Free cash flow (FCF) equals the amount of cash free for distribution to all stakeholders. Think of free cash flow as the real dividend that a company could pay investors as well as a truer proxy for the profitability of a business. Not surprisingly, many of the world’s top investors focus on free cash flow when picking stocks.

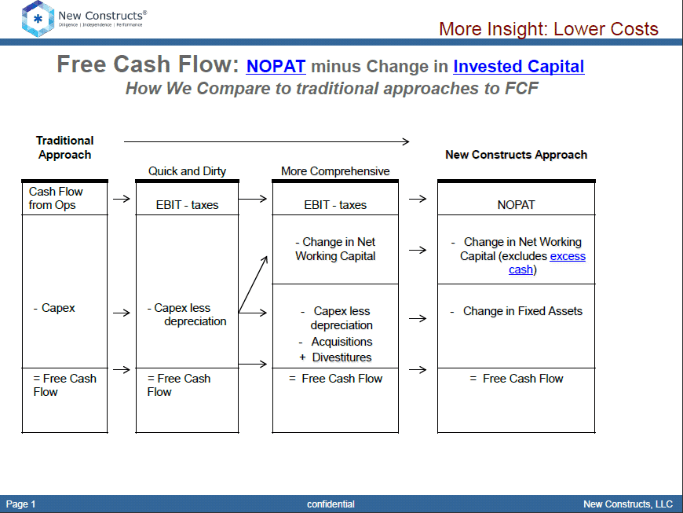

There are many ways to calculate free cash flow. Most approaches are short cuts to a more comprehensive approach to the calculation. Our formula for FCF is in Figure 1.

Figure 1: How to Calculate Free Cash Flow

NOPAT – Change In Invested Capital

Or

Sources: New Constructs, LLC and company filings

As with all things in life, building a solid investment strategy around Free Cash Flow (FCF) is not as simple as it may seem. While it is obvious that companies with larger and growing FCF should fetch higher valuations, making money with that strategy requires a bit more work.

Here are 3 rules to follow when building an investment strategy that uses FCF.

Updated_FCF_and_FCF_YieldRule #1: Cash is (not always) King

If you remember one thing from Accounting 101, it should be: Cash is King. Companies need cash to make, market, or distribute products and services.

However, not all cash flow metrics are made the same. Getting an accurate FCF takes lots of work so almost nothing you see on free websites is accurate. Be particularly wary of the FCF numbers that come from Wall Street, companies or anyone trying to sell you stock (See 3 Reasons Why Amazon’s “Cash Flow” Is A Trap). This paper, especially the Appendix, and these white papers show how much diligence goes into getting NOPAT and Invested Capital, the variables used to calculate FCF, right.

Make sure you can audit any cash flow numbers on which you based investment decisions. Otherwise, you could be making bets on bad information – more details below.

Rule #2: Cash may be King, but FCF yield is an Ace

Free Cash Flow is an important metric, but the level of FCF, by itself, does not provide enough information for an investment strategy. Per Valuation 101, smart investing is about buying low expectations and selling high expectations. We need a metric that tells how highly the market is valuing FCF. FCF Yield is the answer: the ratio of Free Cash Flow to a company’s enterprise value (FCF/Enterprise Value).

We can use the FCF Yield to rank all stocks on an apples-to-apples basis. We can also compare the FCF Yields to bond yields.

Rule #3: FCF yields > P/E multiples

Although they are beloved by the financial media, P/E multiples (price-to-earnings multiples) tell us little about a company. They are an oversimplified metric used to quickly estimate future performance.

FCF yield is an accurate measure of future company and stock performance because it is derived from two calculated accurate values: free cash flow and enterprise value.

Take the case of Hertz (HTZ). In early 2018, Hertz had a P/E multiple of just 6, well below the S&P 500 average of 22. However, as our article, “No Light at the End of the Tunnel for This Stock”, pointed out, this low P/E was based on overstated GAAP net income due to the impact of tax reform. HTZ’s negative free cash flow yield gave a more accurate picture of the true economics of the business.

