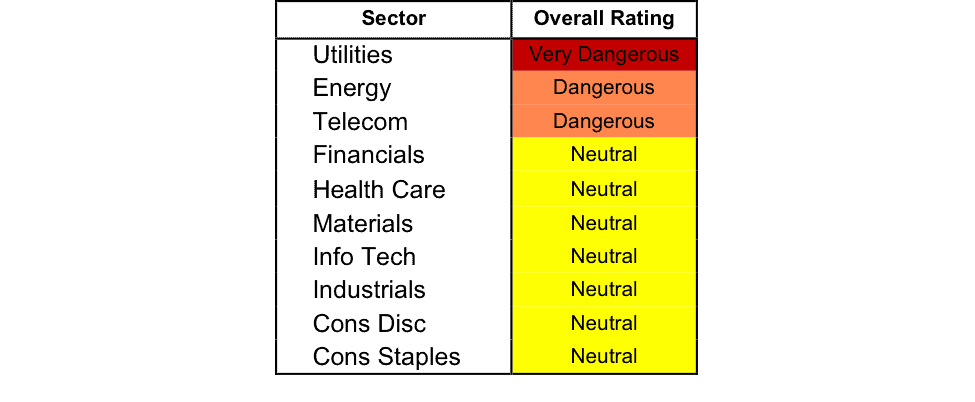

At the beginning of the third quarter of 2016, no sectors earn an Attractive-or-better rating. Our sector ratings are based on the aggregation of our fund ratings for every ETF and mutual fund in each sector. See last quarter’s Sector Ratings here.

Investors looking for sector funds that hold quality stocks should look no further than the Information Technology and Consumer Staples sectors. These sectors, despite not earning an Attractive rating overall, contain the highest percentage of assets allocated to Very Attractive or Attractive rated funds. Figures 4 through 7 provide more details. The primary driver behind an Attractive fund rating is good portfolio management, or good stock picking, with low total annual costs.

Attractive-or-better ratings do not always correlate with Attractive-or-better total annual costs. This fact underscores that (1) cheap funds can dupe investors and (2) investors should invest only in funds with good stocks and low fees.

See Figures 4 through 13 for a detailed breakdown of ratings distributions by sector. See our ETF & mutual fund screener for rankings, ratings and reports on 7000+ mutual funds and 400+ ETFs. Our fund rating methodology is detailed here.

All of our reports on the best & worst ETFs and mutual funds in every sector are available here.

Figure 1: Ratings For All Sectors

Source: New Constructs, LLC and company filings

To earn an Attractive-or-better Predictive Rating, an ETF or mutual fund must have high-quality holdings and low costs. Only the top 30% of all ETFs and mutual funds earn our Attractive or better ratings.

iShares Trust: iShares US Consumer Goods ETF (IYK) is the top rated Consumer Staples fund. It gets our Very Attractive rating by allocating over 32% of its value to Attractive-or-better-rated stocks.

Ford (F: $12/share) is one of our favorite stocks held by IYK and earns a Very Attractive rating. Ford was highlighted as a Long Idea in May 2014 and was on June’s Most Attractive stocks list. After the economic crisis in 2008, Ford’s operations have greatly improved. From 2009-2015, Ford’s after-tax operating profit (NOPAT) grew by 34% compounded annually to $7.4 billion. Over the last twelve months, Ford’s NOPAT has grown even larger, to $9.5 billion. Ford currently earns an impressive return on invested capital (ROIC) of 12%, which is up from 2% in 2009. Despite the quality fundamentals, F is down 12% year-to-date and seems currently undervalued. At its current price of $12/share, Ford has a price to economic-book-value (PEBV) ratio of 0.4. This ratio means that the market expects Ford’s NOPAT to decline by 60% over the remaining life of the corporation. This expectation seems awfully pessimistic given Ford’s profit growth since 2009. If Ford can grow NOPAT at 1% compounded annually for the next decade, the stock is worth $25/share today – a 116% upside.

Rydex Series Funds: Utilities Fund (RYUTX) is the worst Utilities fund. It gets our Very Dangerous rating by allocating over 77% of its value to Dangerous-or-worse-rated stocks. Making matters worse, it charges investors annual costs of 4.65%.

