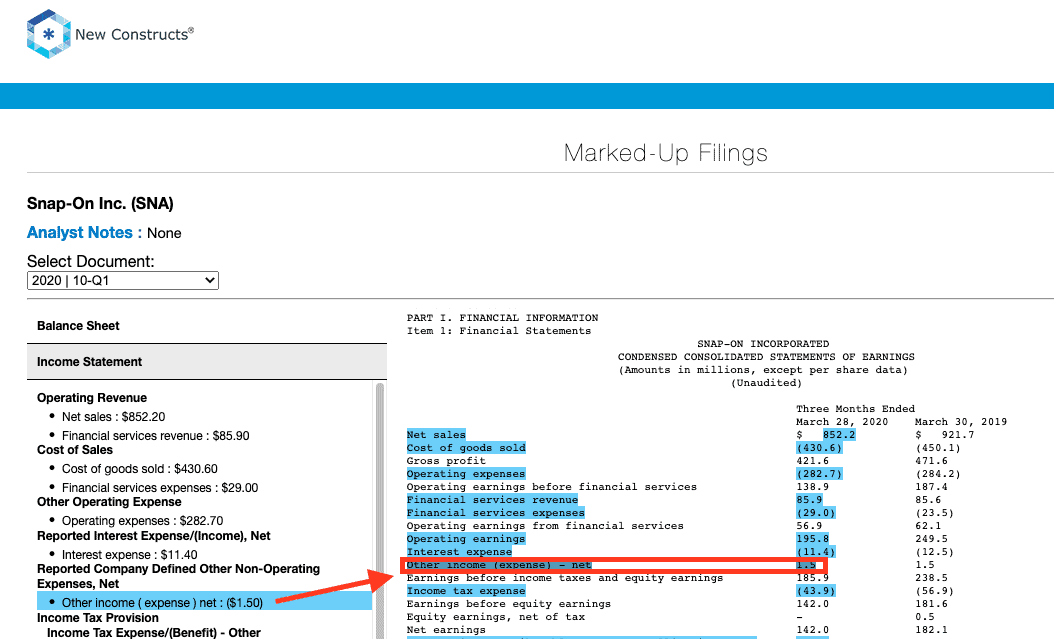

Details: Snap-On Inc. (SNA): Earnings Distortion Score: Miss

Over the trailing-twelve months (TTM), Snap-On had $14 million in net earnings distortion that cause earnings to be overstated by $0.25/share. Notable unusual income hidden and reported in Snap-On’s filings include:

- $12 million in non-operating income recognized in “Operating expenses” as a result of the settlement of a patent-related litigation matter – 2019 10-K page 108

- $2 million in other income reported on the income statement – 1Q20 10-Q

{kind=link}

{kind=link}

In addition, we made a $9.7 million adjustment for income tax distortion. This adjustment normalizes reported income taxes and removes the impact of unusual items on the taxes applied to core earnings.

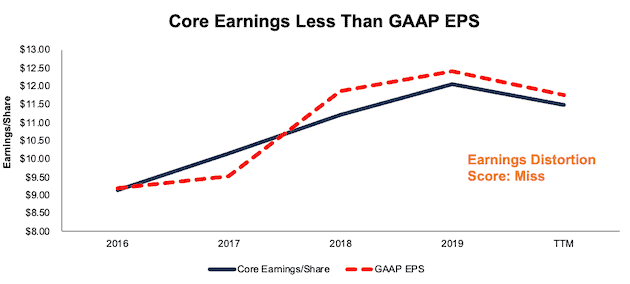

In total, we identified $0.25/share (2% of GAAP EPS) in net unusual income that cause Snap-On’s TTM GAAP results to be overstated. After removing this earnings distortion, Snap-On’s TTM core earnings of $11.49/share are less than GAAP EPS of $11.75, per Figure 2.

With overstated earnings, Snap-On gets our “Miss” Earnings Distortion Score and is likely to miss consensus expectations. While Snap-On looks more likely to miss upcoming estimates, we are more optimistic about the company’s long-term prospects. The firm’s rising economic earnings, high return on invested capital (ROIC), and cheap valuation earn it our Attractive Risk/Reward rating, which focuses on the long-term.

Figure 2: Snap-On Core Earnings Vs. GAAP: 2016 - TTM

Sources: New Constructs, LLC and company filings

Figure 1 shows that Snap-On is one of ten companies that earn our “Strong Miss” or “Miss” score for this week.

How to Make Money with Earnings Distortion Data

“Trading strategies that exploit {adjustments provided by New Constructs} produce abnormal returns of 8% per year.” – Page 1 in Core Earnings: New Data & Evidence

In Section 5.2, professors from HBS & MIT Sloan present a long/short strategy that holds the stocks with the most understated EPS and shorts the stocks with the most overstated earnings.

This strategy produced abnormal returns of 8% a year. Click here for more details on our data offerings.

We Provide 100% Audit-ability & Transparency

Clients can audit all of the unusual items used in our calculations in the Marked-Up Filings section of each of our Company Valuation models. We are 100% transparent about what goes into our research because we want investors to trust our work and see how much goes into building the best earnings quality and valuation models.

This article originally published on July 6, 2020.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, sector, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

Appendix: All Major Companies Expected to Report July 13 – July 17

Figure 3 shows all the S&P 500 companies, plus those with market caps greater than $10 billion, that are expected to report the week of July 13, 2020.

Figure 3: Earnings Distortion Scorecard: Week of 7/13/20-7/17/20

Sources: New Constructs, LLC and company filings

Figure 3: Earnings Distortion Scorecard: Week of 7/13/20-7/17/20 (continued)

Sources: New Constructs, LLC and company filings

[1] Earnings Distortion scores on ~3,000 stocks are also available to clients of our website.