Three new stocks make our Safest Dividend Yields Model Portfolio this month, which was made available to members on June 22, 2017.

Recap from May’s Picks

Our Safest Dividend Yields Model Portfolio underperformed the S&P 500 last month. The Model Portfolio fell 0.7% on a price return basis and rose 0.3% on a total return basis. The S&P 500 rose 0.5% on a price return basis and 1.0% on a total return basis. The best performing stocks in the portfolio were large cap stock Las Vegas Sands (LVS), which was up 12%, and small cap stock, Waddell & Reed (WDR), which was up 14%. Overall, nine out of the 20 Safest Dividend Yield stocks outperformed the S&P in May.

Since inception, this Model Portfolio is up 9% on a price return basis (S&P +12%) and 13% on a total return basis (S&P +14%).

The success of this Model Portfolio highlights the value of our Robo-Analyst technology, which scales our forensic accounting expertise (featured in Barron’s) across thousands of stocks.

This Model Portfolio only includes stocks that earn an Attractive or Very Attractive rating, have positive free cash flow and economic earnings, and offer a dividend yield greater than 3%. Companies with strong free cash flow provide higher quality and safer dividend yields because we know they have the cash to support the dividend. We think this portfolio provides a uniquely well-screened group of stocks that can help clients outperform.

New Stock Feature for June: Steelcase Inc. (SCS: $14/share)

Steelcase Inc. (SCS), a manufacturer of office furniture and other interior architectural products, is one of the additions to our Safest Dividend Yields Model Portfolio in June.

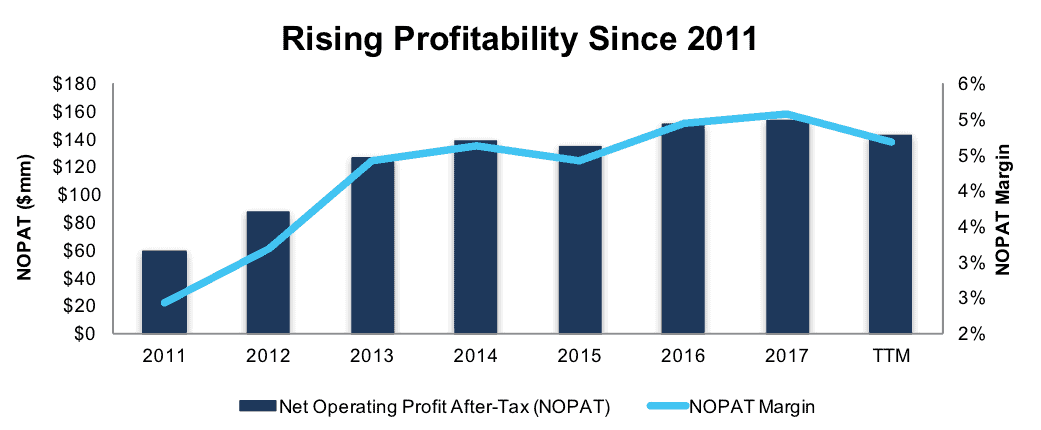

Steelcase has grown revenue by 4% compounded annually since 2011. Per Figure 1, after-tax profit (NOPAT) has grown much faster (17% compounded annually) over the same period due to an improvement in NOPAT margin from 2% in 2011 to 5% over the trailing twelve months (TTM). This strong NOPAT growth has driven return on invested capital (ROIC) to 9% (TTM) from 4% in 2011.

Longer-term, SCS has grown NOPAT by 10% compounded annually over the last 15 years, while its ROIC has improved from 1% to 9% over the same period. Add in the company’s strong free cash flow and nearly 4% dividend yield and it’s easy to see why SCS earned a spot in this month’s Safest Dividend Yields Model Portfolio.

