The Large Cap Value style ranks third out of the twelve fund styles as detailed in our 4Q16 Style Ratings for ETFs and Mutual Funds report. Last quarter, the Large Cap Value style ranked second. It gets our Neutral rating, which is based on an aggregation of ratings of 47 ETFs and 844 mutual funds in the Large Cap Value style as of November 4, 2016. See a recap of our 3Q16 Style Ratings here.

Figures 1 and 2 show the five best and worst rated ETFs and mutual funds in the style. Not all Large Cap Value style ETFs and mutual funds are created the same. The number of holdings varies widely (from 19 to 900). This variation creates drastically different investment implications and, therefore, ratings.

Investors seeking exposure to the Large Cap Value style should buy one of the Attractive-or-better rated ETFs or mutual funds from Figures 1 and 2.

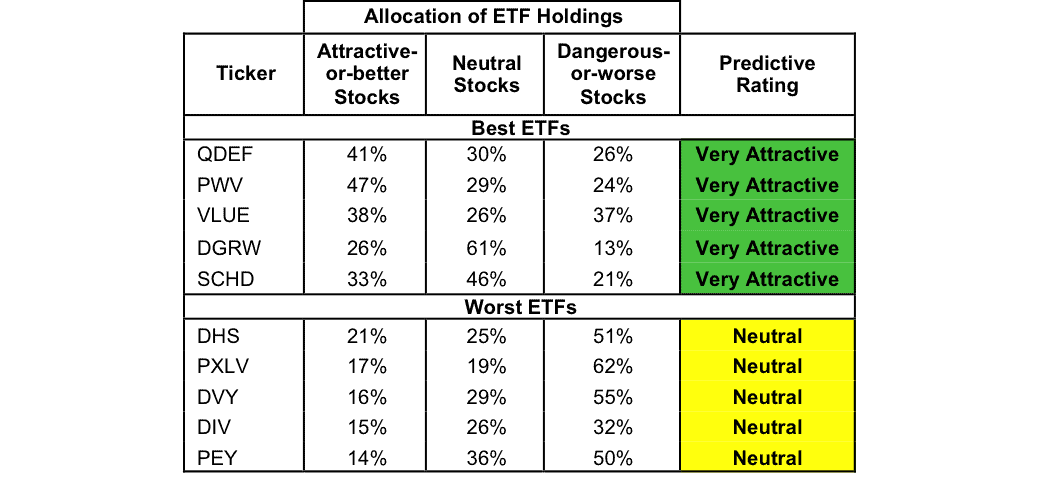

Figure 1: ETFs with the Best & Worst Ratings – Top 5

* Best ETFs exclude ETFs with TNAs less than $100 million for inadequate liquidity.

Sources: New Constructs, LLC and company filings

Four ETFs are excluded from Figure 1 because their total net assets (TNA) are below $100 million and do not meet our liquidity minimums. To see these ETFs please view our fund screener page.

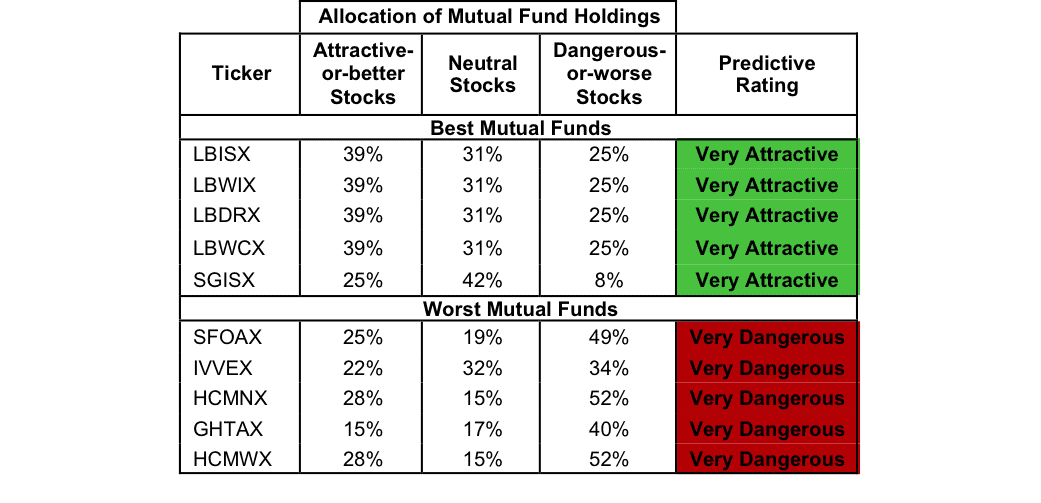

Figure 2: Mutual Funds with the Best & Worst Ratings – Top 5

* Best mutual funds exclude funds with TNAs less than $100 million for inadequate liquidity.

Sources: New Constructs, LLC and company filings

Legg Mason BW Dynamic Large Cap Value Fund (LMBGX, LMBEX, LMBHX, LMBBX) is excluded from Figure 2 because its total net assets (TNA) are below $100 million and do not meet our liquidity minimums.

FlexShares Quality Dividend Defensive Fund (QDEF) is the top-rated Large Cap Value ETF and Legg Mason Diversified Large Cap Value Fund (LBISX) is the top-rated Large Cap Value mutual fund. Both earn a Very Attractive rating.