Dominion Resources (D: $78/share) is one of our least favorite stocks held by RYUTX and earns a Very Dangerous rating. From 2008-2015, Dominion’s economic earnings have declined from $392 million to -$330 million. Over the past twelve months, economic earnings have fallen further to -$497 million. Dominion’s ROIC has fallen from 7% in 2008 to 4% TTM. Despite the deteriorating fundamentals, Dominion remains overvalued. To justify its current price of $78/share, Dominion Resources must grow NOPAT by 6% compounded annually for the next 12 years. This expectation seems overly optimistic given Dominion’s inability to create shareholder value since 2008. For reference, over the last 12 years, Dominion has only grown NOPAT by 2% compounded annually, or one-third the expectations baked into the current stock price.

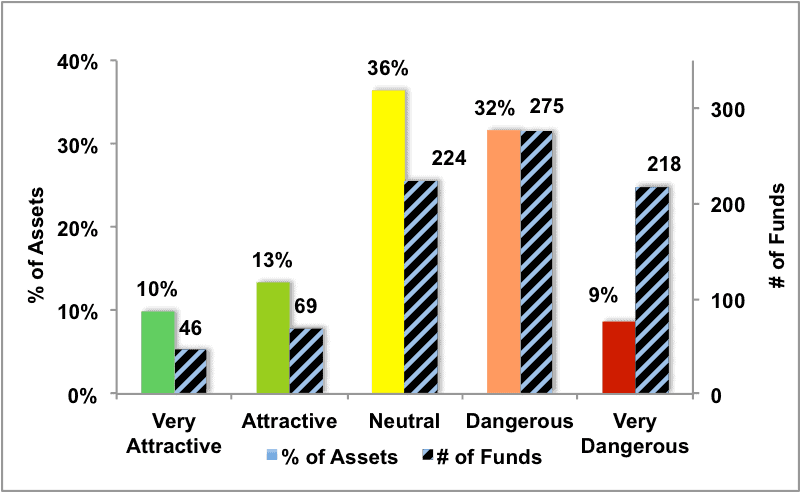

Figure 2 shows the distribution of our Predictive Ratings for all sector ETFs and mutual funds.

Figure 2: Distribution of ETFs & Mutual Funds (Assets and Count) by Predictive Rating

Source: New Constructs, LLC and company filings

Figure 3 offers additional details on the quality of the sector funds. Note that the average total annual cost of Very Dangerous funds is over nine times that of Very Attractive funds.

Figure 3: Predictive Rating Distribution Stats

* Avg TAC = Weighted Average Total Annual Costs

Source: New Constructs, LLC and company filings

This table shows that only the best of the best funds get our Very Attractive Rating: they must hold good stocks AND have low costs. Investors deserve to have the best of both and we are here to give it to them.

