With the SEC’s Disclosure Update and Simplification (Release No. 33-10532; 34-83875; IC 33206; File No. S7-15-16), regulators reduce the disclosure requirements for companies and make it more difficult for investors to analyze the true financial health of publicly-traded companies. The goal of this report is to raise awareness for both regulators and investors of how this change in disclosure affects average investors.

The purpose of the Financial Accounting Standards Board (FASB) is to write and update Generally Accepted Accounting Principles (GAAP) or the rules that govern how publicly-traded companies report their financials. The role of the Securities and Exchange Commission (SEC) is to enforce those rules.

The integrity of the capital markets relies on the FASB and the SEC to do their jobs well. If FASB does not ensure that financial disclosures provide investors the information needed to make informed decisions or the SEC does not enforce compliance with GAAP’s disclosure rules, investors lose.

During my tenure on FASB’s Investor Advisory Committee, it was clear that companies often have more influence on FASB and the SEC than individuals because companies can consolidate more resources and present a more unified voice than investors. In addition, many of the potentially most influential investors prefer less informative financial disclosures because poorer disclosures further enhance their already-strong information advantages.

Background on The Change

The change made by the SEC is intended to reduce the cost of filing for reporting entities by eliminating what the SEC considers redundant or unimportant disclosures. However, one specific change in the Disclosure Update and Simplification eliminates an important disclosure – amortization of capitalized interest– which investors need to accurately assess earnings and cash flow.

SEC Reduced Disclosure Amendment

Effective November 18, 2018, the SEC adopted amendments to disclosure requirements that “have become redundant, duplicative, overlapping, outdated, or superseded, in light of other Commission disclosure requirements, U.S GAAP, or changes in the information environment.”

Through this amendment, the SEC eliminated the requirement that companies report the ratio of earnings to fixed charges exhibit. This exhibit contains a specific line item, amortization of capitalized interest, which is a non-operating expense included in operating earnings. We remove this expense when calculating after-tax operating profit (NOPAT) because it is related to the financing of a company’s operations, not the operations themselves, to provide a more accurate measure of normal, recurring profits.

Most of the time, interest costs are immediately expensed and (for non-financial companies) reported as non-operating. However, in certain cases where debt is used to finance a long-term asset, accrued interest can be capitalized on the balance sheet and expensed as amortization over time. As a result, GAAP allows the cost of interest to be classified as an operating expense, despite the fact that it is really a financing cost.

The SEC specifically noted in its final rule that:

“Certain components commonly used in the ratio of earnings to fixed charges, such as the portion of lease expense that represents interest and the amortization of capitalized interest, are not readily available elsewhere.”

Despite its acknowledgement that the exhibit contained material information not contained elsewhere, the SEC still decided to remove requirements to disclose this information.

Impact of This Change

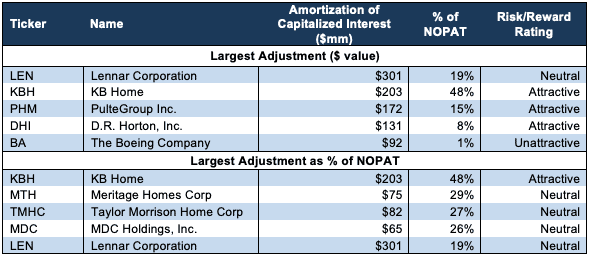

Figure 1 shows the five companies with the largest amortization of capitalized interest adjustment overall, and the five with the largest value as a percent of NOPAT. With the removal of this disclosure, we will no longer be able to make this adjustment for the majority of firms going forward.

Figure 1: Biggest Amortization of Capitalized Interest Adjustments in 2018

Sources: New Constructs, LLC and company filings

These companies, while largely homebuilders, are hardly the only ones whose reported earnings are affected by amortization of capitalized interest. In the past three years, our analysts, leveraging our Robo-Analyst technology, identified 327 amortization of capitalized interest adjustments across 166 different companies. In these three years, amortization of capitalized interest adjustments totaled $8.2 billion.

Many of the companies in Figure 1 are homebuilders, and the amortization of capitalized interest charge is materially greater in this industry than in others. As such, homebuilders have historically disclosed these charges in a section separate from the exhibit eliminated by the SEC. While positive for transparency, we would still prefer the SEC require all companies to present important financial information. Instead, the SEC is choosing to leave it up to management teams, which history shows are not afraid to exploit GAAP to manipulate earnings.

More Technology Not Less Disclosures Is the Answer

There’s no question that the growing volume of financial disclosures can be overwhelming to the average investor. However, the answer to this problem is not to reduce disclosures, especially since the growing complexities of businesses require more granular disclosures than ever. The answer to this problem is to leverage more technology to parse and analyze financial filings and disclosures more efficiently. Regulators are already under enough pressure to fulfill their obligations with limited resources. Without more technological support, we understand how there might be a natural tendency to want to reduce the disclosures they are required to review. We need to give regulators the support so it’s easier to focus more on serving the best interests of investors.

There’s no question that new technologies can aid regulators’ enforcement and analytical responsibilities. These new technologies enable machines, such as the Robo-Analyst featured by Harvard Business School, to perform certain tasks so humans can focus on higher level problems.

For example, we use machine learning and natural language processing tools to flag amortization of capitalized interest and other red flags hidden in the footnotes. These tools could help regulators better leverage human resources and protect the integrity of the capital markets.

This article originally published on July 15, 2019.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.