The large drop in the 4Q22 trailing-twelve-months (TTM) GAAP earnings compared to relatively flat Core Earnings for the NC 2000[1] highlights the more stable nature of Core Earnings. Because we remove unusual losses and gains, Core Earnings are not vulnerable to the kitchen-sink effect that torpedoes 4Q22 TTM GAAP earnings. For the first time since 3Q20, NC 2000 TTM Core Earnings fell quarter-over-quarter (QoQ), albeit just 1%. There is churn among sectors, however, as Core Earnings for four of the eleven sectors through the TTM ended 4Q22 were higher than 3Q22 TTM levels.

This report is an abridged and free version of All Cap Index & Sectors: GAAP Earnings Continue Fall in 4Q22, one of our quarterly reports on fundamental market and sector trends. The full version of the report analyzes Core Earnings[2][3] and GAAP earnings of the NC 2000 and each of its sectors (last quarter’s analysis is here). The full reports are available to Professional and Institutional members.

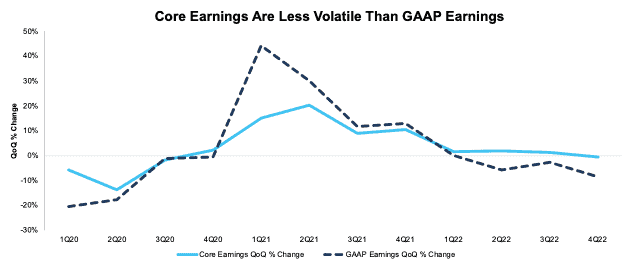

Core Earnings Are Less Volatile than GAAP Earnings

Figure 1 in the full report shows GAAP Earnings for the NC 2000 are lower than Core Earnings for the third consecutive quarter. Corporate profits, as measured by Core Earnings, have been much less volatile than GAAP earnings suggest, especially since 1Q20. For example, per Figure 2, in the TTM ended:

- 1Q21, GAAP earnings rose 44% QoQ compared to a 15% rise in Core Earnings.

- 2Q22, GAAP earnings fell 6% QoQ compared to a 2% rise in Core Earnings.

- 3Q22, GAAP earnings fell 3% QoQ compared to a 1% rise in Core Earnings.

- 4Q22, GAAP earnings fell 9% QoQ compared to a 1% decline in Core Earnings.

Figure 1: NC 2000 Core Earnings Vs. GAAP Earnings QoQ Percent Change: 1Q20 – 4Q22

Sources: New Constructs, LLC and company filings.

Our Core Earnings analysis is based on aggregated TTM data for the sector constituents in each measurement period.

The March 8, 2023 measurement period incorporates the financial data from calendar 2022 10-Ks, as this is the earliest date for which all of the calendar 2022 10-Ks for the NC 2000 constituents were available.

This report leverages our cutting-edge Robo-Analyst technology to deliver proven-superior[4] fundamental research and support more cost-effective fulfillment of the fiduciary duty of care.

GAAP Earnings Are Lower Than Core Earnings for Over Two-Thirds of the NC 2000[5] (by Market Cap)

For the TTM ended 4Q22, 64% of the companies in the NC 2000 reported GAAP Earnings that are lower than Core Earnings. The 1,283 companies with understated GAAP earnings make up 69% of the market cap of the NC 2000 as of 3/8/23.

When GAAP Earnings are lower than Core Earnings, they are understated by an average of 64%, per Figure 2. GAAP Earnings are understated by more than 10 percent for 35% of companies. For comparison, in the TTM ended 3Q22, 1,239 companies had understated GAAP earnings.

Figure 2: NC 2000 GAAP Earnings Understated by 64% On Average

Sources: New Constructs, LLC and company filings.

We use Funds from Operations (FFO) for Real Estate companies rather than GAAP Earnings.

Key Details on Select NC 2000 Sectors

The Energy sector saw the largest QoQ improvement in Core Earnings, which rose from $260.4 billion in 3Q22 to $283.4 billion in 4Q22, or 9%.

At $456.1 billion, the Technology sector generates the highest Core Earnings, and saw Core Earnings fall 2% QoQ in 4Q22. On the flip side, the Real Estate sector has the lowest Core Earnings at $33.2 billion, and the Telecom Services sector had the largest QoQ decline in 4Q22 at -12%.

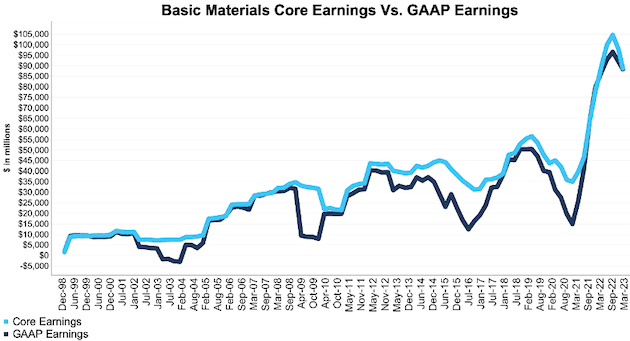

Below we highlight the Basic Materials sector and a stock with some of the most negative Earnings Distortion (i.e. understated GAAP earnings) in the sector.

