We published an update on this Danger Zone pick on August 22, 2022. A copy of the associated report is here.

Robinhood’s (HOOD: $14/share) 4Q21 earnings report underscores our thesis that the stock is wildly overvalued and could fall to as low as $6/share.

Robinhood went public at a valuation that implied its revenue would be larger than industry stalwart Charles Schwab (SCHW), but that growth has not materialized, not even close. No matter how management tries to spin the latest results, or the poor guidance going forward, one thing is clear. Robinhood’s growth story is over.

Without COVID-19 tailwinds, the key issues for this stock grow more obvious:

- growth has fallen to near zero and guidance implies negative year-over-year growth in 1Q22

- Robinhood’s main source of revenue is still highly volatile cryptocurrency and more risky (relative to standard equity trading) option trades.

- competitors continue to hold massive scale advantages and profitable businesses outside of a brokerage

- the lack of scale in an undifferentiated market begs the question – will Robinhood ever be consistently profitable?

The stock has fallen 63% from its IPO price and 83% from its 52-week high, yet still has significantly more downside.

Questionable Revenue Model Screeches to a Halt

Robinhood’s use of payment for order flow (PFOF) has been widely criticized, and we touched on the potential regulatory issues in our original report.

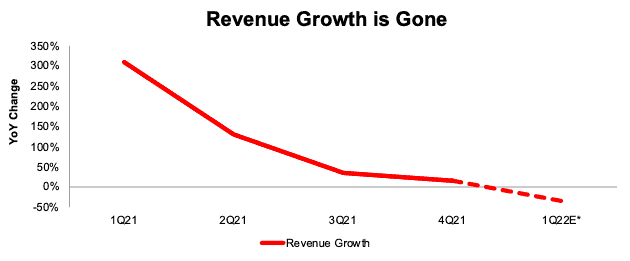

More importantly, what was once a growing model for revenue is no more. Per Figure 1, Robinhood’s revenue grew just 14% year-over-year (YoY) in 4Q21, down from 300%+ growth in 1Q21. Management’s guidance for 1Q22 implies a -35% YoY decline in revenue as retail investors/traders look elsewhere (competitors or non-investing activities alike).

Figure 1: Robinhood’s YoY Revenue Change: 1Q21 through 1Q22 Guidance

Sources: New Constructs, LLC and company filings.

*Based on management guidance for $340 million in revenue in 1Q22.

Investors No Longer Flock to Robinhood

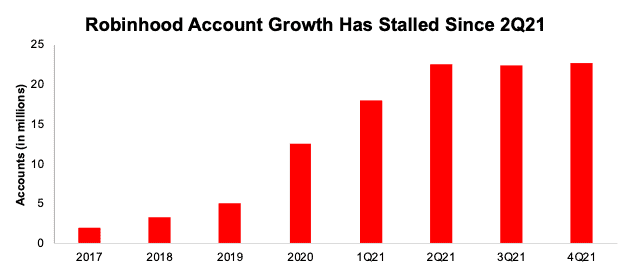

In our original report, we noted the impressive growth in customer accounts Robinhood achieved prior to its IPO, but argued its best days were likely behind it. Figure 2 shows how customer account growth stalled in the last three quarters of 2021.

Since rising to 22.5 million accounts in 2Q21, Robinhood’s account growth has stalled, and at the end of 4Q21, total cumulative funded accounts equaled just 22.7 million.

Figure 2: Robinhood’s Cumulative Funded Accounts – 2017 through 4Q21

Sources: New Constructs, LLC and company filings.

Brokerage Assets Stalled Alongside User Growth

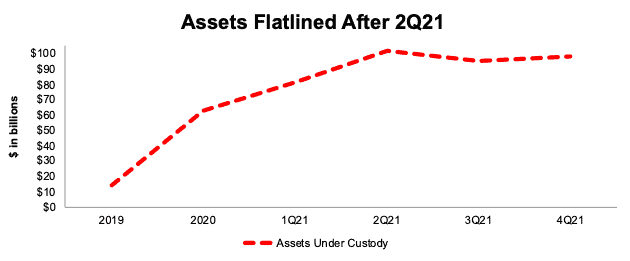

We believe that for Robinhood to compete with its much larger competition the company needs to drastically increase its brokerage assets, which Robinhood refers to as Assets Under Custody. Growing assets would provide a base source of net interest revenue if PFOF is banned, trading activity diminished, or both. However, per Figure 3, Robinhood’s Assets Under Custody, at $98 billion at the end of 4Q21, have fallen from the peak of $102 billion in 2Q21.

Figure 3: Robinhood’s Assets Under Custody – 2019 through 4Q21

Sources: New Constructs, LLC and company filings.

Lack of Scale is Still a Critical Business Model Flaw

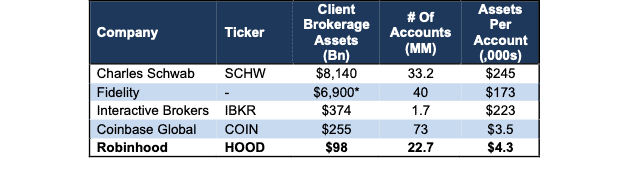

Robinhood’s lack of scale continues to be a big competitive disadvantage. The firm’s focus on first-time, low-profit investors originally helped the company sign up a high number of client accounts, but the average size of said accounts is much smaller than competitors. Per Figure 4, Robinhood holds less than 1% of the combined assets of larger peers and lacks the scale to generate enough revenue to compete with incumbents without PFOF.

