Arm Holdings (ARM: $47 to $51/share), the chip design giant, is expected to start trading September 14, 2023 at a ~$49 billion valuation. At $49/share, the midpoint of its IPO price range, Arm Holdings earns our Unattractive Stock Rating and is this week’s Danger Zone pick. We think it is fair to say that the ~$49 billion valuation mark is based more on Softbank’s self-dealing in private markets to manipulate the valuation higher than the fundamentals of the company.

Specifically, at the midpoint of its IPO price range, the stock’s valuation implies the company will 10x profits and achieve revenue growth well above industry expectations. ARM looks more than fully valued and does not provide investors any upside potential, as we’ll illustrate with our reverse discounted cash flow (DCF) model.

Our IPO research aims to provide more investors with more reliable fundamental research.

Softbank’s Self-Dealing Valuation

In what has now become a well-worn strategy, Softbank famously (and artificially) increased WeWork’s (WE) “on-paper” valuation prior to its attempted IPO. First, in August 2017, SoftBank and its Vision Fund invested in WeWork at a ~$20 billion valuation. In June 2018, SoftBank invested further capital, but this time at a $35-$40 billion valuation. Lastly, in January 2019, just six months before WeWork filed its S-1, SoftBank invested in WeWork again at a $47 billion valuation. We think that self-dealing was a big part of the basis for attempting to IPO WeWork at a $40+ billion valuation. We know how that story ended.

We think the same ploy could be happening with Arm. Softbank took Arm private at a $32 billion valuation in 2016 and, in 2017, sold a 25% stake to the Vision Fund, a fund managed by SoftBank. Fast forward to August 2023, just weeks before Arm would file its F-1, SoftBank bought back Vision Fund’s stake in Arm, but this time at a $64 billion valuation. In other words, SoftBank doubled the “on-paper” valuation of Arm by buying shares from itself, just as it did before the WeWork IPO. That’s not a great precedent.

While Arm’s midpoint IPO valuation of $49 billion may seem cheap relative to the recent $64 billion mark, that mark is a result of self-dealing, not an efficient market.

Other Big Red Flags for Investors From the Footnotes

Self-dealing is not the only reason we caution investors against buying into this IPO. Softbank is making this deal bad for public investors for other reasons.

Public Shareholders Will Have No Rights

Upon completion of the IPO, Softbank Group is expected to own between 90-91% (varies based on underwriter’s decision to exercise option to purchase more) of Arm’s outstanding shares. As a result, Arm will be considered a “controlled company”. As a controlled company, new investors will have no say in determining the outcome of matters submitted for shareholder approval.

Additionally, Arm notes in its F-1:

“As a controlled company, we have elected not to comply with certain corporate governance requirements applicable to most Nasdaq-listed companies. Accordingly, you will not have the same protections afforded to shareholders of companies that are subject to all of these corporate governance requirements.”

In other words, this IPO will take investors’ money while giving them no voting power or control of corporate governance.

Status as Foreign Private Issuer Minimizes Transparency

Investors should take note and beware of Arm’s intentional exploitation of its status as a Foreign Private Issuer.

Under the rules of the SEC, Arm Holdings qualifies as a foreign private issuer, which exempts the company from compliance with certain laws and rules of the SEC and NASDAQ. For instance:

- Arm is exempt from certain rules under the Exchange Act that regulate obligations related to the solicitations of proxies.

- Arm executive officers and directors are exempt from the reporting and “short-swing” profit recovery provisions in the Exchange Act with respect to purchases and sale of securities.

- Arm is not required to file period reports and financial statements with the SEC as frequently or as promptly as U.S. public companies.

- Arm is not required to file its annual report until four months after the end of its fiscal year, while U.S. domestic issuers are required to file their annual report with 75 days of the end of their fiscal year.

Arm notes in its F-1 that is has “taken advantage of certain of these reduced reporting and other requirements in its prospectus.” In other words, the information in the F-1 may be less and/or different than that required from U.S. issuers.

Our spidey sense goes off anytime anyone chooses to be less transparent than usual. Especially in business, we think it’s a bad omen whenever companies choose to be less transparent. If things are great, what is there to hide? The bottom line is that great companies tend not to have anything to hide. That is part of why they are great. Arm does not appear to be great.

