No one was surprised when United Technologies (UTX: $110/share) announced its takeover of Rockwell Collins (COL) last week. After all, a deal between the two companies had been rumored for months. By the time the official news came out, there had been plenty of time for the market to evaluate a potential merger.

The advanced warning of this merger made the market’s reaction all the more striking. UTX dropped 6% the day the deal was announced as investors balked at the $140/share price tag. The market clearly does not believe COL can generate the synergies UTX needs to create value with this acquisition, and looking at the numbers we have to agree.

Simply put, the price UTX will pay for this acquisition – which comes to ~$33 billion when accounting for all forms of debt and unfunded pension liabilities – makes it almost impossible for the deal to create long-term value for shareholders.

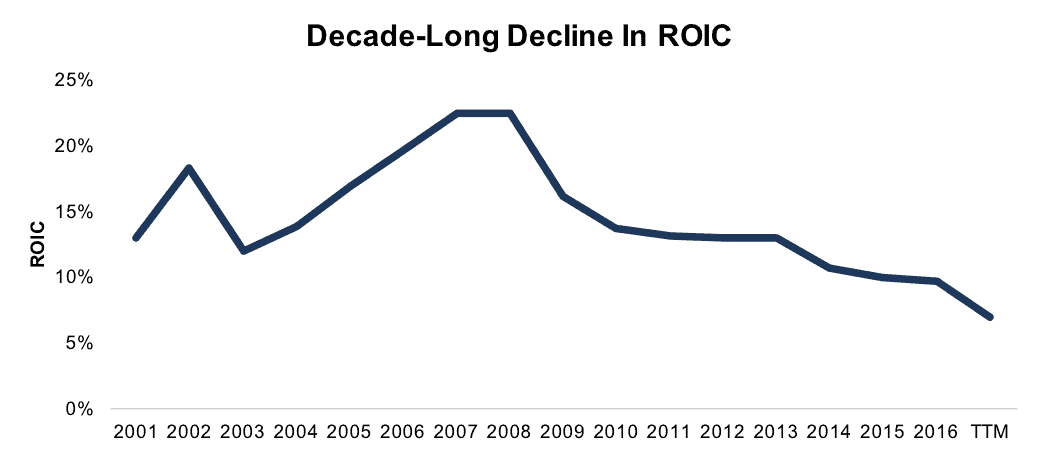

COL’s Declining Profitability

Beyond the deal’s valuation, it’s worth looking at the business UTX plans to acquire. A hefty premium may be warranted if COL were a rapidly growing, highly profitable business. However, Figure 1 makes it clear that the opposite is true. COL has seen its return on invested capital (ROIC) decline every year since 2007.

Figure 1: COL ROIC Since 2001

Sources: New Constructs, LLC and company filings.

COL’s declining profitability has gone hand in hand with a rising valuation. Even before the acquisition rumors gained steam, the stock was up nearly 30% over the prior year. UTX did not just pay a significant premium to acquire COL, it paid a premium on top of an already inflated valuation for a company with declining profitability.

Acquisition Price Implies Unrealistic Growth

When we evaluate any acquisition, we want to answer one key question: Can the acquired company generate enough after-tax profit (NOPAT) for the deal to earn an ROIC greater than the acquiring company’s weighted average cost of capital (WACC). Many mergers are “earnings accretive” but don’t meet this basic test of economic value.

A look at COL’s financials shows just how difficult it will be for UTX to earn an ROIC on this deal that exceeds its 5.1% WACC. Based on COL’s trailing twelve months NOPAT, the current deal earns an ROIC of just 2.7%. As Figure 2 shows, even if we assume significant NOPAT growth for the next five years it will be a high hurdle just for the acquisition to break even.

Figure 2: Implied Acquisition Prices for UTX to Achieve 5.1% ROIC

Sources: New Constructs, LLC and company filings.

The price UTX will pay for this acquisition only makes sense if we assume the synergies can help COL grow NOPAT by 17% compounded annually for the next five years. Even though there are significant scale and integration opportunities open to the combined companies, 17% growth for five years is an optimistic scenario.

The hurdle may grow even higher as rating agencies consider a downgrade for UTX based on the added debt it will take on. Such a downgrade would increase UTX’s cost of debt and its overall WACC.

The fact that the market took nearly $6 billion off of UTX’s market cap the day the acquisition was announced suggests that investors see some synergies in this deal, but not nearly enough to justify its lofty valuation.

Why Accurate ROIC Calculations are Important

We’ve advocated for companies to tie executive compensation to ROIC precisely to avoid overpriced acquisitions such as this one, which makes it especially surprising that UTX actually just began to tie long-term bonuses to ROIC last year.

However, a closer look at UTX’s proxy statement shows a loophole that its executives can exploit. The company’s calculation of invested capital excludes “acquisition and divestiture borrowings.” When calculating ROIC for their bonuses, UTX executives will be able to include the profit that COL generates while excluding the debt the company takes on in the acquisition.

The precise details of how companies calculate the metrics that influence executive compensation aren’t exciting, but they can have a significant impact on shareholders’ interests.

Other Risk Factors

Executives often think about the best-case scenario when considering an acquisition, but it’s also worth looking at the many ways a deal could go wrong. For UTX, the acquisition of COL creates a number of significant risk factors above and beyond the inflated valuation.

- Large acquisitions always create friction and difficulty during the integration process. Integrating COL will be especially difficult due to the fact that COL is still integrating recently acquired B/E Aerospace. Major operational setbacks due to problems with integration could cause problems for UTX, which already faces pressure from key customer Airbus over delayed deliveries.

- Both Boeing (BA) and Airbus have reacted negatively to the acquisition, with both jet manufacturers citing the combined company’s market power. It’s possible that this deal might spur Boeing and Airbus to explore more vertical integration by bringing the manufacture of key components in house, a process which Boeing has already begun.

- The deal also faces significant antitrust concerns, mostly in the EU. If regulators block the merger, UTX will have wasted significant resources that could have been better spent on the operational side.

There are many ways for this acquisition to go wrong for UTX, but the valuation means everything must go right to even begin to create value for shareholders.

This article originally published on September 12, 2017.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.