In late January, we noted that Tesla (TSLA: $342/share) CEO Elon Musk’s executive compensation plan raised significant red flags. Since then, proxy advisor Glass Lewis recommended investors vote against the proposal, which could grant Musk performance-based options worth over $2.6 billion. The red flags haven’t stopped there. More executive departures, more missed production projections, and competitors taking market share have left Tesla’s sky-high valuation with even more downside risk.

Recent Departures Fail to Stoke Confidence

The launch of the Model 3 marks a critical period for Tesla. As the company struggles to hit production targets on its first mass-market vehicle, one would hope the executive team is confident in the company’s future and working as a cohesive unit. Instead, the company is losing top executives at an alarming rate.

In February 2017, Jason Wheeler, then Tesla’s CFO left the company after being hired in 2015. Then, in early February 2018, Jon Mcneil, then Telsa’s president of global sales and services left the company to join Lyft as its chief operating officer. Just last week it was announced that Eric Branderiz, then Tesla’s Chief Accounting Officer, was leaving the company for personal reasons less than two years after joining the firm.

While speculation can run rampant about possible reasons for leaving, and we certainly hope all is well with Mr. Branderiz, one thing is known. When hired in October 2016, Mr. Branderiz was provided a $5 million equity grant that vested over four years. His abrupt departure leaves a significant portion of this grant unvested. While executive departures are rarely a good sign, they’re especially alarming when an executive is leaving big money on the table.

Production Issues Persist

Tesla continues to experience production delays at its Gigafactory. In late January CNBC reported that the company is still producing certain battery components by hand and has been forced to borrow employees from supplier, Panasonic, as it keeps pushing back its production schedule for the Model 3.

Bloomberg recently built its own Model 3 production tracker to determine how many Model 3s were being built. Using vehicle identification numbers, Bloomberg estimates that Tesla is building approximately 737 Model 3s per week. This estimate falls well below the 2,500 per week goal that Tesla hopes to achieve by the end of March. However, even this 2,500/week goal is a long-time coming. In August 2017, Tesla projected it would produce 5,000 Model 3s per week by the end of 2017. Rather than meeting these goals, a delay and subsequent lowering of goals has become the norm.

Per Figure 1, Tesla has routinely missed its initial and revised production targets since mid 2017.

Figure 1: Tesla Consistently Misses Production Estimates

![]()

Sources: Bloomberg

These Model 3 delays are just the latest in a long-line of Tesla vehicles plagued by production issues:

- Its first car, the Roadster, was pushed back from 2007 to 2008 due to production delays.

- Customers faced long wait times for the Model S due to the company’s struggles in balancing global demand.

- The Model X faced numerous delays around missing parts and issues with the “Falcon Wing” doors that ended up pushing delivery back almost two years. These problems prompted Musk to promise that Tesla would “rethink production planning.”

- Currently, Tesla is promising to produce 5,000 Model 3’s a week by the end of June, a number it was originally targeting by the end of 2017.

- Efforts to deal with Model 3 production problems led to the delay of the debut of Tesla’s electric semi-truck.

If Elon Musk can’t hit simple production targets, it’s hard to take his claims of major technological breakthroughs seriously.

Elon Musk seems to be promising the moon (and Mars) to distract from Tesla’s ongoing production issues and the fact that its competitors have matched or surpassed them on several fronts.

Competition Coming for Tesla’s Battery Advantage

In what was once believed to be a significant competitive advantage, Telsa’s Gigafactory may prove just one large production facility amidst a litany of competent competitors.

On March 13, Volkswagen AG announced that it secured $25 billion in battery supplies to begin an aggressive push into electric cars. The automaker plans to equip 16 factories (up from 3 currently) to produce electric vehicles by the end of 2022.

The company also noted that a deal for North American markets will follow shortly and, in total, it plans to purchase 50 billion euros worth of batteries. For reference, Tesla currently has $17.5 billion worth of purchase obligations related to lithium-ion cells from Panasonic.

Ignoring the fact that Tesla’s self-driving technology recently ranked last in Navigant Research’s study, competitors securing battery supplies means Tesla’s batteries may not provide the competitive advantage once hoped for. Worse yet, many of the aspirations Tesla has for its battery technology can’t be backed up. Some of its promises, like a semi-truck that can haul 80,000 pounds for 500 miles, may be feasible if battery technology continues to advance at the same rate. Other claims, like charging stations that will give those trucks 400 miles of charge in 30 minutes, appear completely impossible. To achieve the latter goal, Tesla’s charging stations would need a tenfold leap in efficiency.

Nevertheless, promises like these would lead one to believe that Tesla has made some significant breakthrough in battery technology, but we cannot find evidence to support that assertion. While the company may have a marginal advantage due to refinements to the production process and the scale of the Gigafactory (if they ever get production running smoothly), experts project the competition to catch up very soon.

Apart from Volkswagen’s heavy capital investment in battery supplies, Tesla’s scale advantage should melt away fairly quickly due to other competition. Chinese companies are targeting battery factories that would out produce the Gigafactory more than 3 to 1 by 2021. Two former Tesla executives are building their own battery factory with the backing of VW. Without some unforeseen technological breakthrough, it’s hard to see how Tesla can have any long-term competitive advantage around battery production.

