Our IPO research provides an alternative to the popular narratives on IPOs. This alternative deserves attention as it has warned and saved investors from losing big money on many of the worst IPOs over the last decade, such as Beyond Meat (BYND), WeWork (WE), Peloton (PTON), Klarna (KLAR), Allbirds (BIRD), Didi Global (DIDI) and more.

Space Exploration Technologies Corp (SPCX), commonly known as SpaceX, has filed to go public, and is expected to begin trading in early June. The latest reporting suggests SpaceX is targeting a $1.75 trillion valuation, which would make it the largest IPO in history. At a valuation of $1.75 trillion, SpaceX earns an Unattractive Stock Rating.

We recommend investors avoid this IPO based on the company’s:

- lack of proper internal accounting controls,

- offering almost no voting rights to investors providing $80 billion in IPO proceeds,

- obligations to use 78% of IPO proceeds to pay off existing debts,

- misleading non-GAAP reporting, and

- numerous and material red flags in related party transactions.

In our view, SpaceX’s IPO looks more like a way to lure unsuspecting investors into paying off $62.6 billion in debt (78% of expected IPO proceeds), fund an increasingly costly AI race, and lock in a trillion-dollar pay day.

The company faces real competition in its broadband and AI offerings, holds significant customer concentration risk, and flaunts a litany of related party transactions that should give any potential investor pause.

We think the projected $1.75 trillion valuation is far too high because it implies SpaceX will simultaneously generate the most revenue and profit of any company in the entire stock market. The expectations for future profits needed to justify SpaceX’s projected IPO valuation are truly out of this world.

Below, we’ll detail these risks and use our reverse discounted cash flow (DCF) model to show exactly why the projected $1.75 trillion valuation is too expensive.

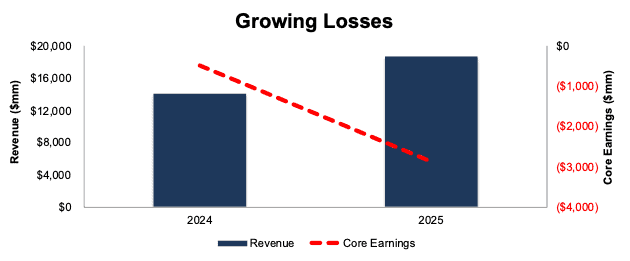

Revenue Rising, Losses Growing

SpaceX grew its revenue 33% year-over-year (YoY) in 2025, which is no small feat. At the same time, however, SpaceX’s Core Earnings fell from -$475 million in 2024 to -$2.9 billion in 2025. See Figure 1.

Figure 1: SpaceX’s Revenue & Core Earnings: 2024 – 2025

Sources: New Constructs, LLC and company filings

Total Addressable Market Could Be “Largest Ever”

There’s no doubt the combination of satellites, rocket launches, broadband, AI, space exploration, and social media create vast revenue growth opportunities for SpaceX. To justify the largest IPO in history, SpaceX should have ample growth opportunities.

In fact, the S-1 notes that the company believes they have “identified the largest actionable total addressable market (TAM) in human history.” SpaceX estimates its TAM is $28.5 trillion, which consists of:

- $26.5 trillion in AI

- $22.7 trillion in enterprise applications

- $2.4 trillion in AI infrastructure

- $760 billion in consumer subscriptions

- $600 billion in digital advertising

- $1.6 trillion in Connectivity

- $870 billion in Starlink Broadband

- $740 billion in Starlink Mobile

- $370 billion from Space-enabled solutions

Large TAM’s provide strong growth potential. But, they also invite competition. SpaceX isn’t the only company that would like to take a piece of a $28.5 trillion market. Execution risk remains high for SpaceX to achieve the expectations baked into its projected IPO valuation, as we’ll show below.

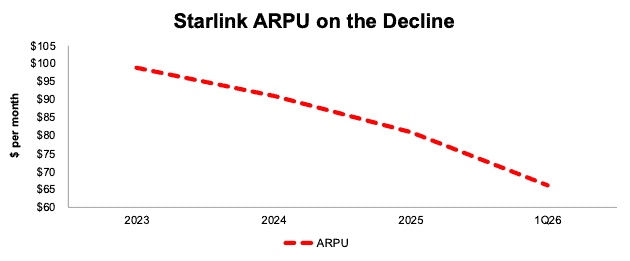

Starlink Is the Early Star

SpaceX has three reportable segments, Space, Connectivity, and AI.