Ratings by Sector

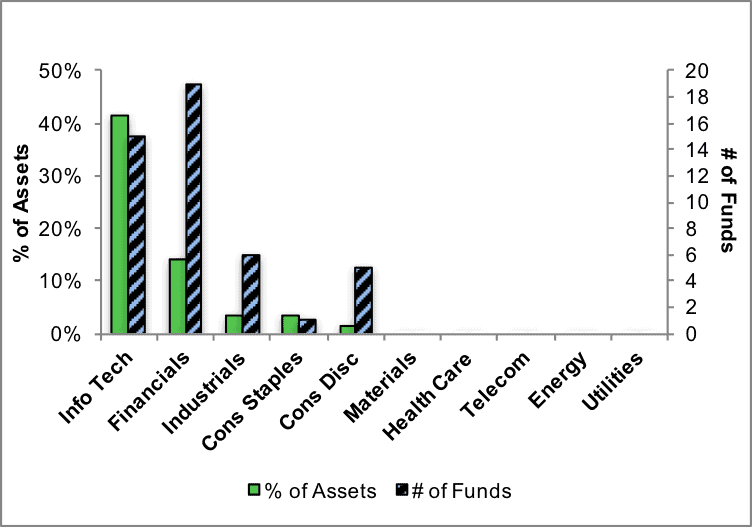

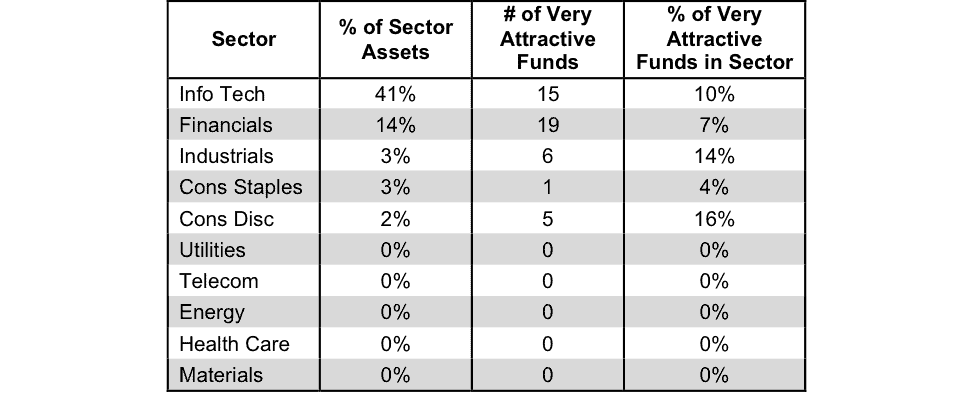

Figure 4 presents a mapping of Very Attractive funds by sector. The chart shows the number of Very Attractive funds in each sector and the percentage of assets in each sector allocated to funds that are rated Very Attractive.

Figure 4: Very Attractive ETFs & Mutual Funds by Sector

Source: New Constructs, LLC and company filings

Figure 5 presents the data charted in Figure 4.

Figure 5: Very Attractive ETFs & Mutual Funds by Sector

Source: New Constructs, LLC and company filings

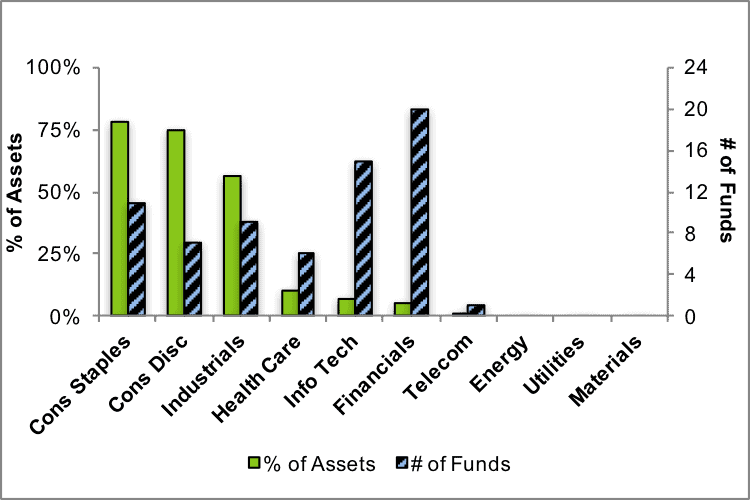

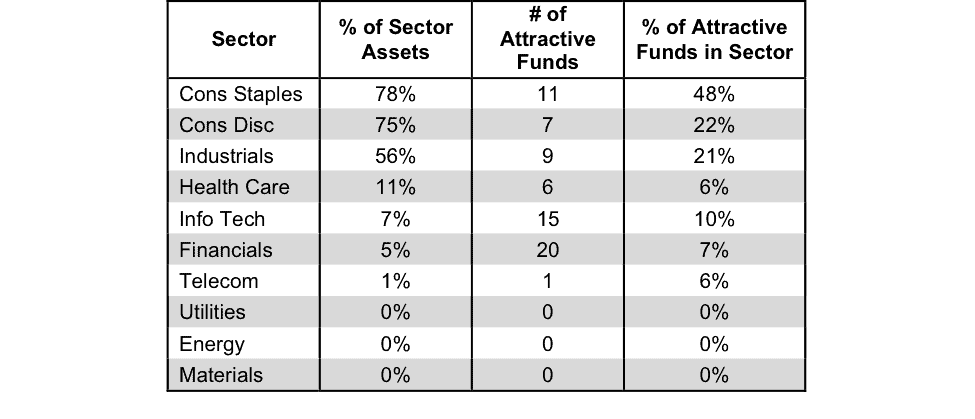

Figure 6 presents a mapping of Attractive funds by sector. The chart shows the number of Attractive funds in each sector and the percentage of assets allocated to Attractive-rated funds in each sector.

