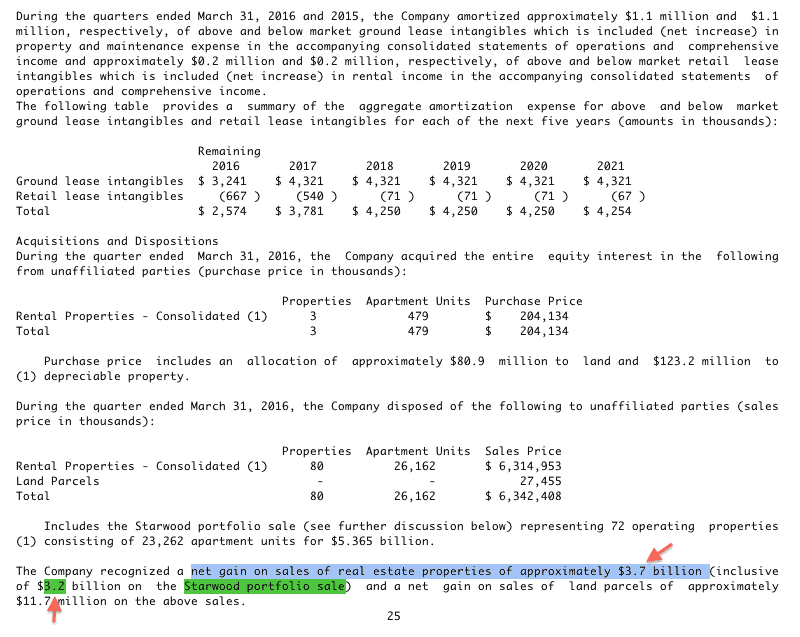

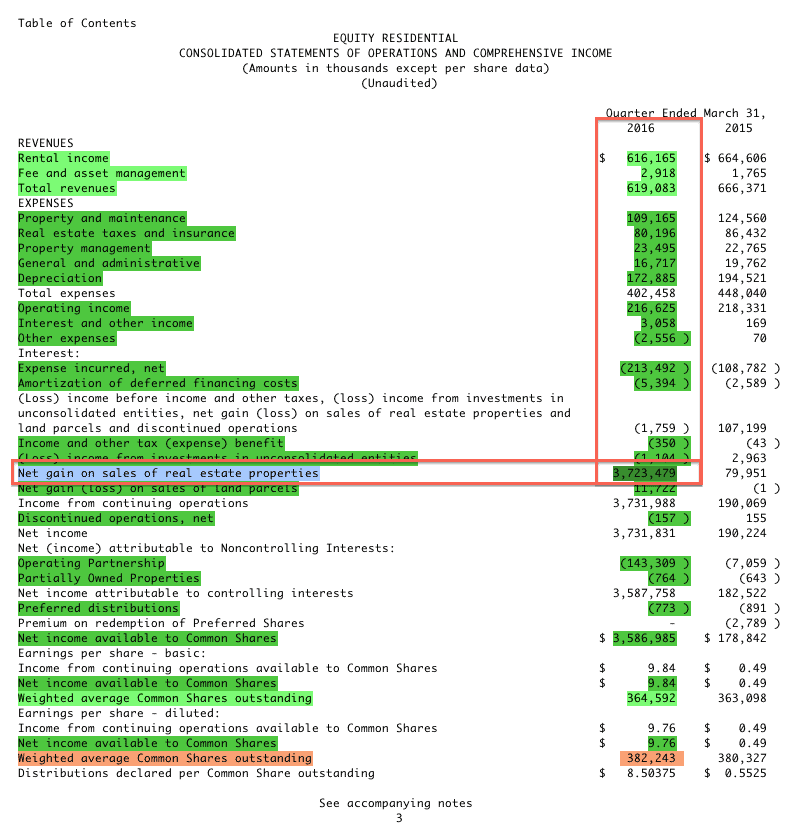

New Constructs has suspended the rating for Equity Residential (EQR) due to an abnormally large gain on the sale of real estate properties. The $3.7 billion gain is comprised of $3.2 billion net gain on the sale of the Starwood portfolio as well as roughly $500 million in other undisclosed gains. Normally, property sales are treated as a recurring component of operations for this type of REIT, which we call “Equity REIT”. However, the low likelihood of EQR realizing consistent gains of this magnitude in the future has influenced our decision to remove the bulk of the gain from Net Operating Profit After Taxes (NOPAT).

{kind=link}

{kind=link}

While we are able to remove the net gain on the sale of the Starwood portfolio ($3.2 billion) from NOPAT, the rest ($500 million) remains because the lack of additional disclosure regarding which parts are not normal requires treating the gain as operating. Without knowing exactly of the $500 million is (operating/non-operating), we cannot be sure what the exact right number is. Rather than remove the entire amount and show an overly negative view of the business, we leave the $500 in NOPAT and provide this additional disclosure for clients.

Removing the remaining $500 million would bring EQR’s NOPAT down from $1.8 billion to $1.3 billion, a 27% drop. NOPAT growth, the numerator of Return On Invested Capital (ROIC), is driven primarily by this undisclosed gain. Additionally, the disposition of Starwood assets has marginally reduced Invested Capital, the denominator of ROIC, resulting in an inflated ROIC metric. Because of these factors, we have opted to suspend our rating for this quarter.

Disclosure: David Trainer, Lindsay Bohannon, and Kyle Martone receive no compensation to write about any specific stock, sector, or theme.