The Financial Accounting Standards Board’s (FASB) Accounting Standards Update (ASU) 2017-12, reduces the disclosure requirements for companies and makes it more difficult for investors to analyze the true financial health of publicly-traded companies. The goal of this report is to raise awareness for both regulators and investors of how this change in disclosure affects average investors.

The purpose of the Financial Accounting Standards Board (FASB) is to write and update Generally Accepted Accounting Principles (GAAP) or the rules that govern how publicly-traded companies report their financials. The role of the Securities and Exchange Commission (SEC) is to enforce those rules.

The integrity of the capital markets relies on the FASB and the SEC to do their jobs well. If FASB does not ensure that financial disclosures provide investors the information needed to make informed decisions or the SEC does not enforce compliance with GAAP’s disclosure rules, investors lose.

During my tenure on FASB’s Investor Advisory Committee, it was clear that companies often have more influence on FASB and the SEC than individuals because companies can consolidate more resources and present a more unified voice than investors. In addition, many of the potentially most influential investors prefer less informative financial disclosures because poorer disclosures further enhance their already-strong information advantages.

Background on The Change

The change made by the FASB is intended to reduce the cost of filing for reporting entities, FASB parlance for companies, by eliminating what the SEC considers redundant or unimportant disclosures. However, the change eliminates an important disclosure – hedge ineffectiveness – which investors need to accurately assess earnings and cash flow.

ASU 2017-12

Effective for all public entities for fiscal years beginning December 15, 2018, ASU 2017-12 amended the hedge accounting recognition and presentation requirements. The stated goals of this change were to “provide users with a more complete picture of the effect of hedge accounting on an entity’s income statement and balance sheet” and to “ease the operational burden of applying hedge accounting by allowing more time to prepare hedge documentation.”

Through this amendment, firms are no longer required to separately measure and report hedge ineffectiveness. Hedge ineffectiveness is the degree to which a hedge fails to correlate with the underlying asset or forecasted transaction prices. For example, if a company hedged against falling commodity prices through a derivative contract, but then both the price of the commodity and the derivative fell, it would record a loss due to hedge ineffectiveness.

Hedge ineffectiveness was previously presented on the income statement in the period deemed ineffective. For non-financial companies, ineffectiveness is excluded from our calculation of NOPAT because it is a portion of the derivative contract that does not hedge the underlying asset and therefore serves no operating purpose. Accordingly, we classify ineffectiveness gains as non-operating income. If ineffectiveness is a loss, we still classify as a non-operating item, and we also classify as a write-down, which impacts reported assets and our calculation of invested capital.

The new amendment will cause significant reduction in the disclosure of hedge ineffectiveness. What would have been separately delineated as ineffectiveness will now be buried in other comprehensive income (OCI) until the entire hedge is recognized out of OCI and onto the income statement. When the hedge is re-classified from OCI into net earnings, it will be reported within the same line item as the hedged items, with no distinction between the ineffective and effective portion. This lack of delineation reduces transparency and analytical value of the financial statements.

This FASB amendment appears to prioritize reducing reporting entities’ burdens over providing investors with valuable disclosures.

Impact of This Change

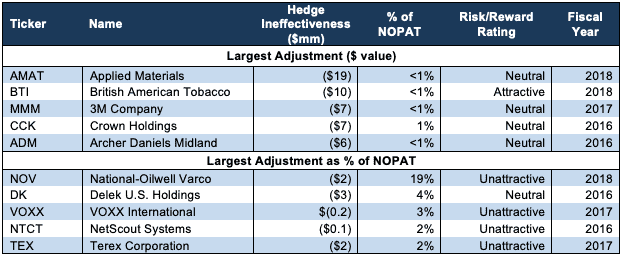

Figure 1 shows the five companies with the largest hedge ineffectiveness NOPAT adjustment and the five with the largest value as a percent of NOPAT.

Figure 1: Biggest Hedge Ineffectiveness Adjustments Over Past Three Years

Sources: New Constructs, LLC and company filings

In the past three years, we identified 50 NOPAT adjustments for hedge ineffectiveness across 34 companies. These adjustments totaled $182 million.

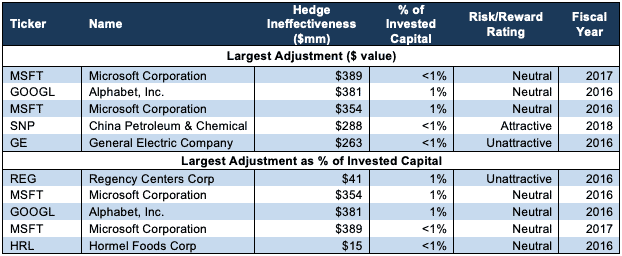

Figure 2 shows the five companies with the largest hedge ineffectiveness invested capital adjustment and the five with the largest value as a percent of invested capital. As can be seen, these adjustments are, on average, smaller than many of the other adjustments we make. However, in our experience, adjustments can go from immaterial to very material in any given reporting period.

Figure 2: Biggest Hedge Ineffectiveness Adjustments Over Past Three Years

Sources: New Constructs, LLC and company filings

In the past three years, we identified 148 invested capital adjustments for hedge ineffectiveness losses as write-downs across 96 different companies. In these three years, hedge ineffectiveness adjustments totaled $2.8 billion.

More Technology Not Less Disclosures Is the Answer

There’s no question that the growing volume of financial disclosures can be overwhelming to the average investor. However, the answer to this problem is not to reduce disclosures, especially since the growing complexities of businesses require more granular disclosures than ever. The answer to this problem is to leverage more technology to parse and analyze financial filings and disclosures more efficiently. Regulators are already under enough pressure to fulfill their obligations with limited resources. Without more technological support, we understand how there might be a natural tendency to want to reduce the disclosures they are required to review. We need to give regulators the support needed to make focusing more on serving the best interests of investors easier.

There’s no question that new technologies can aid regulators’ enforcement and analytical responsibilities. These new technologies enable machines, such as the Robo-Analyst featured by Harvard Business School, to perform certain tasks so humans can focus on higher level problems.

For example, we use machine learning and natural language processing tools to flag hedge ineffectiveness and other red flags hidden in the footnotes. These tools could help regulators better leverage human resources and protect the integrity of the capital markets.

This article originally published on July 15, 2019.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.