Figure 6: Attractive ETFs & Mutual Funds by Sector

Source: New Constructs, LLC and company filings

Figure 7 presents the data charted in Figure 6.

Figure 7: Attractive ETFs & Mutual Funds by Sector

Source: New Constructs, LLC and company filings

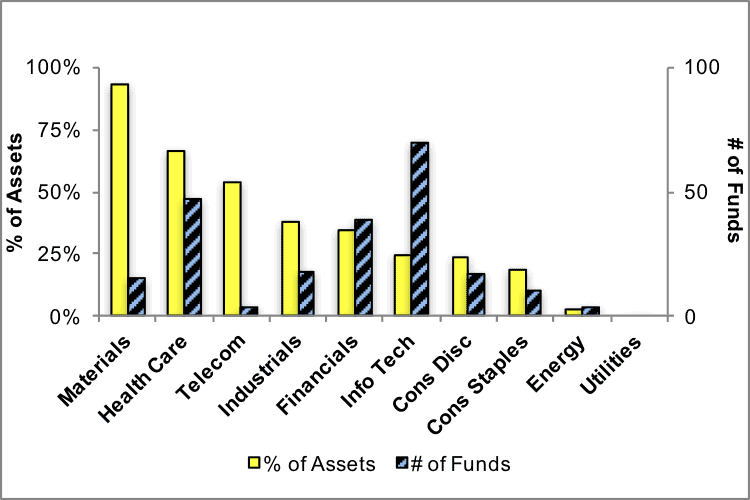

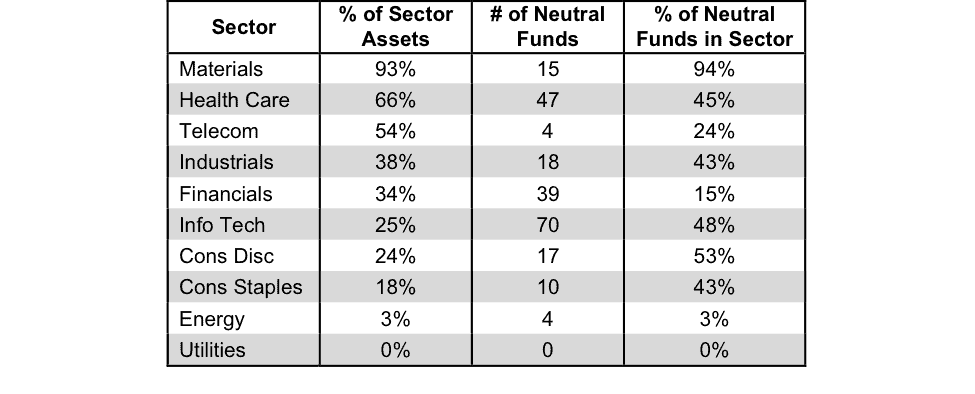

Figure 8 presents a mapping of Neutral funds by sector. The chart shows the number of Neutral funds in each sector and the percentage of assets allocated to Neutral-rated funds in each sector.

Figure 8: Neutral ETFs & Mutual Funds by Sector

Source: New Constructs, LLC and company filings

Figure 9 presents the data charted in Figure 8.

Figure 9: Neutral ETFs & Mutual Funds by Sector

Source: New Constructs, LLC and company filings

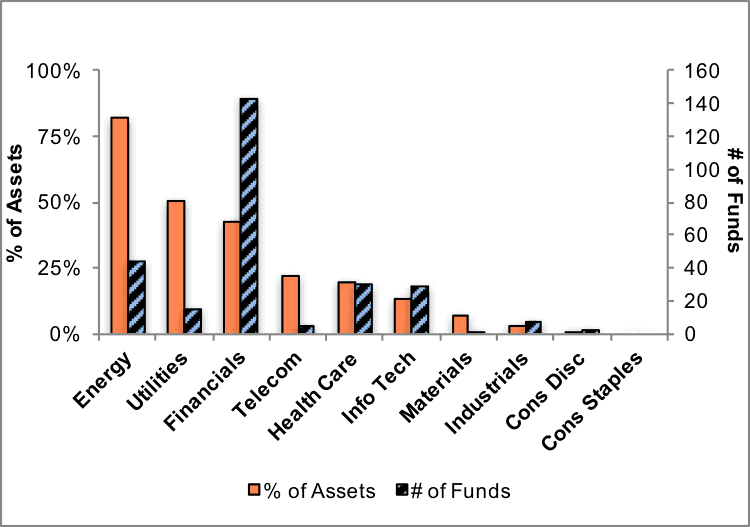

Figure 10 presents a mapping of Dangerous funds by fund sector. The chart shows the number of Dangerous funds in each sector and the percentage of assets allocated to Dangerous-rated funds in each sector.