The Connectivity segment is the clear standout among these segments.

In 2025, the Connectivity segment accounted for 61% of SpaceX’s revenue and reported $4.4 billion in operating income. The remaining two segments reported enough negative operating income to offset the Connectivity profits, and SpaceX as a whole reported a -$2.6 billion operating loss in 2025.

1Q26 looks similar, as Connectivity accounted for 69% of total revenue and was the only segment to report positive operating income as well.

The good news is that the Connectivity segment is growing. Starlink subscribers more than doubled from 5 million in 1Q25 to 10.3 million in 1Q26.

However, average revenue per user (ARPU) is falling fast. Starlink ARPU has fallen from $99/month in 2023 to $81/month in 2025. In 1Q26, ARPU fell even further to $66/month. Management expects ARPU to fall in the coming years as the company expands its subscriber base outside North America.

Effectively managing Starlink’s costs alongside falling ARPU remains a key execution risk, and one that must be addressed to even begin to justify SpaceX’s projected IPO valuation.

Figure 2: Starlink ARPU: 2023 – 1Q26

Sources: New Constructs, LLC and company filings

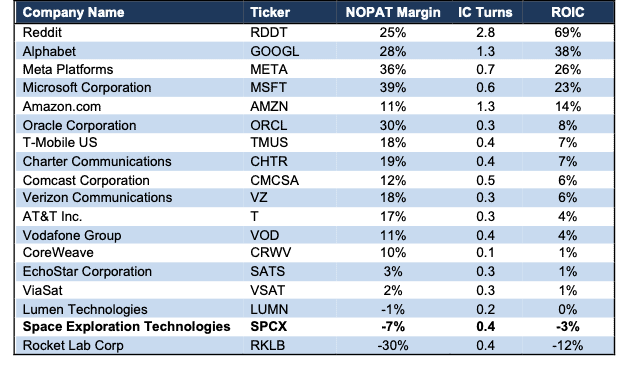

Competition is Plentiful

SpaceX faces strong competition across its three business segments. As noted above, a large TAM provides a long growth runway, but it’s naïve to assume that others do not see the same or similar opportunities. Accordingly, SpaceX notes in its S-1 it faces competition from:

- AI

- OpenAI,

- Anthropic,

- Alphabet (GOOGL),

- Meta (META),

- Microsoft (MSFT),

- Reddit (RDDT),

- And more.

- Consumer and Enterprise Broadband companies

- Verizon (VZ),Comcast (CMCSA),AT&T (T),T-Mobile (TMUS),Lumen (LUMN),Charter Communication (CHTR),GFiber,Vodafone Group (VOD),

- And more.

The company further notes that as it explores monetizing its excess compute capacity, it could emerge as a competitor to companies like CoreWeave (CRWV).

Unfortunately for potential investors, SpaceX’s profitability ranks below nearly all its competition. Per Figure 3, SpaceX has the second lowest net operating profit after-tax (NOPAT) margin and return on invested capital (ROIC) amongst its main competitors.

Figure 3: SpaceX’s Profitability Vs. Competition: TTM

Sources: New Constructs, LLC and company filings

Profitability could head the wrong direction as the company expands its AI ambitions. We’ve recently shown how the AI race is draining cash from some of the largest companies in the market. In order to compete with the hyperscalers, SpaceX will have to spend like the hyperscalers.

While the proceeds of its IPO can help meet such needs in the short-term, that money won’t last forever, and without profitable operations, SpaceX could find itself falling farther behind or diluting investors with additional capital raises in short time.

Robo-Analyst Red Flags

Below, we highlight additional red flags identified in SpaceX’s S-1.

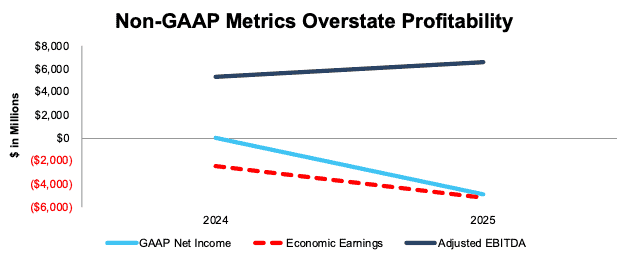

Red Flag #1: Misleading Non-GAAP Results

Many high growth and/or unprofitable companies present non-GAAP metrics to appear more profitable than they really are, in hopes of justifying a higher valuation. SpaceX is no different.

