We’ve compiled a "Top 11" list of the companies (who have already filed for 2014) with the largest adjustments to their balance sheets across the 11 adjustments we make.

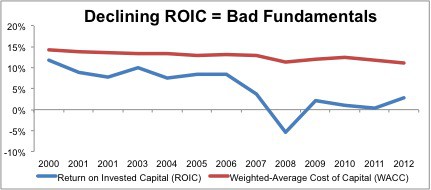

MSFT currently earns our Neutral rating, but if new CEO Satya Nadella can halt the company’s declining return on invested capital (ROIC), the stock’s valuation is cheap enough to make it intriguing.

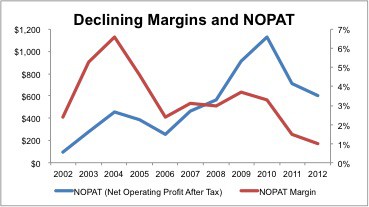

A high quality smartphone from Amazon that undercuts higher-priced competitors could mean more serious trouble for Apple’s iPhone and the company's declining profit margins.

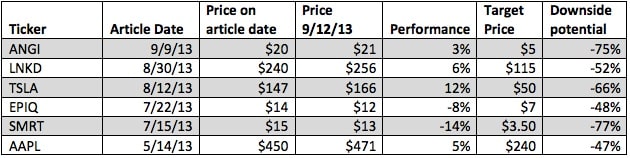

In November of last year, Netflix (NFLX: ~$355/share) landed in the Danger Zone after rising 363% year-to-date on promising quarterly results and much media hype. The stock rose rapidly for a while after our pick but has come back down nearly 20% in the past month.

Apple cannot have pricing power and market share at the same time. No one can for an extended period of time. The problem with AAPL is that it is priced for the company to achieve market share penetration and growth at high prices. The reality is that the quality of Apple products versus competitors is declining. Prices will have to come down just to maintain market share.

Online trading firms aim to exploit the gullibility of many retail investors by encouraging the myth that they can outperform professional money managers armed with vastly greater resources, experience and expertise. The E*Trade babies are the most glaring symbol of this myth. The symbol also reinforces the notion that investing is an easy task that takes no special effort or aptitude to succeed.

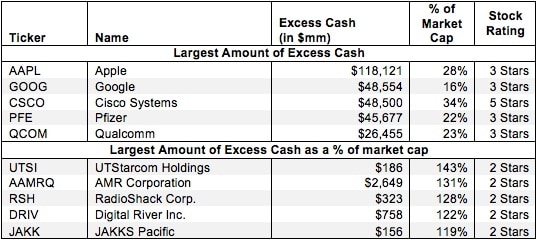

For most companies, we estimate the required amount of cash for normal business operations to be around 5% of sales. However, many companies hold cash or other liquid investments above and beyond this amount. We refer to this extra amount as excess cash. This surplus cash can be used for any number of purposes, including acquisitions, research and development, and cushioning the company against economic downturns. Excess cash is immediately available for distribution to shareholders, so we add a company’s excess cash to our calculation of shareholder value.

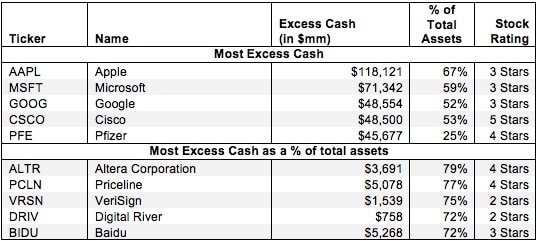

Most companies hold some cash—or cash equivalents in the form of investments—above this required amount. Companies hold excess cash in order to cushion against economic downturns, prepare for acquisitions, or any number of other reasons. Sometimes, past profits pile up on balance sheets and are a form of excess cash. Excess cash is not needed for the operations of a company. It is removed from our calculation of invested capital.

As the market bulls continue to look to rising interest rates as a sign of future strength for Citi, they ignore the fundamentals of the market and of Citi’s weak profit history.

I am optimistic about the U.S. economy and I don’t believe we are in bubble. Too many investors and economists are looking at the economy the wrong way.

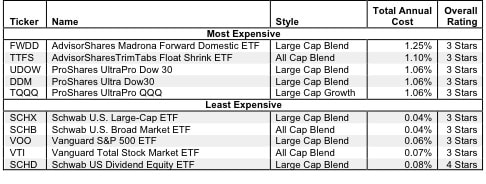

The word “index” in an ETF label does not always mean that investors are getting the specific exposure they seek. Diligence on ETF holdings is necessary despite what the providers might have you believe. Below I dispel the following myths concerning index ETFs.

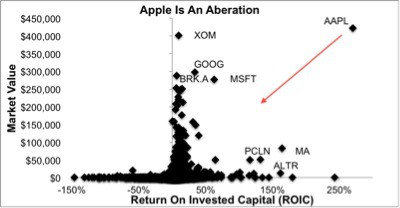

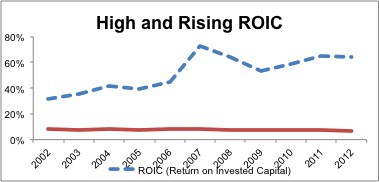

This article provides some empirical evidence behind my putting Apple (AAPL) in the Danger Zone last week because its return on invested capital (ROIC) is outrageously high. That fact underscores why valuing this company or any other with the expectation that such a high ROIC was sustainable would be a mistake.

The belief that Internet retail is or will be more profitable than traditional retail is untrue. Amazon is in a competitive, low margin business that cannot justify the profit growth implied in its valuation.

Too many investors are looking at AAPL through the rear view mirror and assume that its sky-high profits and return on invested capital (ROIC) are sustainable. As I detail in my CNBC interview, Apple is not cheap and investors should not underestimate the impact of losing Steve Jobs.