Sample Sector Analysis[6]: Basic Materials

Figure 3 shows Core Earnings for the Basic Materials sector, at $88.8 billion, fell 9% QoQ in 4Q22, while GAAP earnings, at $88.4 billion, fell 4% over the same time.

Figure 3: Basic Materials Core Earnings Vs. GAAP: 1998 – 4Q22

Sources: New Constructs, LLC and company filings.

Our Core Earnings analysis is based on aggregated TTM data for the sector constituents in each measurement period.

The March 8, 2023 measurement period incorporates the financial data from calendar 2022 10-Ks, as this is the earliest date for which all of the calendar 2022 10-Ks for the NC 2000 constituents were available..

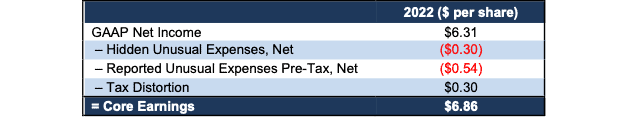

GAAP Earnings Understatement Details: Dow Inc. (DOW)

Below, we detail the hidden and reported unusual items that were overlooked in GAAP Earnings captured in Core Earnings for Dow Inc. After adjusting for unusual items, we find that Dow’s Core Earnings of $5.0 billion, or $6.86/share are much higher than reported GAAP Earnings of $4.6 billion, or $6.31/share.

Dow’s Earnings Distortion Score is Beat and its Stock Rating is Attractive, in part due to its positive economic earnings and price-to-economic book value (PEBV) ratio of 0.8. We made Dow a Long Idea in September 2022. The stock is up 16% while the S&P is up 4% since then. The stock remains undervalued.

Below, we detail the differences between Core Earnings and GAAP Earnings so readers can audit our research.

Figure 4: Dow’s GAAP Earnings to Core Earnings Reconciliation

Sources: New Constructs, LLC and company filings.

More details:

Total Earnings Distortion of -$0.54/share, which equals -$394 million, is comprised of the following:

Hidden Unusual Expenses Pre-Tax, Net = -$0.30/per share, which equals -$220 million and is comprised of:

- -$230 million in digitalization program costs bundled in Corporate costs

- $10 million in sublease income

Reported Unusual Expenses Pre-Tax, Net = -$0.54/per share, which equals $390 million and is comprised of:

- -$662 million in interest expense and amortization of debt discount

- -$337 million contra adjustment for recurring pension costs. These recurring expenses are reported in non-recurring line items, so we add them back and exclude them from Earnings Distortion.

- -$118 million restructuring and asset related charges

- -$117 million in foreign exchanges losses

- -$8 million loss on early extinguishment of debt

- -$4 million in indemnification and other transaction-related costs

- $31 million in Other Income

- $60 million in Dow Silicones breast implant liability adjustment

- $78 million gain on sales of other assets and investments

- $321 million gain related to Nova legal matter

- $358 million in non-operating pension and other post-retirement benefit plan net credits

Tax Distortion = $0.30/per share, which equals $216 million

This article was originally published on March 31, 2023.

Disclosure: David Trainer, Kyle Guske II, and Italo Mendonça receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

Appendix: Calculation Methodology

We derive the Core Earnings and GAAP Earnings metrics above by summing up the trailing-twelve-month individual NC 2000 constituent values for Core Earnings and GAAP Earnings in each sector for each measurement period. We call this approach the “Aggregate” methodology.

The Aggregate methodology provides a straightforward look at the entire sector, regardless of market cap or index weighting and matches how S&P Global (SPGI) calculates metrics for the S&P 500.

[1] The NC 2000 consists of the largest 2000 U.S. companies by market cap in our coverage. Constituents are updated on a quarterly basis (March 31, June 30, September 30, and December 31). We exclude companies that report under IFRS and ADR companies.

[2] Core Earnings enable investors to overcome the flaws in legacy fundamental data and research, as proven in Core Earnings: New Data & Evidence, written by professors at Harvard Business School (HBS) & MIT Sloan for The Journal of Financial Economics.

[3] Based on the latest audited financial data, which is the 2022 10-K in most cases. Price data as of 3/8/23.

[4] Our research utilizes our Core Earnings, a more reliable measure of profits, as proven in Core Earnings: New Data & Evidence, written by professors at Harvard Business School (HBS) & MIT Sloan and published in The Journal of Financial Economics.

[5] Understated companies include all companies with Earnings Distortion <-0.1% of GAAP earnings.

[6] The full version of this report provides analyses for all eleven sectors.