This report is an abridged and free version of All Cap Index & Sectors: ROIC vs. WACC Through 3Q21, one of our quarterly series on fundamental market and sector trends.

Key Points:

- ROIC for the NC 2000[1], our All Cap Index, rose from 6.6% in 3Q20 to 8.6% in 3Q21.

- The Technology sector performed best over the past year, as measured by change in ROIC. the Consumer Non-cyclicals sector saw the smallest YoY increase in ROIC from 3Q20 to 3Q21.

- The full version of this report analyzes[2],[3] the drivers of economic earnings [return on invested capital (ROIC), NOPAT margin, invested capital turns, and weighted average cost of capital (WACC)] for the NC 2000 and each of its sectors (last quarter’s analysis is here). These reports are available to clients with a Pro or higher membership or can be purchased here.

These reports leverage more reliable fundamental data[4] that overcomes flaws with legacy fundamental datasets to provide a more informed view of the fundamentals of companies and a new source of alpha.

NC 2000 ROIC Rises Year-Over-Year in 3Q21

ROIC for the NC 2000 rose from 6.6% in 3Q20 to 8.6% in 3Q21. All eleven sectors in the NC 2000 index saw an improvement in return on invested capital (ROIC) year-over-year (YoY) based on 3Q21 financial data.

See Figure 1 in the full version of our report for the chart of ROIC vs. WACC for the NC 2000 from December 1998 through 3Q21.

Key Details on Select NC 2000 Sectors

The Technology sector performed best over the past year, as measured by change in ROIC. This trend is not surprising given that the global shutdowns accelerated the enterprise and individual shift to cloud and other software solutions. On the flip side, the Consumer Non-cyclicals sector saw the smallest YoY increase in ROIC from 3Q20 to 3Q21.

In absolute terms, the Technology sector earned the highest ROIC, by far, and the Energy sector earned the lowest. Below, we highlight the Technology sector, which has the highest ROIC and the largest YoY improvement through 3Q21.

Sample Sector Analysis[5]: Technology

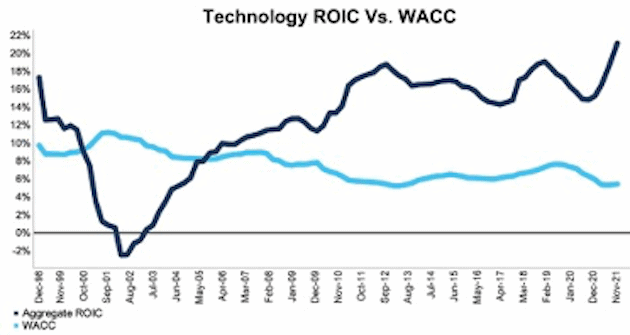

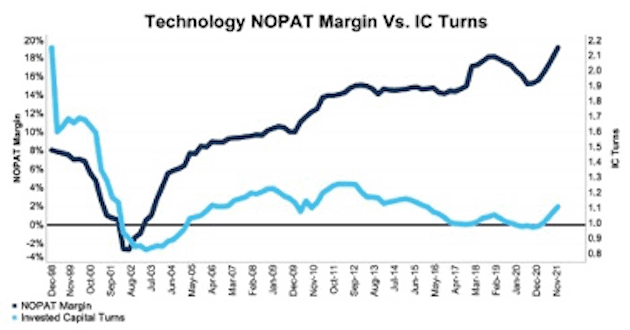

Figure 1 shows ROIC for the Technology sector rose from 15.2% in 3Q20 to 21.1% in 3Q21. The Technology sector NOPAT margin rose from 15.6% in 3Q20 to 19.1% in 3Q21, while invested capital turns rose from 0.98 in 3Q20 to 1.11 in 3Q21.

Figure 1: Technology ROIC vs. WACC: Dec 1998 – 11/16/21

Sources: New Constructs, LLC and company filings.

The November 16, 2021 measurement period uses price data as of that date and incorporates the financial data from 3Q21 10-Qs, as this is the earliest date for which all the 3Q21 10-Qs for the NC 2000 constituents were available.

Figure 2 compares the NOPAT margin and invested capital turns trends for the Technology sector since December 1998. We sum the individual NC 2000/sector constituent values for revenue, NOPAT, and invested capital to calculate these metrics. We call this approach the “Aggregate” methodology.

Figure 2: Technology NOPAT Margin Vs. IC Turns: Dec 1998 – 11/16/21

Sources: New Constructs, LLC and company filings.

The November 16, 2021 measurement period uses price data as of that date and incorporates the financial data from 3Q21 10-Qs, as this is the earliest date for which all the 3Q21 10-Qs for the NC 2000 constituents were available.

The Aggregate methodology provides a straightforward look at the entire sector, regardless of market cap or index weighting and matches how S&P Global (SPGI) calculates metrics for the S&P 500.