The landscape of sector ETFs and mutual funds is littered with Dangerous funds. Investors in Energy funds have put over 82% of their assets in Dangerous-rated funds.

Figure 10: Dangerous ETFs & Mutual Funds by Sector

Source: New Constructs, LLC and company filings

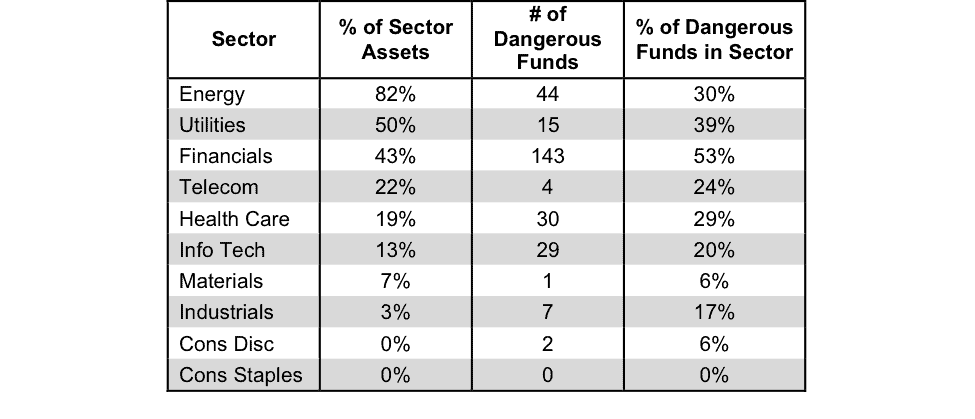

Figure 11 presents the data charted in Figure 10.

Figure 11: Dangerous ETFs & Mutual Funds by Sector

Source: New Constructs, LLC and company filings

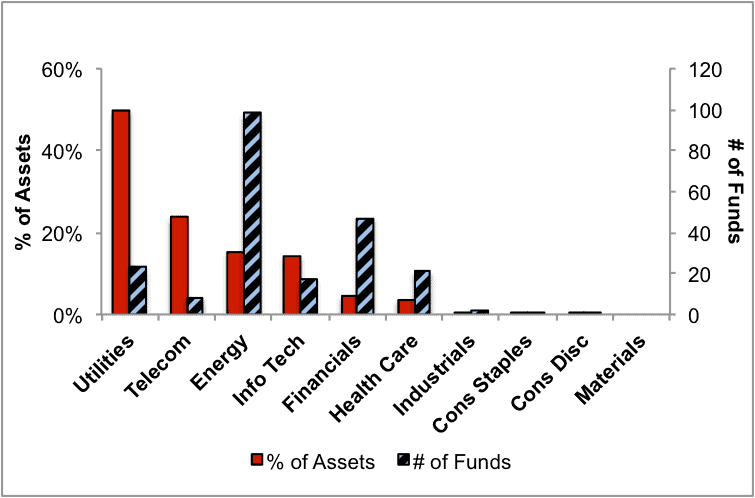

Figure 12 presents a mapping of Very Dangerous funds by fund sector. The chart shows the number of Very Dangerous funds in each sector and the percentage of assets in each sector allocated to funds that are rated Very Dangerous.

Figure 12: Very Dangerous ETFs & Mutual Funds by Sector

Source: New Constructs, LLC and company filings

Figure 13 presents the data charted in Figure 12.

Figure 13: Very Dangerous ETFs & Mutual Funds by Sector

Source: New Constructs, LLC and company filings

Disclosure: Kyle Martone owns F. David Trainer and Kyle Martone receive no compensation to write about any specific stock, sector or theme.