This report red flags the firms with the most underfunded pensions and the most aggressive assumptions for returns they expect to earn on the pension assets.

CEO David Trainer sat down with Chuck Jaffe of Money Life to talk about our Danger Zone pick this past week: Pension Accounting: Expected Returns on Plan Assets.

Pension underfunding remains dangerously high for many firms, and some companies use unusual assumptions for expected return on plan assets to mislead investors.

Some stocks are more dangerous than others. In an anemic economic environment, the most dangerous stocks are those with issues that are lurking behind the scenes or in footnotes.

Goodyear Tire & Rubber (GT) must overcome $3.7 billion in underfunded pensions plus $6.3 billion in debt ($1.1 billion of which is off balance sheet) before investors could see any upside.

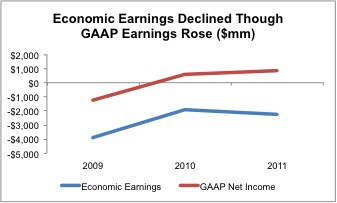

I do not think S&P's analysts are aware of Delta's staggering $22.3 billion in off-balance sheet liabilities, which include $14.1 billion in underfunded pensions and $8.2 in operating leases.

I recommend investors avoid Delta Airlines (DAL). I think the stock could see significant downward pressure as more investors realize how the company is propping up its earnings with relatively aggressive accounting for its pension and postretirement plan (“pensions”), which are already seriously underfunded.