Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

We’ve been bearish on Netflix (NFLX: $310/share) for many years, and it seems as if the market is finally catching on to the issues with the business model that we’ve seen all along. The stock is down 15% after the company missed subscriber expectations for Q2, and short interest is up 20% over the past month.

At this point, we think it’s hard to ignore all the red flags in Netflix’s fundamentals and valuation. Here’s a list of all the reasons why Netflix will struggle to justify its valuation. Netflix is in the Danger Zone.

Content Spending Not Adding Enough Subscribers

Netflix’s biggest problem is that it’s paying more and more to acquire new subscribers. Marketing and streaming content spending has risen from $308/new subscriber in 2012 to $581/new subscriber TTM . Meanwhile, revenue and subscriber growth is slowing. As we showed in “Netflix’s Original Content Strategy Is Failing”, the company’s incremental expenditures each year are ~50% higher than its incremental revenue.

Rising customer acquisition costs make it hard to see how the company reverses its trend of negative free cash flow.

Still Reliant on Licensed Content – Which It Is Losing

Despite Netflix’s heavy spending on original content, shows and movies licensed from 3rd party studios continue to drive the majority of the company’s viewing hours. Netflix does not release its own viewing data, but numbers from analytics company 7Park Data suggest that, as of last fall, licensed content accounted for 63% of viewing hours on the platform.

That same data also showed that The Office and Friends are two of the three top-streamed shows on Netflix. As we wrote about in “Loss of Licensed Content Is an Underrated Crisis for Netflix”, Netflix doesn’t appear to have a plan in place to replace these beloved shows when they depart the service in 2020 and 2021.

Benioff & Weiss Deal Reeks of Desperation

Netflix’s latest strategy to spend big bucks (and burn more cash) to sign up big name writers and producers to create original content for the platform is risky. Most recently, the company signed up Game of Thrones showrunners David Benioff and D.B. Weiss to a reported $200 million deal. Speaking to CNBC, New Constructs CEO David Trainer said this deal “reeks of desperation.”

Looking at the facts, it’s hard to see how the Benioff and Weiss deal can generate value for Netflix. The screenwriting pair have little goodwill from fans after the final season of Game of Thrones (GOT), and they don’t exactly have a huge track record of hits outside of the HBO adaptation of GOT. Plus, they’re already signed on to produce a new Star Wars trilogy for Disney (DIS), so it’s unclear how much time they’ll have to devote to Netflix shows in the near future. Netflix appears to be falling victim to “The Overvaluation Trap” and feels the need to swing for the fences in order to attempt to justify its inflated valuation. While these high-profile, fashionable deals may get some headlines, we think they will destroy shareholder value over the long-term.

Pricing Power Evaporating

Pricing power has long been one of the major bull cases for the stock. By this argument, the company is keeping its price low now to attract new customers, but the service is sticky enough that they’ll be able to raise prices in the future.

This bull case doesn’t stand up to scrutiny. Streaming services actually face relatively high churn, with 18% of streaming subscribers dropping their service each year. After its recent price increase, Netflix actually saw its U.S. subscriber base decline slightly in the most recent quarter. As we wrote in our article “Reality Is Closing in on Netflix”, the company’s price increases are not the result of pricing power, but instead a reaction to its rising content costs.

Competition Ramping Up

To the extent that Netflix has been able to sustain price increases in the past, it was due to the company’s first-mover advantage. Now, Netflix faces competition from Amazon Prime Video, HBO Now, and Hulu, and the competition is only going to get more intense. Disney, NBCUniversal (CMCSA), and Time Warner (T) are all launching their own streaming services in the next two years.

Disney’s streaming efforts, in particular, represent a significant threat to Netflix. Disney CEO Bob Iger announced on the company’s recent earnings call that it will offer a bundle of Disney+, ESPN+, and ad-supported Hulu for $12.99/month, the same price as Netflix in the U.S. As we wrote in “Disney’s Avengers Spell Endgame for Netflix”, Disney’s wildly popular tentpole franchises give it a significant edge in the streaming wars, and its ability to bundle that content with live sports and popular 3rd party shows is a major competitive advantage.