China Risk

Arm China represents 24% of Arm’s overall revenue in fiscal 2023. The problem here is that neither Arm nor Softbank control the operations of Arm China. Should geopolitical tensions rise further between the United States and China, or China itself clamps down trade for national security reasons, Arm Holdings’ revenue could be severely impacted from its dependence on Arm China.

For example, recent news that China might ban government use of iPhones suggests tensions are, indeed, rising. We’ve seen the Chinese government take rather drastic measures against large companies, like Alibaba (BABA) and Tencent (TCEHY). Even if the Chinese government only threatens to take away part of Arm, we think that could send shares much lower. Considering the escalating strategic importance of semiconductors and the attendant technology, it is not outside of the realm of possibility that Arm Holdings could lose Arm China.

For reference, Arm Holdings’ economic book value, or no growth value, is only $13/share. Losing 24% of its revenue would put a big dent in the growth story and could easily send the stock below its economic book value.

A Profitable Company Is Not Always A Good Stock

Arm Holdings has been profitable over the past two years, the only years for which it discloses financial data. Given that the company provides key components for nearly every smartphone on the market, it will likely be profitable for many years to come.

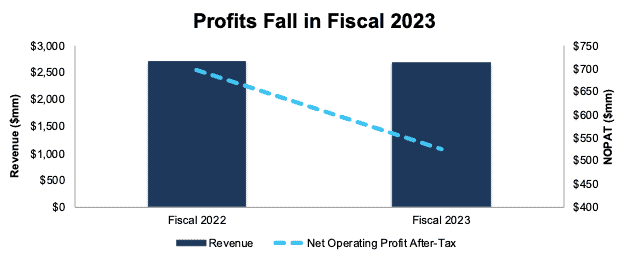

Through the collection of royalties on nearly all smartphones in the world, Arm Holdings generated nearly $2.7 billion in revenue in fiscal 2023 (year end March 2023) and $525 million in net operating profit after tax (NOPAT). In fiscal 2023, revenue was down 1% year-over-year while NOPAT was down 24% over the same time. See Figure 1.

Figure 1: Arm Holdings’ Revenue & NOPAT: Fiscal 2022 – Fiscal 2023

Sources: New Constructs, LLC and company filings

Market Share Leader…

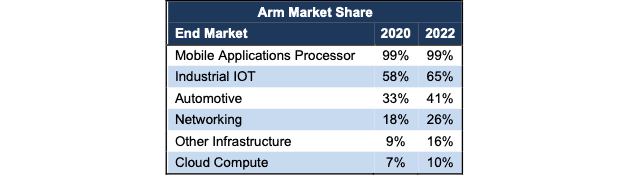

In its F-1, Arm refers to its chip design intellectual property (“IP”) as “the world’s most pervasive CPU architecture”, and its market share in its many end markets backs up this claim. Beyond the staggering 99% market share of the mobile applications processor market, a market share Arm has held “for many years”, the company has successfully grown its share in many other markets as well. See Figure 2. Further highlighting its prevalence, the company estimates that 70% of the world population uses Arm based products.

Figure 2: Arm Market Share by End Market: 2020 – 2022

Sources: New Constructs, LLC and company filings

…In Growing Markets

Not does only Arm hold significant, and rising, market share in its end markets, these markets are also poised for strong growth in the coming years. Per the company’s F-1, there were 30.6 billion chips shipped in the year ended March 2023, which is 70% more than the number of chips shipped in the year ended March 2016.

The company’s end markets are projected to grow at the following compound annual rates through 2025:

- All chips that contain a processor: 6.8%

- Mobile application processors: 6.4%

- Consumer electronics: 4.3%

- Industrial IOT: 6.7%

- Networking equipment: 1.8%

- Cloud Compute: 16.6%

- Other Infrastructure: 2.7%

- Automotive: 15.7%

Customer List Runs the Gamut

As the leading CPU architecture for many of the electronic devices we use on the daily, it should come as no surprise that Arm works with some of the largest firms in the world, including:

- Apple (AAPL)

- Advanced Micro Devices (AMD)

- Alphabet (GOOGL)

- Intel (INTC)

- NVIDIA (NVDA)

- Samsung

- Qualcomm (QCOM)

- Amazon (AMZN)

In total, Arm estimates that more than 60 companies reported they shipped Arm-based chips in the year ended March 2023.

But Customers Are Concentrated

While Arm may boast a large customer base, some are clearly more important than others.