SpaceX provides investors with Adjusted EBITDA and Segment Adjusted EBITDA and, not surprisingly, these non-GAAP metrics present a more positive picture of the firm’s business than GAAP net income and our proven superior economic earnings.

For instance, SpaceX reports adjusted EBITDA of $6.6 billion in 2025. Meanwhile, GAAP net income is -$4.9 billion and economic earnings are -$5.2 billion. See Figure 4.

One of the biggest charges SpaceX removes from net income (loss) to calculate adjusted EBITDA is share-based compensation. In 2025 alone, the company removed $1.9 billion in share-based compensation when calculating Adjusted EBITDA. It’s hard to argue share-based compensation isn’t a real expense when nearly the entirety of Mr. Musk’s compensation package is share-based.

Figure 4: SpaceX’s Adjusted EBITDA, GAAP Net Income, and Economic Earnings: 2024 – 2025

Sources: New Constructs, LLC and company filings

Red Flag #2: Management Cannot Confirm Proper Internal Controls

Even after we adjust the company’s numbers to calculate true profitability, we don’t know if we can trust the financials.

The company notes in its S-1 that their internal controls over financial reporting “currently do not meet all of the standards contemplated by Section 404…”. Furthermore, the company “cannot conclude in accordance with Section 404 that we do not have a material weakness in our internal controls.”

Importantly, the company notes that through the process of updating their internal controls, they “have identified deficiencies and may identify deficiencies in the future. “

SpaceX was not required to evaluate its internal controls over financial reporting as a private company. As part of the process of preparing for its IPO, the company identified deficiencies and can’t say for sure they don’t have a material weakness in internal controls.

Weaknesses in internal controls increase the risk that the company’s financials are fraudulent and/or misleading. As the S-1 notes “Any material weaknesses could result in a material misstatement of our annual or quarterly consolidated financial statements or disclosures that may not be prevented or detected.”

It is important for investors to know that they’ve been given fair warning and will have no legal recourse to recoup any losses if the company has engaged in fraudulent financial reporting.

Red Flag #3: IPO Investors Get Almost Voting Power

As is increasingly common, SpaceX is going public with a dual class share structure. Class A shares will be offered as part of the IPO and will receive one vote per share. Class B shares will receive 10 votes pers share. This super voting class, which consists largely of Elon Musk, gives existing shareholders nearly all say over corporate governance matters.

Mr. Musk owns 12% of class A shares, 94% of class B shares, and holds 85% of the voting power in the company.

The company notes in its S-1 that “Mr. Musk will be able to elect, remove or fill any vacancy among the Class B Directors. In addition, for so long as he beneficially owns more than 50% of the voting power of our common stock, Mr. Musk will control the voting power over the selection of our board. As a result, Mr. Musk will have the power to control the outcome of matters requiring shareholder approval…”

As a result of this share and voting structure, SpaceX will be a “controlled company” under Nasdaq rules. As a controlled company, SpaceX is not required to have a majority of its board composed of independent directors or establish independent compensation and nominating committees.

New shareholders will have little to no say in the corporate governance of the company.

Red Flag #4: Paying for Elon’s Past Ventures

Famously, Elon Musk acquired Twitter (later renamed X) in 2022 in a $44 billion transaction that took the company private.

In March 2026, SpaceX took on a bridge loan of $20 billion to repay legacy X Corp and xAI debt.

Under the terms of the bridge loan, SpaceX is required to use the IPO proceeds to repay the bridge loan if other funding sources are not secured within six months after the IPO.

We don’t think it is the best use of capital to give money to SpaceX which will then be immediately used to repay billions in debt from Elon Musk’s other ventures.

Red Flag #5: Related Party Transactions Galore

Elon Musk’s companies are often intertangled as they contract and work with one another. In some instances, the companies get rolled up into one entity. Potential investors should be aware that there is a long history of covering up bad businesses through acquisition, such as Tesla’s bailout of SolarCity.

SpaceX’s S-1 reveals the latest related party transactions, or agreements between directors, executive officers, or holders of more than 5% of the company’s stock, and the company.