PowerShares High Yield Equity Dividend Achievers Portfolio (PEY) is the worst rated Large Cap Value ETF and HCM Dividend Sector Plus Fund (HCMWX) is the worst rated Large Cap Value mutual fund. DVY earns a Neutral rating and HCMWX earns a Very Dangerous rating.

Cisco Systems (CSCO: $31/share) is one of our favorite stocks held by BIGRX and earns a Very Attractive rating. Cisco was first featured as a Long Idea in August 2012 and remains a quality value investment. Over the past decade, CSCO has grown after-tax profit (NOPAT) by 7% compounded annually. CSCO has improved its return on invested capital (ROIC) from 15% in 2006 to a top-quintile 18% in 2016. Despite the impressive profit growth, shares remain undervalued. At its current price of $31/share, CSCO has a price-to-economic book value (PEBV) ratio of 0.8. This ratio means the market expects Cisco’s NOPAT to permanently decline by 20%. If Cisco can grow NOPAT by just 4% compounded annually over the next decade, the stock is worth $44/share today – a 42% upside.

FelCor Lodging Trust (FCH: $7/share) is one of our least favorite companies held by GHTAX and earns a Very Dangerous rating. Since 2006, FCH’s NOPAT has declined by 6% compounded annually. The company’s ROIC has fallen from 7% in 2006 to a bottom-quintile 4% over the last twelve months (TTM). Despite the deterioration of the business’ fundamentals, FCH remains overvalued. To justify its current stock price of $7/share, FCH would have to grow NOPAT by 14% compounded annually for the next 11 years. This scenario seems overly optimistic given the decline of FelCor’s NOPAT since 2006.

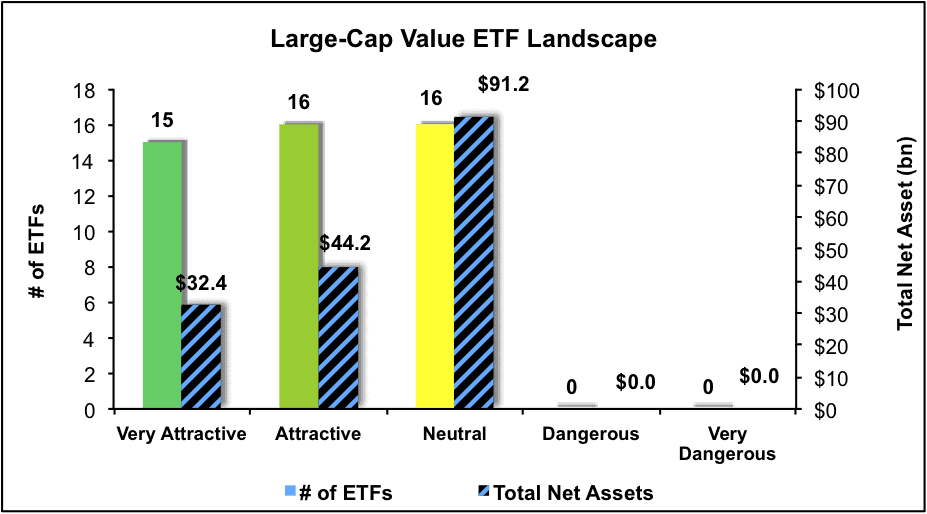

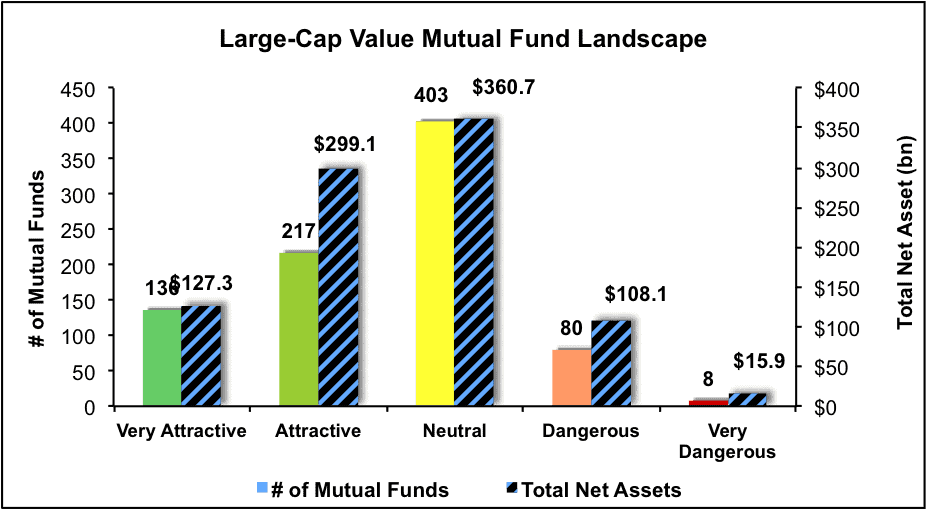

Figures 3 and 4 show the rating landscape of all Large Cap Value ETFs and mutual funds.

Figure 3: Separating the Best ETFs From the Worst Funds

Sources: New Constructs, LLC and company filings

Figure 4: Separating the Best Mutual Funds From the Worst Funds

Sources: New Constructs, LLC and company filings

This article originally published here on November 4, 2016.

Disclosure: David Trainer, Kyle Guske and Kyle Martone receive no compensation to write about any specific stock, style, or theme.