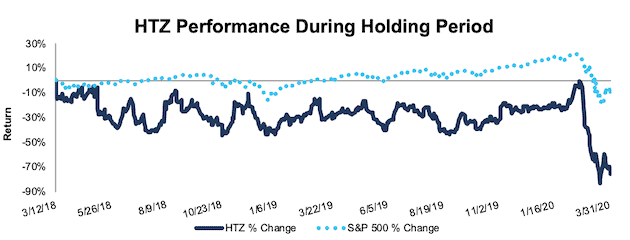

Hertz Global Holdings (HTZ) – Closing Short Position – down 75% vs. S&P down 9%

We put Hertz Global Holdings (HTZ: $5/share) in the Danger Zone on March 12, 2018. At the time, HTZ received a Very Unattractive rating. Our short thesis noted the firm’s falling net operating profit after-tax (NOPAT) and return on invested capital (ROIC), poor corporate governance, and overvalued stock price.

This Danger Zone report, along with all of our research, utilizes our “novel dataset”[1] of footnotes disclosures to get the truth about earnings, as shown in the Harvard Business School and MIT Sloan paper, “Core Earnings: New Data and Evidence.”

During the two-year holding period, HTZ outperformed as a short position, falling 75% compared to a 9% drop for the S&P 500.

HTZ’s fundamentals have improved since our original report. Its ROIC improved from 1% at the time of our report to 2% in 2019 while NOPAT margin increased from 2% to 6% over the same time. However, HTZ is down 68% year-to-date and, despite still being overvalued, this drop in valuation provides a great time to take the gains and close this short position.

Figure 1: HTZ vs. S&P 500 – Price Return – Successful Short Call

Sources: New Constructs, LLC and company filings

Note: Gain/Decline performance analysis excludes transaction costs and dividends.

This article originally published on April 3, 2020.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] In Core Earnings: New Data & Evidence, professors at Harvard Business School (HBS) & MIT Sloan empirically show that data is superior to IBES “Street Earnings”, owned by Blackstone (BX) and Thomson Reuters (TRI), and “Income Before Special Items” from Compustat, owned by S&P Global (SPGI).