Figure 4: Robinhood’s Client Assets Are Tiny Compared to Peers – 2021

Sources: New Constructs, LLC and company filings. Fidelity data available here.

*Estimate based on $11.1 trillion in customer assets at Fidelity minus $4.2 trillion in “Discretionary Assets” or assets in managed accounts that Fidelity has the discretion of how they’re invested.

Business Model Built On Conflict of Interest

With transaction based revenue, including PFOF, generating 77% of the company’s revenue in 2021, Robinhood has a clear incentive to generate and sell as much order flow as possible. The company has proven it is good – maybe too good – at enticing users to trade. More trading is not always prudent for clients and brokers generating account “churn” is not a new phenomenon for regulators. Notable regulatory issues:

- Robinhood previously agreed to pay a record $70 million settlement after a FINRA investigation into giving options trading to unqualified investors.

- This settlement comes after a lawsuit filed by the family of 20-year-old Alex Kearns, who committed suicide in June 2020 after Robinhood misinformed him about how much money he lost trading options.

- The state of Massachusetts filed a lawsuit against Robinhood to revoke its license to operate in the state based on claims of “gamifying” investing and predatory business practices.

The mounting regulatory risk Robinhood faces makes us concerned that the public may see Robinhood’s stated goal to ‘democratize investing’ as a ruse to lure them into gambling . That said, there are many beautiful casinos in Las Vegas that are tributes to the willingness of millions of people to lose money gambling.

Otherwise Undifferentiated Offering

In prior years, Robinhood stood out amongst its peers as the only brokerage offering commission-free trades. The largest brokerages quickly eliminated this competitive advantage by cutting stock commissions in late 2019.

Generally, there is a lack of differentiation between most brokerage businesses. Not only do they all offer 0% commission on stock trades, most offer ancillary services, such as education, a variety of asset classes to invest in, retirement accounts, personalized wealth management, and options trading. Robinhood is playing catch up in some instances, for example, the firm plans to begin offering retirement accounts later this year.

Robinhood’s most differentiating feature, options trading for new investors, has also been a source of significant legal and regulatory costs and challenges, and led famed investor Charlie Munger to call Robinhood “a gambling parlor masquerading as a respectable business.”

A Niche Player in Crypto

Robinhood continues its push into cryptocurrency and plans to add more coins to its trading capabilities in 2022. However, just like in traditional securities, Robinhood is playing catch up in this market as well. Peers such as Coinbase (COIN) dwarf its brokerage assets and others, such as PayPal (PYPL) and Block (SQ) are looking to take market share in the industry as well.

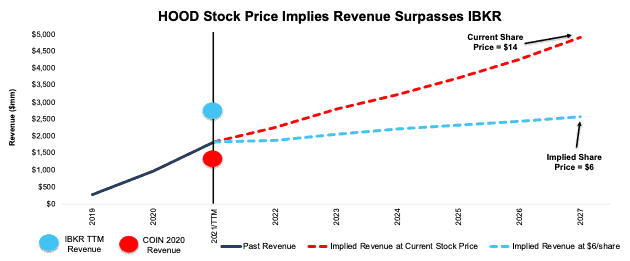

Valuation Implies 2x Revenue of Interactive Brokers

Below we use our reverse discounted cash flow (DCF) model to show the expectations for future cash flows in HOOD look overly optimistic, given that Robinhood’s growth story unraveled in the second half of 2021 and guidance for 1Q22 is weak.

To justify Robinhood’s current price of $14/share, the company must:

- improve its NOPAT margin to 16% (compared to 8% in 2020 and -355% in 3Q21) and

- grow revenue by 26% compounded annually through 2027, which is over 6x the projected industry growth rate through 2026

In this scenario, Robinhood would generate $4.9 billion in revenue in 2027, which is nearly 3x its 2021 revenue, 2x Interactive Brokers (IBKR) TTM revenue and 4x Coinbase’s TTM revenue. Additionally, Robinhood would generate $784 million in NOPAT in 2030, which is more than 9x its 2020 NOPAT and just under half Interactive Brokers’ TTM NOPAT.

Keep in mind, the number of companies that grow revenue by 20%+ compounded annually for such a long period are unbelievably rare, making the expectations in Robinhood’s share price look unrealistic.

57% Downside Even if Growth is 4x Industry Expectations

Robinhood’s economic book value, or no growth value, is negative $1/share, which illustrates the overly optimistic expectations in its stock price.

Even if we assume Robinhood:

- achieves a NOPAT margin of 16% and

- grows revenue by 15% compounded annually through 2027 (nearly 4x projected industry growth rates through 2026) then

the stock is worth just $6/share today – a 57% downside.

Figure 5 compares the company’s implied future revenue in these two scenarios to its historical revenue, along with the revenue of competitors, such as Interactive Brokers and Coinbase.

Figure 5: Robinhood’s Historical and Implied Revenue: DCF Valuation Scenarios

Sources: New Constructs, LLC and company filings

Each of the above scenarios also assumes Robinhood grows revenue, NOPAT, and FCF without increasing working capital or fixed assets. This assumption is highly unlikely but allows us to create best-case scenarios that demonstrate the level of expectations embedded in the current valuation. For reference, Robinhood’s invested capital increased $1.4 billion (146% of revenue) YoY in 2020. If we assume Robinhood’s invested capital increases at a similar rate in DCF scenario 2, the downside risk is even larger.

This article originally published on February 2, 2022

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.