Netflix Is More Like A Traditional TV Network Now

The combination of all the above points – increased competition, lack of pricing power, and loss of licensed content – leads to a simple conclusion. Netflix is no longer a revolutionary tech platform, it’s just another TV network. We’ve been making this argument since our 2016 article, “The Spell Is Broken: Netflix Is More Like A Traditional TV Network”.

However, Netflix’s valuation does not resemble a TV network. The company has an enterprise value of $150 billion, about 5x the value of the largest standalone TV network we cover, CBS (CBS). Some people might scoff at the comparison of these two companies, but they earned about the same amount of revenue last year ($15 billion), and CBS generated $1.7 billion in free cash flow to Netflix’s -$4.5 billion.

Reliance On Credit Market Creates Risk

The only way Netflix sustains its high content spending and cash burn is through a heavy reliance on the credit market. The company raised $2 billion in debt earlier this year, bringing its total debt burden to nearly $14 billion. Given the company’s projections for continued negative free cash flow, we should expect even more debt raises on the horizon.

Part of Netflix’s high stock price can be explained by support from Wall Street. Currently, 29 out of 41 sell-side analysts rate the stock “Outperform” or “Buy”. Not coincidentally, many of those analysts work for banks that earn significant fees from underwriting Netflix’s debt deals. By contrast, 60% of independent (i.e. unconflicted) authors on Seeking Alpha are bearish on the stock.

As we wrote in “Danger Zone: Investors Who Trust Wall Street”, Netflix can’t sustain this cycle of debt-fueled growth forever. When the market turns against the company, it will create a negative feedback loop. Loss of access to cheap credit will force the company to curtail its content spending, which will hurt the growth, which will cause the stock to crash, which will make credit even harder to come by.