Figure 1: SCS’ Improving NOPAT and Margins

Sources: New Constructs, LLC and company filings

Free Cash Flow Supports Dividend Growth

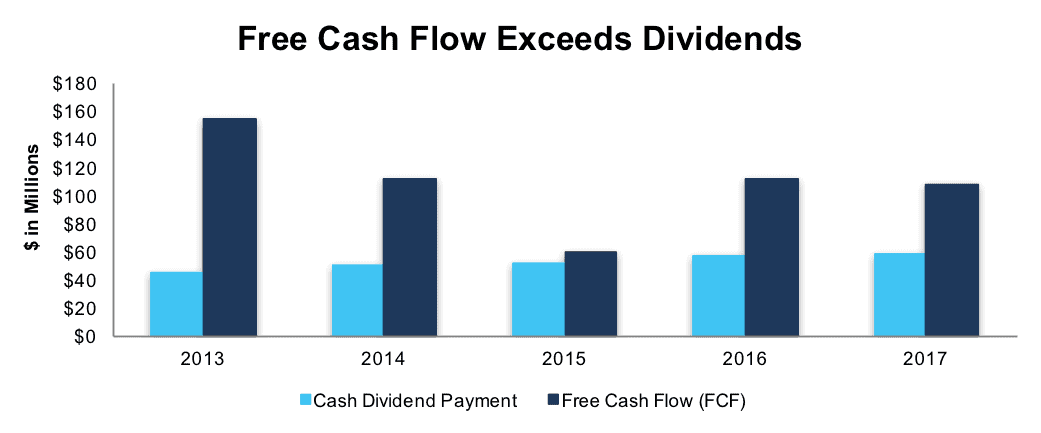

SCS has increased its quarterly dividend from $0.10 in 2Q13 to $0.13 in 2Q17, which has been made possible by Steelcase’s growing NOPAT and free cash flow. Per Figure 2, Steelcase has generated ample free cash flow to cover its cash dividend payments. Since 2007, SCS has generated a cumulative $1.3 billion (81% of market cap) in FCF and paid out cumulative dividends of just over $816 million. Steelcase’s TTM FCF of $108 million equates to a 7% FCF yield compared to 2% for the average S&P 500 stock.

Companies with strong free cash flow provide higher quality dividend yields because we know the firm has the cash to support its dividend. On the flip side, dividends from companies with low or negative free cash flow cannot be trusted as much because the company may not be able to sustain paying dividends.

Figure 2: SCS’ FCF Vs. Dividend Since 2013

Sources: New Constructs, LLC and company filings

SCS Remains Undervalued Despite Strong Fundamentals

SCS is down 16% over the past month, while the S&P is relatively flat, after the most recent earnings report came in below expectations. This overreaction to one earnings report leaves shares significantly undervalued. At its current price of $14/share, SCS has a price-to-economic book value (PEBV) ratio of 0.8. This ratio means the market expects SCS’ NOPAT to permanently decline by 20%. This expectation seems rather pessimistic for a firm that has grown NOPAT 10% compounded annually over the past 15 years.

Even if SCS were to never again grow profits from current levels, the company’s economic book value, or no growth value of the firm is $17/share – a 21% upside from the current valuation.

However, if SCS can maintain TTM NOPAT margins of 5% and grow NOPAT by just 3% compounded annually for the next decade, the stock is worth $22/share today – a 57% upside. Large upside potential coupled with SCS’ 4% dividend yield provides investors a low risk/high reward opportunity.

Impacts of Footnotes Adjustments and Forensic Accounting

Our Robo-Analyst technology enables us to perform forensic accounting with scale and provide the research needed to fulfill fiduciary duties. In order to derive the true recurring cash flows, an accurate invested capital, and a real shareholder value, we made the following adjustments to Steelcase’s 2017 10-K:

Income Statement: we made $57 million of adjustments with a net effect of removing $31 million in non-operating expense (1% of revenue). We removed $44 million related to non-operating expenses and $13 million related to non-operating income. See all adjustments made to SCS’ income statement here.

Balance Sheet: we made $1.2 billion of adjustments to calculate invested capital with a net increase of $199 million. The most notable adjustment was $393 million (31% of reported net assets) related to asset write-downs. See all adjustments to SCS’ balance sheet here.

Valuation: we made $768 million of adjustments with a net effect of decreasing shareholder value by $375 million. The largest adjustment to shareholder value was $475 million in total debt, which includes $179 million in off-balance sheet operating leases. This lease adjustment represents 11% of SCS’ market value. Despite the net decrease in shareholder value, SCS remains undervalued.

This article originally published on June 28, 2017.

Disclosure: David Trainer, Kyle Guske II, and Kenneth James receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.