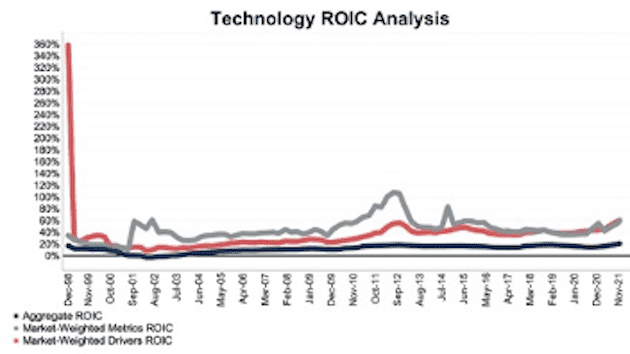

For additional perspective, we compare the Aggregate method for ROIC with two other market-weighted methodologies: market-weighted metrics and market-weighted drivers. Each method has its pros and cons, which are detailed in the Appendix.

Figure 3 compares these three methods for calculating the Technology sector’s ROICs.

Figure 3: Technology ROIC Methodologies Compared: Dec 1998 – 11/16/21

Sources: New Constructs, LLC and company filings.

The November 16, 2021 measurement period uses price data as of that date and incorporates the financial data from 3Q21 10-Qs, as this is the earliest date for which all the 3Q21 10-Qs for the NC 2000 constituents were available.

This article originally published on December 3, 2021.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

Appendix: Analyzing ROIC with Different Weighting Methodologies

We derive the metrics above by summing the individual NC 2000/sector constituent values for revenue, NOPAT, and invested capital to calculate the metrics presented. We call this approach the “Aggregate” methodology.

The Aggregate methodology provides a straightforward look at the entire sector, regardless of market cap or index weighting and matches how S&P Global (SPGI) calculates metrics for the S&P 500.

For additional perspective, we compare the Aggregate method for ROIC with two other market-weighted methodologies:

- Market-weighted metrics – calculated by market-cap-weighting the ROIC for the individual companies relative to their sector or the overall NC 2000 in each period. Details:

- Company weight equals the company’s market cap divided by the market cap of the NC 2000/its sector

- We multiply each company’s ROIC by its weight

- NC 2000/Sector ROIC equals the sum of the weighted ROICs for all the companies in the NC 2000/each sector

- Market-weighted drivers – calculated by market-cap-weighting the NOPAT and invested capital for the individual companies in the NC 2000/each sector in each period. Details:

- Company weight equals the company’s market cap divided by the market cap of the NC2000/its sector

- We multiply each company’s NOPAT and invested capital by its weight

- We sum the weighted NOPAT and invested capital for each company in the NC 2000/each sector to determine the NC 2000/sector’s weighted NOPAT and weighted invested capital

- NC 2000/Sector ROIC equals weighted NC 2000/sector NOPAT divided by weighted NC 2000/sector invested capital

Each methodology has its pros and cons, as outlined below:

Aggregate method

Pros:

- A straightforward look at the entire NC 2000/sector, regardless of company size or weighting.

- Matches how S&P Global calculates metrics for the S&P 500.

Cons:

- Vulnerable to impact of by companies entering/exiting the group of companies, which could unduly affect aggregate values despite the level of change from companies that remain in the group.

Market-weighted metrics method

Pros:

- Accounts for a firm’s size relative to the overall NC 2000/sector and weights its metrics accordingly.

Cons:

- Vulnerable to outsized impact of one or a few companies, as shown below in the Consumer Non-cyclicals sector. This outsized impact tends to occur only for ratios where unusually small denominator values can create extremely high or low results.

Market-weighted drivers method

Pros:

- Accounts for a firm’s size relative to the overall NC 2000/sector and weights its NOPAT and invested capital accordingly.

- Mitigates potential outsized impact of one or a few companies by aggregating values that drive the ratio before calculating the ratio.

Cons:

- Can minimize the impact of period-over-period changes in smaller companies, as their impact on the overall sector NOPAT and invested capital is smaller.

[1] The NC 2000 consists of the largest 2000 U.S. companies by market cap in our coverage. Constituents are updated on a quarterly basis (March 31, June 30, September 30, and December 31). We exclude companies that report under IFRS and non-U.S. ADR companies.

[2] We calculate these metrics based on SPGI’s methodology, which sums the individual NC 2000 constituent values for NOPAT and invested capital before using them to calculate the metrics. We call this the “Aggregate” methodology.

[3] Our research is based on the latest audited financial data, which is the 3Q21 10-Q in most cases. Price data is as of 11/16/21.

[4] Three independent studies prove the superiority of our data, models, and ratings. Learn more here.

[5] The full version of this report provides analysis for every sector like what we show for this sector.