We published an update on PTON on Nov 22, 2021. A copy of the associated Earnings Update report is here.

Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

Luxury fitness company Peloton (PTON: $27.50/share midpoint of IPO price range) is expected to IPO on Thursday, September 26. At a price range of $26-$29 per share, the company plans to sell up to $1.1 billion of shares with an expected market cap of ~$7.6 billion. At the midpoint of the IPO price range, PTON currently earns our Unattractive rating.

Peloton’s suspect accounting and outrageous claims about its total addressable market suggest a WeWork-like perception of reality. The business is moving farther away from profitability with no realistic path to achieve the cash flows implied by its valuation. Peloton is in the Danger Zone.

Mind the (Non) GAAP

Peloton was founded in 2012 and launched its signature stationary bike in 2014. The company has sold 577 thousand products (mostly its bike, but also the treadmill it launched in 2018) and has 511 thousand subscribers to its streaming fitness classes.

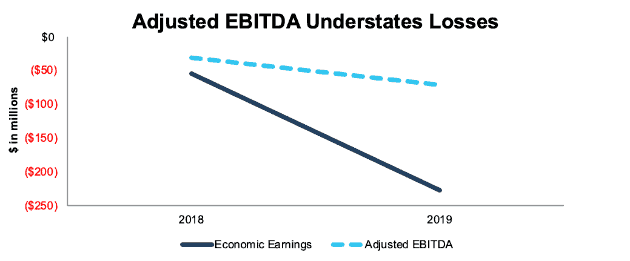

Despite its rapid growth, the company has made no progress towards profitability. Its economic earnings, the true cash flows of the business, declined from -$54 million in 2018 to -$226 million in 2019 (Peloton’s fiscal year runs through June 30).

Peloton tries to mask the extent of its losses by highlighting Adjusted EBITDA, every unprofitable company’s favorite metric. This metric excludes $90 million in stock-based compensation expense, $22 million in depreciation and amortization, $12 million in litigation expense, and $7 million in construction costs related to its new corporate headquarters. In total, Peloton’s Adjusted EBITDA excludes $124 million (14% of revenue) in expenses, while also ignoring the company’s cost of capital. More often than not, we’re seeing private companies and investors operate as if capital has no costs.

Figure 1 shows that Peloton’s Adjusted EBITDA understates both the size and the increase of the company’s losses.

Figure 1: Economic Earnings and Adjusted EBITDA for PTON: 2018-2019

Sources: New Constructs, LLC and company filings

In addition to Adjusted EBITDA, Peloton uses two other misleading non-GAAP metrics:

- Subscription Contribution Margin: Normally, contribution margin refers to the operating profits of a specific segment. In this case, however, Peloton’s Subscription Contribution Margin refers to the gross profit of its subscription offering, excluding stock-based compensation and depreciation and amortization expense. As a result, the company shows its Subscription Contribution Margin rising from 47.5% in 2018 to 50.8% in 2019. Without excluding those items, subscription gross margin declined from 43.3% to 42.7% over the same time.

- Average Net Monthly Connected Fitness Churn: Instead of disclosing its churn rate on an annual basis, as most companies do, Peloton discloses it monthly. The company’s 0.65% monthly churn (which sounds very low), annualizes to ~8% churn, which is not nearly as impressive. In addition, 11% of its subscribers are on prepaid subscriptions, which means they have no option to cancel. Peloton’s true annual churn rate for subscribers that are eligible for cancellation is probably close to double digits.

Red Flag from the Auditors

Investors need to take Peloton’s GAAP numbers with a grain of salt. The company disclosed a material weakness in its internal control over financial reporting as a risk factor in its S-1. This disclosure means Peloton didn’t have adequate technology and processes in place to ensure the accuracy of its financial statements and increases the odds that Peloton need to restate its financials in the future.

As an emerging growth company, Peloton is not required to have its auditor give an opinion on its internal controls. We applaud the company for disclosing this risk factor in its S-1, but investors should know that this disclosure is voluntary and could be eliminated in future filings even if the problem persists.

Lack of Disclosure Raises More Red Flags

Peloton omits certain details that are important for investors to understand the growth potential of the business. In particular, the company does not break out sales numbers for its new treadmill, which it launched in 2018.

The two important facts Peloton discloses about the treadmill are:

- It’s responsible for a decline in the company’s product gross margin from 44% in 2018 to 43% in 2019.

- It caused the company’s inventory balance to increase from $25 million in 2018 to $137 million in 2019, a 440% increase.

The fact that Peloton apparently has ~$100 million worth of treadmills in inventory, and that it’s earning inferior margins on those it does sell, suggests that the launch of its treadmill has not been successful. We can’t know for sure without more disclosure, but if Peloton was selling lots of treadmills it would probably be quick to tell us.

Products Are Overpriced Compared to Alternatives

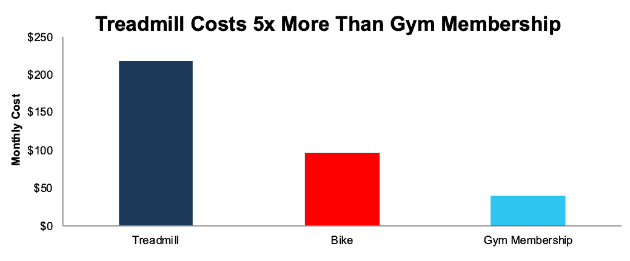

We’re not surprised that Peloton’s treadmill sales are disappointing. The $4,295 price tag is more than four times the cost of the best-selling treadmill on Amazon, the $899 NordicTrack T Series. Buyers that chose the 24-month financing option and pay for the Connected Fitness Subscription pay $217/month, which adds up to more than double the cost of the bike and more than five times the cost of the average gym membership. See Figure 2.