For the year ended March 2023, 57% of Arm’s revenue came from its top five customers. Its largest customer, Arm China, accounted for 24% of revenue in fiscal 2023, which is an increase from 18% of revenue in fiscal 2022.

As we all know from studying Michael Porter, large customers can exert more influence over their suppliers. In other words, large customers have a lot of bargaining power when it comes to pricing. We think there’s risk that these customers decide to negotiate for lower prices, take their business elsewhere or build more of their own chips. In any of those scenarios, Arm’s profit growth could take a big dive.

Customers are Also Competitors

Because Arm-based chips are only one piece of the puzzle to building electronic devices, its customers can often end up as competitors. While a customer may use a single central processing unit (CPU) design from Arm, it may choose to develop the other components on its own. No one knows what a company needs more than its own internal design team. Building customized solutions, while more costly up front, can create lasting efficiencies and cost savings and eliminate additional licensing opportunities for Arm Holdings.

Arm also faces competition from other chip technologies such as the x86 architecture, which is owned by Intel, AMD, and RISC-V. These technologies have a much stronger foothold than Arm in the markets for laptops and data centers. As a result, we do not expect Arm to see much growth in those markets.

Lastly, Arm’s customers do not license Arm products exclusively. Instead, Arm’s customers also develop, manufacture and market processors based on non-Arm architectures. These customers turned competitors are in the business of designing their own architectures in markets where Arm aims to compete.

The bottom line here is that Arm faces a growing brigade of formidable competitors in each of its end markets. Many of the competitors have more than enough capital and expertise to build their own custom solutions and box Arm out of many of the markets in which it needs to grow to justify its lofty IPO valuation.

RISC-V Architecture Poses Problems

In particular, RISC-V is an open-source architecture that could eat into Arm’s large market share in the coming years. The adoption and use of RISC-V as a substitute to Arm architecture provides key benefits to potential customers:

- Is open-source, which enables customers to avoid Arm licensing fees

- Eliminates dependency on Arm and thereby limits Arms pricing power

Perhaps most importantly, RISC-V has support from some of the largest tech companies in the world, who also happen to be Arm customers.

In August 2023, Qualcomm (QCOM), along with Bosch, Infineon, Nordic Semiconductor, and NXP Semiconductors announced a joint venture aimed at “accelerating the commercialization of future profits based on the open-source RISC-V architecture.” The joint venture’s initial focus will be automotive, but it will eventually expand into mobile and IoT.

Before the joint venture, Google presented at the RISC-V Summit to show its support for RISC-V. Lars Bergstrom, Android’s director of engineering noted that he wants RISC-V to be seen as a ”tier 1 platform” in Android, akin to Arm. Should current customers continue to strongly support RISC-V, Arm’s days of market dominance could soon be a relic of the past. However, at the midpoint of its IPO valuation, Arm is priced for the exact opposite – significant revenue and profit growth, as we’ll show below.

Less Profitable than Peers and Customers

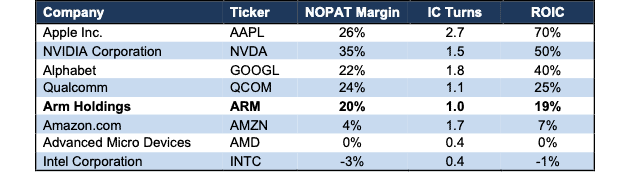

Unfortunately for investors, being the provider of key components for all smartphones and other device has not built a profit juggernaut. In fact, Arm Holdings’ NOPAT margin and return on invested capital (ROIC), while still high at 20% and 19% respectively, fall below peers/competitors such as Apple, NVIDIA, Alphabet, and Qualcomm. See Figure 3.

Most of these firms are also more efficient from a balance sheet perspective and achieve higher invested capital turns than Arm’s 1.0 in fiscal 2023.

For an IPO valuation as lofty as Arm’s, you’d think the company would be more competitive and have a higher ROIC. Note that the lower ROIC only accentuates the vulnerability of Arm to competition from its peers and customers because the higher ROIC gives them more capital to bring to the fight for market share and the development of superior technology.

Figure 3: Arm Holdings’ Profitability Vs. Competition: TTM

Sources: New Constructs, LLC and company filings

Valuation Implies Too Much Profit Growth

When we use our reverse discounted cash flow (DCF) model to analyze the future cash flow expectations baked into ARM, we find that shares, even at the midpoint, embed very optimistic assumptions about margins and growth. We think the stock looks fully valued.

