Economic Earnings for the S&P 500 have been falling quarter-over-quarter (QoQ) since 1Q22. 4Q22 was no different. Trailing-twelve-months (TTM) Economic Earnings in 4Q22 were lower than 3Q22 TTM levels for all but three sectors: Financials, Energy, and Industrials.

This report is an abridged and free version of S&P 500 Economic Earnings: Downward Trend Continues In 4Q22, one of our quarterly series on fundamental market and sector trends. The full reports are available to our Professional and Institutional members or can be purchased below.

The full version of this report analyzes the economic earnings[1] (which adjust for unusual items on both the income statements and balance sheets) and GAAP earnings for the S&P 500 and its sectors (last quarter’s analysis is here).

Economic Earnings provide a more accurate measure of the true underlying cash flows of businesses than GAAP earnings. Reports on the drivers of Economic Earnings are here.

This report leverages our cutting-edge Robo-Analyst technology to deliver proven-superior[2] fundamental research and support more cost-effective fulfillment of the fiduciary duty of care.

Economic Earnings Fall in 4Q22

TTM Economic Earnings for the S&P 500 fell from $727.4 billion in 3Q22 to $673.8 billion in 4Q22, while TTM GAAP Earnings fell from $1.68 trillion to $1.55 trillion over the same time. Despite falling in the quarter, economic and GAAP earnings remain near record highs and well above pre-pandemic levels.

The S&P 500’s Economic Earnings have fallen quarter-over-quarter in each of the past four quarters, a trend we foresaw in our 1Q22 report S&P 500 Economic Earnings Set Records, but WACC Is a Drag. Indeed, a major headwind facing Economic Earnings is a rising weighted-average cost of capital (WACC). WACC for the S&P 500 sits at 6.8% in 4Q22, which is up from 6.3% in 3Q22 and 5.0% in 4Q21. Investors can protect themselves by paying closer attention to Economic Earnings, which account for the effects of high inflation on a firm’s WACC.

See Figure 1 in the full version of our report for the chart of Economic Earnings vs. GAAP earnings for the S&P 500 from December 2004 through 2022.

Key Details on Select S&P 500 Sectors

The Financials sector saw the largest QoQ improvement in TTM Economic Earnings, $24.8 billion, which rose from $11.6 billion in 3Q22 to $36.4 billion in 4Q22.

The Technology sector’s TTM Economic Earnings fell by 8% QoQ in 4Q22, though it generates the highest Economic Earnings of any sector. On the flip side, the Utilities sector has the lowest TTM Economic Earnings of any sector and was one of eight sectors that destroyed shareholder value in 4Q22.

Below, we highlight the Industrials sector, one of just three sectors which saw a QoQ improvement in TTM Economic Earnings in 4Q22.

Sample Sector Analysis[3]: Industrials

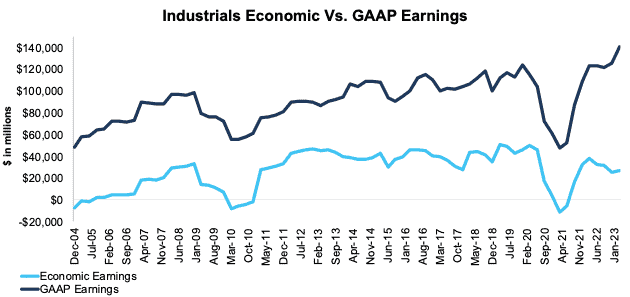

Figure 1 shows TTM Economic Earnings for the Industrials sector, at $26.4 billion, rose 7% QoQ in 3Q22, while TTM GAAP earnings, at $140.5 billion, rose 12% over the same time.

Figure 1: Industrials Economic Earnings Vs. GAAP: 2004 – 4Q22

Sources: New Constructs, LLC and company filings.

Our Economic Earnings analysis is based on aggregated TTM data for the sector constituents in each measurement period.

The March 8, 2023 measurement period incorporates the financial data from calendar 2022 10-K, as this is the earliest date for which all the calendar 2022 10-Ks for the S&P 500 constituents were available.

This article was originally published on March 30, 2023.

Disclosure: David Trainer, Kyle Guske II, and Italo Mendonça receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

Appendix: Calculation Methodology

We derive the economic earnings and GAAP Earnings metrics above by summing the Trailing Twelve Month individual S&P 500 constituent values for economic earnings and GAAP Earnings in each sector for each measurement period. We call this approach the “Aggregate” methodology.

The Aggregate methodology provides a straightforward look at the entire sector, regardless of market cap or index weighting and matches how S&P Global (SPGI) calculates metrics for the S&P 500.

[1] This report is based on the latest audited financial data available, which is the 2022 10-K in most cases. Price data as of 3/8/23.

[2] Our research utilizes our more of reliable fundamental data, as proven in Core Earnings: New Data & Evidence, written by professors at Harvard Business School (HBS) & MIT Sloan and published in The Journal of Financial Economics.

[3] The full version of this report provides analysis for every sector like what we show for this sector.