Figure 2: Monthly Price for PTON Treadmill and Bike vs. Average Gym Membership

Sources: New Constructs, LLC and company filings

Peloton has certain advantages over a gym membership: the ability to workout in the comfort of your own home, a wider variety of classes, and premium equipment. Still, for most people those advantages won’t be worth the extra $57/month for the bike or $178/month for the treadmill. Many gyms also offer cheaper options than the $40/month average (Bruce Springsteen works out at a $10/month gym).

Peloton claims an addressable market of 92 million households, but it’s hard to believe their products can gain that level of mass-market appeal at their current price points. It’s much more likely that Peloton will be confined to a much smaller demographic of high-income individuals.

The high price point of its products and services also makes Peloton especially vulnerable to an economic downturn. Consumers have a number of cheaper alternatives, whether that’s a gym membership, cheaper fitness apps (of which there are many), or cheaper at-home equipment. In a recession, consumers would likely flock to these substitute goods rather than pay a premium for Peloton.

Dependence on Streaming Music Rights Creates Risk

All of Peloton’s classes feature music playlists to add to the experience. The company disclosed that the fees it pays for music streaming increased by $23 million in 2019, although it doesn’t disclose the beginning value.

Peloton’s reliance on music streaming puts it in a similarly difficult situation as Spotify (SPOT), another stock on which we’re heavily bearish. Peloton’s subscribers expect to listen to music from all their favorite artists while they exercise, and the rights to that music is primarily controlled by the “Big 3” record labels – Universal, Sony, and Warner. The concentration of publishing rights in the music industry makes it hard for Peloton to exert any leverage in negotiations.

If anything, Peloton’s situation is even more difficult than Spotify and other streaming services. Because the music in these playlists is being broadcast to the entire class, Peloton has to obtain both the publishing rights and the public performance rights for the music. As a result, the rights are more expensive, and the added complexity creates more legal risk for the company.

Earlier this year, a group of over a dozen independent music publishers sued Peloton for failing to obtain the necessary rights to stream their music and are seeking $150 million in damages. Any judgement against Peloton could have a negative impact on their financials (fines, increased rights fees), or even their classes, if they’re required to remove popular music playlists.

Public Shareholders Have No Rights

Pelton is going public with a dual-class share structure. The Class A shares sold to the public will have one vote per share, while the Class B shares held by insiders and early investors get 20 votes. Upon the completion of the IPO, Class B shareholders will hold ~99% of the voting rights in the company, which means public shareholders will effectively have no say in corporate governance – a trend becoming all too normal.

DCF Model Reveals High Expectations

When we use our dynamic DCF model to analyze the future cash flow expectations baked into the midpoint of the IPO price range, we find that Peloton must achieve impressive growth and profitability in order to justify its expected valuation.

It’s hard to find a good comparison for Peloton due to its combination of fitness equipment and streaming services. Still, 79% of the company’s revenue came from equipment sales last year, so the best comparison is probably a company like Nautilus (NLS), maker of the Bowflex. Over the past 15 years, the highest after-tax profit (NOPAT) margin NLS achieved was 10% in 2015.

In order to justify the midpoint of its IPO range, $27.50/share, Peloton must achieve 15% NOPAT margins – significantly higher than NLS – and grow revenue by 32% compounded annually for 7 years. See the math behind this dynamic DCF scenario.

In this scenario, Peloton would earn $6.3 billion in revenue in year 7, or ~44% of the projected size of the global fitness equipment market. It seems unlikely that Peloton would be able to achieve premium margins and gain such a wide degree of mass market adoption at the same time.

If Peloton earns 10% NOPAT margins – equal to NLS’ company high mark in 2015 – and grows revenue by 23% compounded annually for 7 years, the stock is worth just $7/share today, a 75% downside to the midpoint of the IPO range. See the math behind this dynamic DCF scenario.

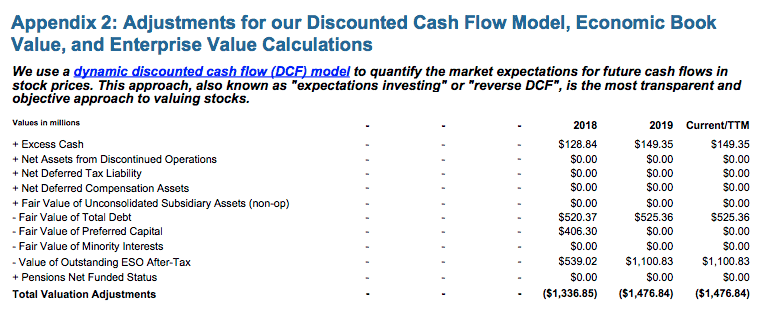

Crucially, any analysis of PTON’s valuation must account for the 64.6 million employee stock options the company has outstanding. At the midpoint of the IPO range, these options have a fair value of $1.1 billion (14% of market cap). Investors that don’t account for these options will significantly overestimate their share of future cash flows.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

As investors focus more on fundamental research, research automation technology is needed to analyze all the critical financial details in financial filings. Below are specifics on the adjustments we make based on Robo-Analyst[1] findings in Peloton’s S-1:

Income Statement: we made $35 million of adjustments, with a net effect of removing $21 million in non-operating expense (2% of revenue). You can see all the adjustments made to PTON’s income statement here.

Balance Sheet: we made $905 million of adjustments to calculate invested capital with a net increase of $148 million. You can see all the adjustments made to PTON’s balance sheet here.

Valuation: we made $1.8 billion of adjustments with a net effect of decreasing shareholder value by $1.5 billion. You can see all the adjustments made to PTON’s valuation here.

{kind=link}

This article originally published on September 23, 2019.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Harvard Business School Features the powerful impact of research automation in the case study New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.