In order to sustain its various business operations, Hertz must invest higher rates of its profits back into its business. In 2018, Hertz spent $12.5 billion on additions to its rental fleet, while depreciation and sales of its vehicle totaled $11 billion. The high capital cost of maintaining its rental fleet explains why Hertz’s total debt increased from $15.3 billion in 2015 to $20.7 billion in 2019.

In the 18 months after we published our Hertz article, the stock dropped 39% while the S&P 500 was up 7%.

But a P/E multiple wouldn’t have told you that, would it?

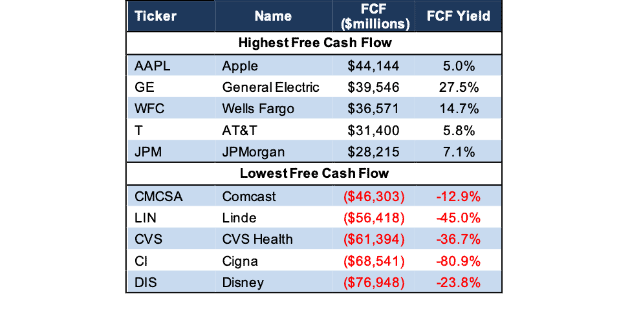

Companies with the Most Positive/Negative Free Cash Flow

Figure 2 contains the S&P 500 companies with the highest and lowest level of FCF and their FCF yields.

Figure 2: Companies with Most Positive/Negative FCF: Trailing Twelve Months as of September 2019

Sources: New Constructs, LLC and company filings

Carter’s has increased its annual dividend in each of the past five years. The annual dividend has grown from $0.76/share in 2014 to $1.80/share in 2018, or 24% compounded annually. Carter’s TTM dividend has totaled $1.90/share. CRI easily generates the cash flow needed to continue paying and growing its dividend. Since 2014, CRI has generated cumulative FCF of $938 million (22% of market cap) while paying $307 million in dividends.

Companies with FCF well in excess of dividend payments provide higher quality dividend growth opportunities because we know the firm generates the cash to support a higher dividend. On the other hand, the dividend of a company where FCF falls short of the dividend payment over time cannot be trusted to grow or even stay the same because of inadequate free cash flow.

Per Figure 2, Apple (AAPL) has the most free cash flow out of all companies under coverage over the trailing twelve months as of September. See Apple’s historical free cash flow, dating back to 2008, in our model here. You can see that each of the past 10 years, Apple has generated positive free cash flow, totaling to a cumulative $321 billion. As a company that generates massive profits and has relatively low capital requirements, Apple is one of the most consistent free cash flow generators around. The adjustments page in our model shows all the adjustments we make to get NOPAT and Invested Capital right for AAPL’s FCF calculation.

General Electric (GE), Wells Fargo (WFC), AT&T (T), and JPMorgan (JPM) round out the list of companies that generate the most FCF. Additionally, these companies earn a high free cash flow yield.

Disney (DIS) generates the least, or most negative, free cash flow of all companies under coverage over the trailing twelve months as of September. You can see DIS’s FCF dating back to 2007 here. Disney is a great example of why investors should not always rely on free cash flow in any given year to evaluate a stock. Over most of its history, Disney has generated lots of FCF. Over the trailing twelve months, the company has a negative free cash flow due to its ~$70 billion acquisition of 21st Century Fox. However, as we outlined in our article, “Too Many Positive Catalysts to Count for This Media Giant”, Disney has a solid track record of creating value for shareholders through acquisitions, and we think the company will eventually generate an ROIC > WACC on the capital invested in buying Fox. Accordingly, negative free cash flow can be good as long as the company can generate a return on invested capital (ROIC) above its cost of capital (WACC) on its investments.

The adjustments page in our model shows all the adjustments we make to get NOPAT and Invested Capital right for DIS’s FCF calculation.

Cigna (CI), CVS Health (CVS), Linde (LIN) and Comcast (CMCSA) round out the list of companies generating the least free cash flow.