First Mover Advantage Disappeared Long Ago

For a time, Tesla had the competitive advantage of being the only quality, semi-affordable electronic vehicle on the market. That’s definitively no longer the case, as the Chevy Bolt alone outsold all Tesla models combined last October, and it nearly replicated the feat in November.

In a recent head-to-head comparison in Motor Trend, three reviewers compared the Tesla Model 3, Chevy Bolt, and Nissan Leaf: only one person picked the Tesla. The reviewers highlighted certain features, such as one-pedal driving, where the competitors have definitively surpassed Tesla. Notably, the reviewers were comparing the base versions of the Leaf and Bolt, which cost $30-35 thousand, to the fully loaded Model 3 that costs more than $60 thousand. To date, Tesla has not shipped any units of the $35 thousand base Model 3.

The number of competing electronic vehicles coming out makes you wonder how many people will want to keep waiting a year or more to be able to buy the Model 3. If Tesla can’t fix its production issues soon, it may see its customers abandoning it for cheaper and more accessible options.

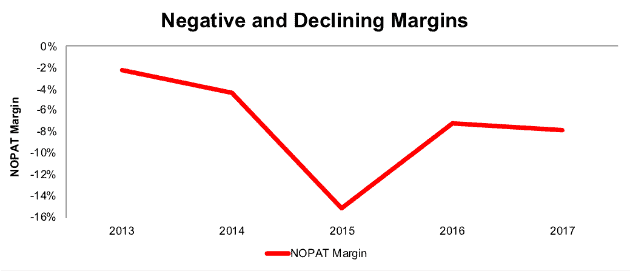

Longer-term, increased competition should put additional strain on Tesla’s already poor after-tax profit (NOPAT) margins. Reduced pricing power, combined with the eventual end of its federal tax credit, will make the company’s already precarious path to profitability that much more difficult.

Figure 2: Tesla Getting Further Away from Profitability

Sources: New Constructs, LLC and company filings

Cash Flow Burn Creates Another Disadvantage

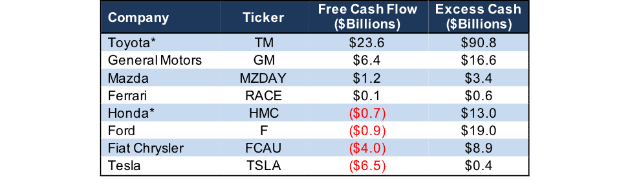

As Tesla starts to face more competition, it faces a key disadvantage compared to more established automakers. While these incumbents have steady cash-flow streams coming in from their existing business, Tesla loses money as it tries to build up production and sell its cars below cost to attract a customer base. Figure 3 shows how far behind its peers Tesla ranks in terms of free cash flow and cash on hand.

Figure 3: TSLA’s Cash Flow Disadvantage Over the Last 12 Months

* Trailing twelve-month values, not fiscal year end

Sources: New Constructs, LLC and company filings

Tesla’s lack of cash flow limits the amount it can invest compared to competitors and makes it more beholden to capital markets. Operational struggles, of which the company has had plenty, can lead to more difficulty attracting capital, which creates a negative feedback loop that could abruptly amplify problems.

Valuation Still Leaves Significant Downside

No one needs to be told that the stock price reflects enormous growth expectations, but it’s worth quantifying how unrealistic those expectations really are. Even in spite of the executive departures and growing competition, TSLA is up 7% year-to-date, which is greater than the 3% increase in the S&P 500. This price appreciation in the face of so many potential issues makes Tesla even more risky.

To justify its current price of $342/share, Tesla must achieve 8% NOPAT margins (between a mass-market and luxury car manufacturer, compared to -8% in 2017) within four years and grow revenue by 27% compounded annually for the next eight years. In this scenario, Tesla would be generating more than half General Motors’ 2017 revenue. For reference, GM produced 9.6 million cars in 2017 while Tesla produced just over 100,000. Those are ambitious expectations for a company with no track record of profitability and major problems with meeting production goals.

Even if we assume Telsa’s NOPAT margin tops out at 4% and it can grow revenue by 22% compounded annually for the next decade, the stock is worth just $161/share today. This scenario represents a 53% downside in the face of what would still be fairly impressive operating results.

Each of these scenarios also assumes TSLA is able to grow revenue, NOPAT and FCF without increasing working capital or fixed assets. This assumption is unlikely but allows us to create best-case scenarios that demonstrate how high expectations embedded in the current valuation are. For reference, TSLA’s invested capital has grown on average $4.5 billion (38% of 2017 revenue) over the past five years.

This article originally published on March 16, 2018.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

Click here to download a PDF of this report.

Photo Credit: blomst (Pixabay)

2 replies to "Time to Follow Tesla Executives and Run for the Hills?"

can you update this report

Hi James,

We’ve written several reports on Tesla since this one.

You can see our analysis of Tesla’s cash burn here

You can see how far behind Tesla is in self-driving technology here

We placed Tesla in the “micro-bubble” here

And last month we updated our analysis of Elon Musk’s stock compensation on Tesla’s valuation here