First and foremost, SpaceX acquired xAI in February 2026. The deal raised questions over governance, valuation, and conflicts of interest, given the interwoven leadership, namely Elon Musk, between the two companies. SpaceX is now also on the hook to repay debt of xAI as part of the bridge loan referenced above.

Beyond business acquisitions, the S-1 reveals additional related party transactions. Specifically:

- Tesla owns nearly 19 million SpaceX class A Shares, while xAI purchased $506 million worth of goods and services from Tesla in 2025.

- SpaceX owns and operates aircraft used by Elon Musk, in his capacity as CEO of Tesla, and invoices Tesla for that usage.

- In 2024, X entered into a lease agreement with a subsidiary of The Boring Company (affiliated with Elon).

- xAI leases property owned by Musk Industries, LLC, which is owned by Elon Musk.

- SpaceX is part of a service agreement with a security company owned by Elon Musk to organize and provide security for him. Expenses under this agreement totaled $2 million in 2023, $3 million in 2024, and $4 million in 2025.

Though Mr. Musk touts how he does not get paid a salary, he certainly receives significant income and services from his many entities.

Elon Musk and his companies aren’t the only related party transactions at SpaceX.

Antonio Gracias is the founder, CEO, and CIO of Valor Equity Partners. He is also a member of SpaceX’s board. Valor Equity Partners has three separate lease agreements with xAI subsidiaries for total cash obligations of $20.2 billion. The performance obligations under these agreements are guaranteed by SpaceX.

These related party transactions are material enough to warrant significant investor concern.

Red Flag #6: Potentially Astronomical Levels of Dilution

In January 2026, SpaceX granted Elon Musk 1 billion performance-based restricted shares of Class B common stock. The restricted shares only vest upon the company’s achievement of specific market capitalization milestones across 15 equal tranches, which range from $500 billion to $7.5 trillion, and the company’s establishment of a permanent human colony on Mars.

In March 2026, SpaceX cancelled Elon Musk’s previous xAI award and replaced it with 302 million performance based restricted Class B shares which vest upon market cap goals split over 12 tranches and the company’s completion of non-Earth-based data centers.

Even setting aside the loftiness of these goals, investors should be aware of the potential dilution implied if any meaningful portion of these tranches vest.

Red Flag #7: Customer Concentration Risk is Rising

SpaceX generated 21% of its revenue in 2025 from one customer. The company notes that revenue from this customer spans all three business segments. While the company doesn’t name the customer, we think it’s fair to speculate that the customer is the U.S. government.

SpaceX holds government contracts for rocket launches, xAI holds contracts with the U.S. government for access to Grok and related services, and Starlink also receives payments from the U.S government for broadband access.

Government contracts can be a great source of revenue for any business, but they’re also subject to the whims of political forces. The company notes as much in the Risk Factors section of its S-1. Specifically, “government contracts are susceptible to unilateral termination, reduction in scope, or delays at the government’s convenience”. Additionally, ‘The actual receipt of revenue on awards may never occur or may change because a program schedule could change or the program could be canceled, or a contract could be reduced, modified, or terminated early.”

Beyond the existing concentration, potential new customer concentration is on the rise. SpaceX disclosed in its S-1 that as part of a cloud services agreement, Anthropic will pay SpaceX $1.25 billion per month through May 2029. For reference, SpaceX’s entire AI segment revenue in 2025 was $3.2 billion and just $818 million in 1Q26.

Unfortunately, this revenue is not locked in via long-term contracts. Yes, the existing contract runs through May 2029. However, the agreement may be terminated by either party upon 90 days’ notice. Without diversifying this revenue stream, the company’s AI segment will be highly reliant on one customer for a material portion of its revenue.

Red Flag #8: Nearly 80% of IPO Proceeds Are Already Spoken For

Adding together the known obligations for this IPO reveals that 78.3% of the proceeds are already claimed by insiders and vendors. Here’s the math:

- $20.2 billion owed to Valor Equity Partners

- $20.0 billion to repay legacy X Corp and xAI debt

- $22.6 billion to pay Echostar (SATS) for the “Spectrum Acquisition Closing”

The total is $62.6 billion or 78.3% of the $80 billion in expected IPO proceeds.