To justify the midpoint of its IPO valuation, our model shows Arm would have to:

- immediately improve NOPAT margin to 26% (equal to fiscal 2022 and also equal to Apple’s TTM NOPAT margin) and

- grow revenue by 22% compounded annually (over 3x Arm’s own estimated growth of its total addressable market through 2025) for the next decade.

In this scenario, Arm would earn $20 billion in revenue in fiscal 2033, or 7.5x its fiscal 2023 revenue, and $5.2 billion in NOPAT, or nearly 10x its fiscal 2023 NOPAT. For reference, Advanced Micro Devices generated $22 billion in revenue over the trailing-twelve-months, but it generated negative NOPAT.

We can further analyze the implications of this scenario by looking at the revenue Arm generates per chip shipped and the chip shipments implied by the scenario above. In fiscal 2023, Arm generated $2.7 billion in revenue while 30.6 billion Arm-based chips were shipped, which means Arm collects ~9 cents per chip shipped. If we assume this rate remains the same, Arm customers must ship 228 billion Arm-based chips in fiscal 2033 for Arm to generate the revenue implied by the midpoint IPO valuation. For reference, Arm notes in its F-1 that there have been only 250 billion Arm-based chips shipped in the last 30 years or since its inception in 1990.

It’s also important to note that companies that grow revenue by 20%+ compounded annually for such a long period are “unbelievably rare”. The cash flows expectations in Arm Holdings’ midpoint IPO valuation are very high, which indicates there could be much more downside risk than upside potential.

41% Downside if Growth is 2x Industry

We present an additional DCF scenario to highlight the downside potential in the stock should Arm grow sales at 2x industry projections.

If we assume Arm’s:

- NOPAT margin immediately improves to 26% and

- revenue grows 14% compounded annually (2x Arm’s estimate growth of its TAM through 2025) for the next decade, then

ARM would be worth just $29/share today – a 41% downside to the midpoint IPO price range. In this scenario, Arm’s revenue would still grow to $9.6 billion in fiscal 2033, or 3.6x Arm’s fiscal 2023 revenue. This scenario also implies the company would earn $2.5 billion in NOPAT and grow NOPAT 17% compounded annually through fiscal 2033.

If we assume Arm generates ~9 cents in revenue per chip, this scenario implies Arm customers ship 109.6 billion Arm-based chips in fiscal 2033, or 3.6x chips shipped in fiscal 2023.

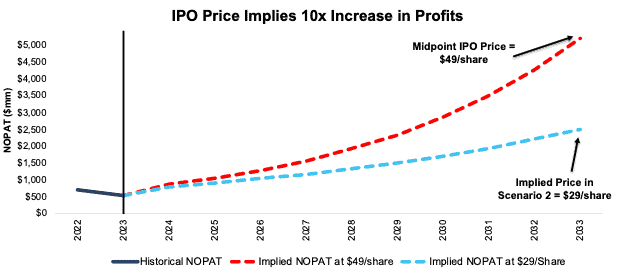

Figure 4 compares Arm Holdings’ implied future NOPAT in these scenarios to its historical NOPAT.

Figure 4: Midpoint IPO Price Looks Fully Valued

Sources: New Constructs, LLC and company filings

Each of the above scenarios assume Arm Holdings grows revenue, NOPAT, and FCF without increasing working capital or fixed assets. This assumption is highly unlikely but allows us to create best-case scenarios that demonstrate the high level of expectations embedded in the current valuation.

No White Knight To Save Softbank

The expectations baked into Arm’s IPO valuation look highly optimistic. Often, the best hope investors might have in overvalued stocks is for an established company to acquire the firm. However, that hope has already been dashed, which led to the current attempted IPO. In 2020, NVIDIA announced its plan to acquire Arm for $40 billion. However, after a years-long fight with regulatory bodies, the two announced a termination of the deal in February 2022.

The termination announcement stated, “Arm will now start preparations for a public offering.” In other words, there was no white knight to bail out Softbank from its pricey purchase of Arm, and now it’s looking to offload its overvalued shares to unsuspecting public investors. We think investors would be wise to avoid the bait.

This article was originally published on September 8, 2023.

Disclosure: David Trainer, Kyle Guske II, Italo Mendonça, and Hakan Salt receive no compensation to write about any specific stock, style, or theme.

Questions on this report or others? Join our Society of Intelligent Investors and connect with us directly.