The Small Cap Growth style ranks last out of the twelve fund styles as detailed in our 1Q21 Style Ratings for ETFs and Mutual Funds report. Last quarter, the Small Cap Growth style ranked last as well. It gets our Very Unattractive rating, which is based on an aggregation of ratings of 21 ETFs and 509 mutual funds in the Small Cap Growth style as of January 20, 2021. See a recap of our 4Q20 Style Ratings here.

Figures 1 and 2 show the five best and worst rated ETFs and mutual funds in the style. Not all Small Cap Growth style ETFs and mutual funds are created the same. The number of holdings varies widely (from 28 to 3,251). This variation creates drastically different investment implications and, therefore, ratings.

Investors should not buy any Small Cap Growth ETFs or mutual funds because none get an Attractive-or-better rating. If you must have exposure to this style, you should buy a basket of Attractive-or-better rated stocks and avoid paying undeserved fund fees. Active management has a long history of not paying off.

The best fundamental data in the world, proven in The Journal of Financial Economics, drives our research. Our Robo-Analyst technology[1] empowers our unique ETF and mutual fund rating methodology, which leverages our rigorous analysis of each fund’s holdings.[2] We think advisors and investors focused on prudent investment decisions should include analysis of fund holdings in their research process for ETFs and mutual funds.

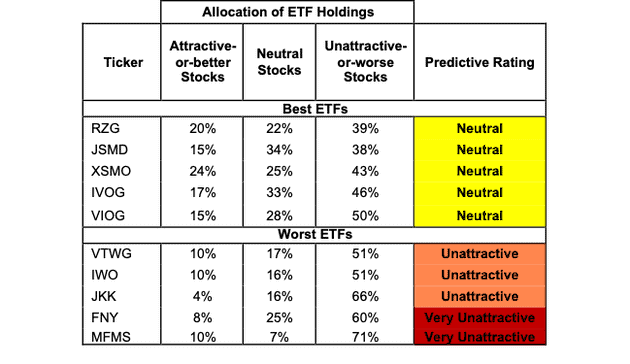

Figure 1: ETFs with the Best & Worst Ratings – Top 5

* Best ETFs exclude ETFs with TNAs less than $100 million for inadequate liquidity.

Sources: New Constructs, LLC and company filings

Fidelity Small-Mid Factor ETF (FSMD) and Janus Henderson Small Cap Growth Alpha ETF (JSML) are excluded from Figure 1 because their total net assets (TNA) are below $100 million and do not meet our liquidity minimums.

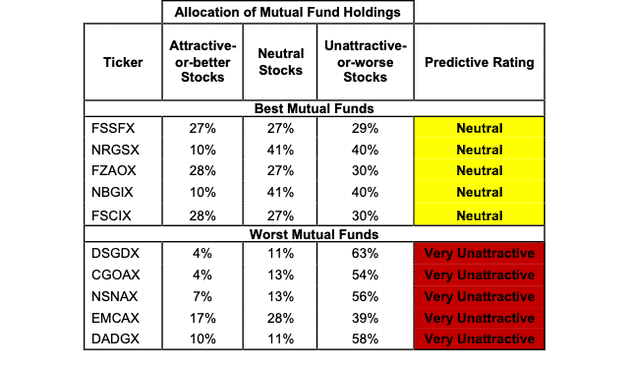

Figure 2: Mutual Funds with the Best & Worst Ratings – Top 5

* Best mutual funds exclude funds with TNAs less than $100 million for inadequate liquidity.

Sources: New Constructs, LLC and company filings

American Beacon Bahl & Gaynor Small Cap Growth Fund (GBSIX, GBSYX, GBSPX, GBSCX) is excluded from Figure 2 because its total net assets (TNA) are below $100 million and do not meet our liquidity minimums.

Invesco S&P Small Cap 600 Pure Growth ETF (RZG) is the top-rated Small Cap Growth ETF and Fidelity Advisor Series Small Cap Fund (FSSFX) is the top-rated Small Cap Growth mutual fund. Both earn a Neutral rating.

RBB MFAM Small Cap Growth ETF (MFMS) is the worst rated Small Cap Growth ETF and Dunham Small Cap Growth Fund (DADGX) is the worst rated Small Cap Growth mutual fund. Both earn a Very Unattractive rating.

The Danger Within

Buying a fund without analyzing its holdings is like buying a stock without analyzing its business and finances. Put another way, research on fund holdings is necessary due diligence because a fund’s performance is only as good as its holdings’ performance. Don’t just take our word for it, see what Barron’s says on this matter.

PERFORMANCE OF HOLDINGS = PERFORMANCE OF FUND

Analyzing each holding within funds is no small task. Our Robo-Analyst technology enables us to perform this diligence with scale and provide the research needed to fulfill the fiduciary duty of care. More of the biggest names in the financial industry (see At BlackRock, Machines Are Rising Over Managers to Pick Stocks) are now embracing technology to leverage machines in the investment research process. Technology may be the only solution to the dual mandate for research: cut costs and fulfill the fiduciary duty of care. Investors, clients, advisors and analysts deserve the latest in technology to get the diligence required to make prudent investment decisions.

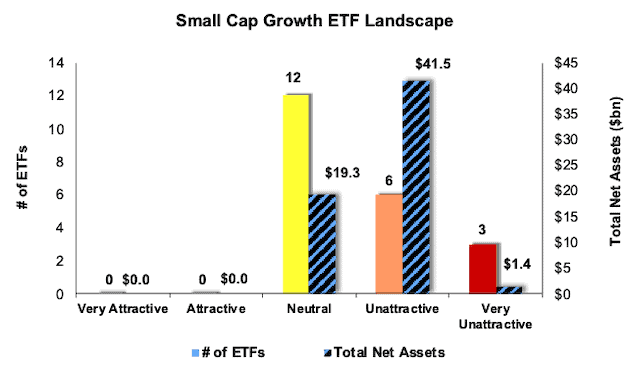

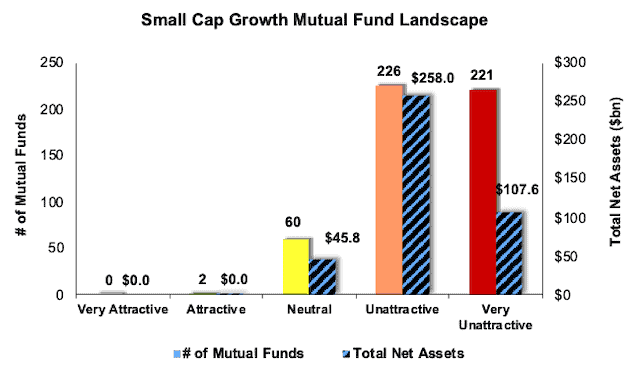

Figures 3 and 4 show the rating landscape of all Small Cap Growth ETFs and mutual funds.

Figure 3: Separating the Best ETFs from the Worst Funds

Sources: New Constructs, LLC and company filings

Figure 4: Separating the Best Mutual Funds from the Worst Funds

Sources: New Constructs, LLC and company filings

This article originally published on January 22, 2021.

Disclosure: David Trainer, Kyle Guske II, Alex Sword, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Harvard Business School features the powerful impact of our research automation technology in the case New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.

[2] See how our models and financial ratios are superior to Bloomberg and Capital IQ’s (SPGI) analytics in the detailed appendix of this paper.