Below, we show how our approach to free cash flow compares with traditional approaches. You can download a copy of this exhibit here.

Figure 3: The New Constructs Approach to Free Cash Flow

Sources: New Constructs, LLC and company filings

It is important to note, that the level of FCF does not always reflect the health of a business or its prospects. For example, a large amount of FCF can be a sign that a company has limited investment opportunities and, hence, limited growth prospects. On the other hand, negative FCF can be an attractive indication that a company has more investment opportunities than it can fund with internal cash flows. Zero FCF could mean that the company generates just enough cash to internally fund its growth opportunities.

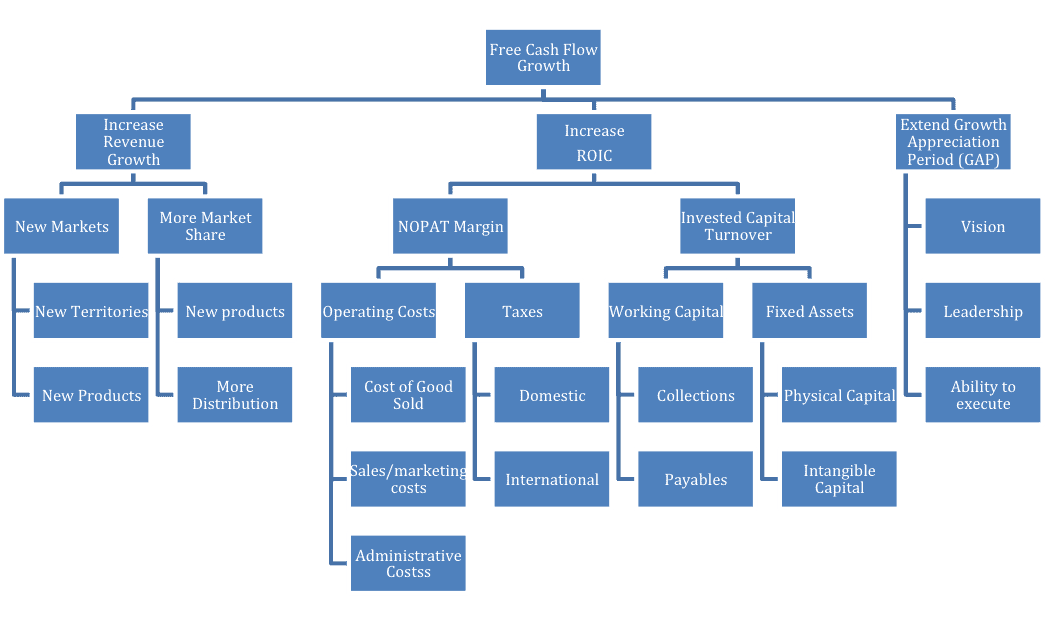

Whatever the level of free cash flows, investors benefit from (1) an accurate measure of free cash flow and (2) knowing the drivers of free cash flow. Figure 4 comes from our detailed reports on the importance of ROIC to valuation. Nearly every single activity within a for-profit business can be linked back to free cash flow, which drives valuation as explained in How New Constructs’ Reverse Discounted Cash Flow (DCF) Model Works.

Figure 4: Drivers of Free Cash Flow – Linking Strategy to Valuation

Sources: New Constructs, LLC and company filings

Whatever your opinion about the level of free cash flow, it is important that your calculation of it be as accurate as possible.

This article originally published on September 9, 2019.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

2 replies to "Free Cash Flow and FCF Yield"

Hi Sam,

Great article. Can you help me think this through…..in a nutshell, FCF is what can be spent by the company; however, depreciation is embedded in NOPAT. Depreciation is a non-cash item. As a result, if we’re calculating FCF, shouldn’t depreciation be added back in?

The New Constructs formulas does not do that. What’s the rationale behind that?

Thanks, Sherwin

Sherwin,

Thanks for your comment! We believe depreciation is a very real expense that is a good approximation for the future, recurring cash that will be required to keep a firm’s operations ongoing.