Valuation Remains Unrealistic

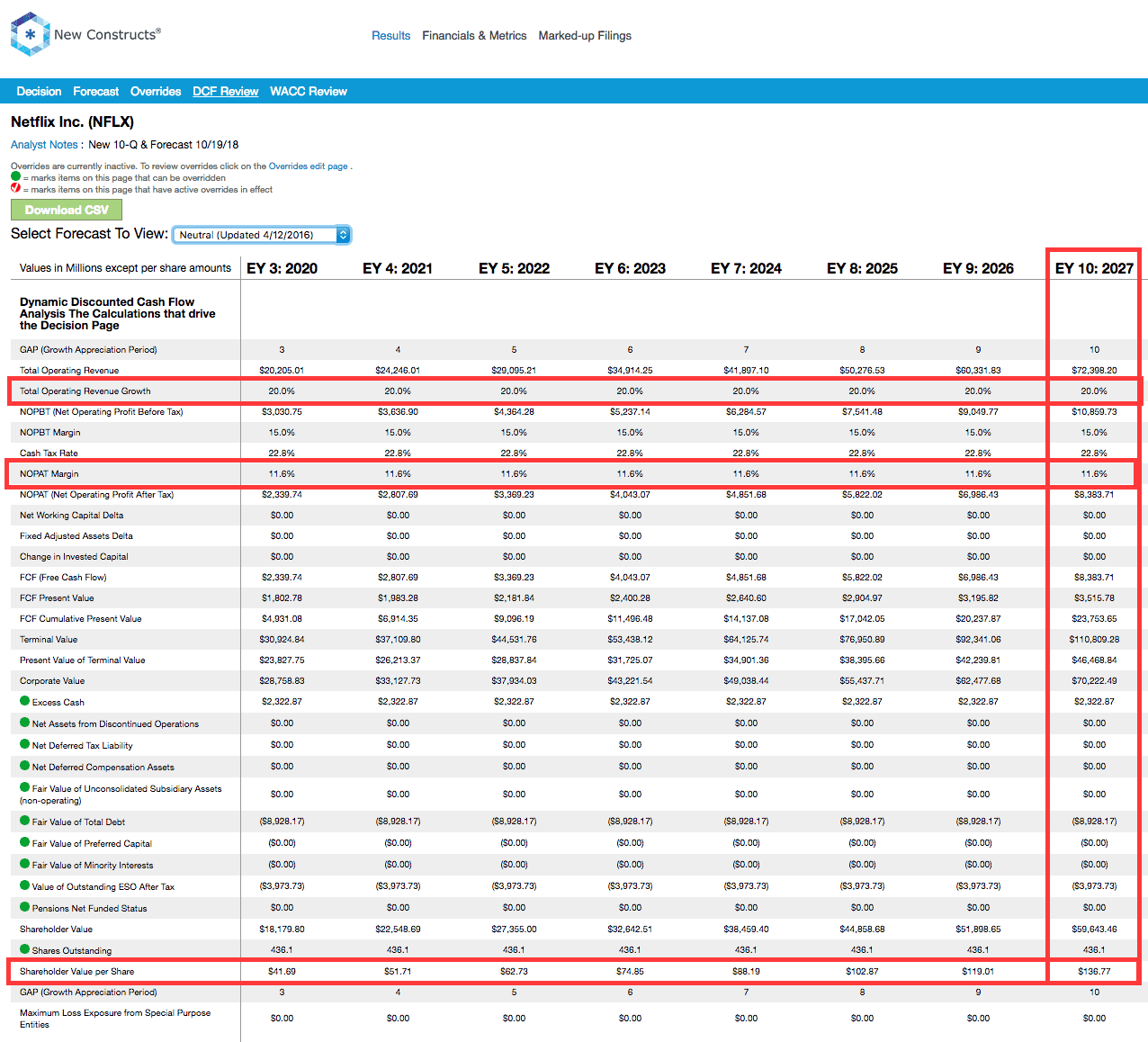

As we covered in “Netflix’s Momentum Has Run Out” and many other articles, it’s hard to create a plausible future cash flow scenario where Netflix justifies its valuation. The company’s current valuation implies that it will be able to raise its price to $20/month, achieve the same NOPAT margins as Disney, and reach 396 million subscribers over the next 8 years (compared to 151 million currently). See the math behind this dynamic DCF scenario.

{kind=link}

This scenario would require Netflix to grow subscribers by ~30 million annually, roughly its rate of growth in 2018. We don’t think it’s likely that Netflix, with its already slowing growth, could significantly raise prices and expand margins while maintaining this growth rate.

No Acquisition Bailout On the Horizon

For a long time, many investors thought Netflix would be bought by a larger competitor. However, with all the major networks/studios launching their own streaming services, it’s hard to see who’s left to acquire the company. In this respect, Netflix has been a victim of its own high valuation. Companies who considered building vs. buying a streaming service realized they could build their own platforms for far less than the cost of acquiring Netflix.

The only real remaining candidate to buy Netflix is Apple (AAPL), but that hardly seems likely given the company’s history. Apple’s largest acquisition to date was Beats Electronics for $3 billion, or ~1/50th the price of Netflix. Unless Netflix’s stock declines by a massive amount, it seems pretty clear there’s no white knight willing to bail out NFLX investors and buy the company at anywhere near its current valuation.

It’s important to remember that any acquirer doing diligence on a deal to buy NFLX has to consider not only the high price of the stock but also the high price of funding the $4 billion of annual losses the company currently incurs. In other words, any buyer would have to write one check to buy the business and keep writing checks to fund the business. So far, no one has been willing to write those checks, and we think the chances of anyone becoming willing get less every day.

This article originally published on August 12, 2019.

Disclosure: David Trainer, Sam McBride and Kyle Guske II receive no compensation to write about any specific stock, sector, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

Click here to download a PDF of this report

Photo Credit: Tim Reckmann (Flickr)

3 replies to "All The Reasons Why Netflix Is Doomed"

That may be what the traditional valuations metrics say but if you look at previous market transactions, like HBO, each subscriber was bought for around $1000. Their subscribers have higher fees but for the sake of simplicity, let us assume they cost $1000 each. Since NFLX expects to have 168M subscribers by 2019 Q4, it would be worth $168 billion, which is less than the current market capitalization of $136 billion.

I’m not sure how you’re valuing HBO since it was part of Time Warner, so we can’t be sure how much of the acquisition price AT&T paid was for HBO in particular. However, a key difference between HBO and Netflix is that HBO actually generates positive cash flow from its subscribers. HBO’s annual content budget is ~$1.5 billion, or roughly 1/10th of Netflix’s projected content spending this year. Anyone who acquires Netflix is not just paying the acquisition price, they’re also committing to sinking huge amounts of money into content spending every year if they want to keep those subscribers.

^^^ Great reply