Valuation Implies “Best In This World” Expectations

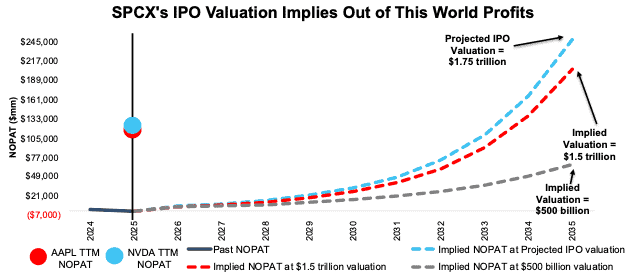

When we use our reverse discounted cash flow (DCF) model to analyze the future cash flow expectations baked into SpaceX’s, we find that the $1.75 trillion valuation embeds expectations that are, quite literally, out of this world.

Specifically, to justify a $1.75 trillion valuation, our model shows that SpaceX would have to:

- immediately improve NOPAT margin to 23% (between hyperscalers and broadband providers in Figure 3, compared to SpaceX’s -7% in 2025) and

- grow revenue by 50% compounded annually through 2035.

In this scenario, SpaceX’s revenue would reach $1.1 trillion in 2035, or 58 times higher than the company’s 2025 revenue.

For reference, Amazon (AMZN) generated the most revenue of any company in our coverage universe over the TTM. SpaceX’s implied revenue in this scenario would be 1.5x higher than Amazon’s TTM revenue. For additional context, $1.1 trillion in revenue would rank 22nd in terms of global GDP per country, right above Taiwan and below Poland. Contact us for the math behind this reverse DCF scenario.

In this scenario, SpaceX’s NOPAT would reach $248 billion in 2035, compared to -$1.3 billion NOPAT in 2025. Over the TTM, Apple (AAPL) generated the highest NOPAT ($127 billion) of any company in the U.S. To justify its projected IPO valuation, SpaceX would have to generate 2x the TTM NOPAT of Apple in 2035.

In other words, SpaceX’s projected IPO valuation implies that the company will generate the most revenue and the most NOPAT of any company in the entire market. It’s more plausible to expect SpaceX to generate either the most revenue or the most NOPAT. Expecting the company to both at the same time is a lot, to say the least.

There’s 10%+ Downside If Margins Match Broadband Peers

Even if SpaceX can maintain such high revenue growth rates, but margins fall more in-line with broadband (SpaceX’s largest segment) peers, the stock has large downside risk.

If we assume:

- NOPAT margin immediately improves to 19% (equal to Charter in the TTM), and

- revenue grows 50% compounded annually through 2035, then

the stock would be worth $1.5 trillion today – a 14% downside to the projected IPO valuation.

Even in this scenario, SpaceX’s NOPAT would reach $205 billion in 2035 and rank higher than any company in the S&P 500. Contact us for the math behind this reverse DCF scenario.

There’s 70%+ Downside If Revenue Growth Matches Historical Rates

Lastly, we put together a scenario assuming margins improve to broadband peer levels and the company’s revenue growth matches recent years’ growth rates.

If we assume:

- NOPAT margin immediately improves to 19%, and

- revenue grows 34% compounded annually (equal to SpaceX’s revenue CAGR since 2023) through 2035, then,

SpaceX would be worth just $500 billion today – a 71% downside to the projected IPO valuation. Contact us for the math behind this reverse DCF scenario.

This scenario implies SpaceX’s revenue would reach $349 billion in 2035, or 110% of Microsoft’s TTM revenue. This scenario also implies SpaceX’s NOPAT would reach $66 billion in 2035. $66 billion in NOPAT would rank higher than all but six companies of the 3,300+ we have under coverage.

Figure 5 compares SpaceX’s implied future NOPAT in these scenarios to its historical NOPAT. For reference, we include Apple and NVIDIA’s 2025 NOPAT.

Figure 5: Projected IPO Valuation Looks Too Expensive

Sources: New Constructs, LLC and company filings

Importantly, each of the above scenarios assume SpaceX grows revenue, NOPAT, and FCF without increasing working capital or fixed assets. This assumption is highly unlikely, given the capital-intensive nature of launching rockets, deploying satellites, and managing AI compute power, but allows us to create best-case scenarios that demonstrate the high level of expectations embedded in the projected IPO valuation. For reference, SpaceX’s invested capital increased 35% YoY in 2025.

This article was originally published on May 21, 2026.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Questions on this report or others? Join our online community and connect with us directly.