We published an update on this Danger Zone pick on August 8, 2022. A copy of the associated report is here.

We counsel investors not to try and catch falling knives – stocks that have seen steep declines but still have further to fall. As the market rotates away from high-flying growth names to more stable cash generators, investors need reliable fundamental research, more than ever, to protect their portfolios from falling knives.

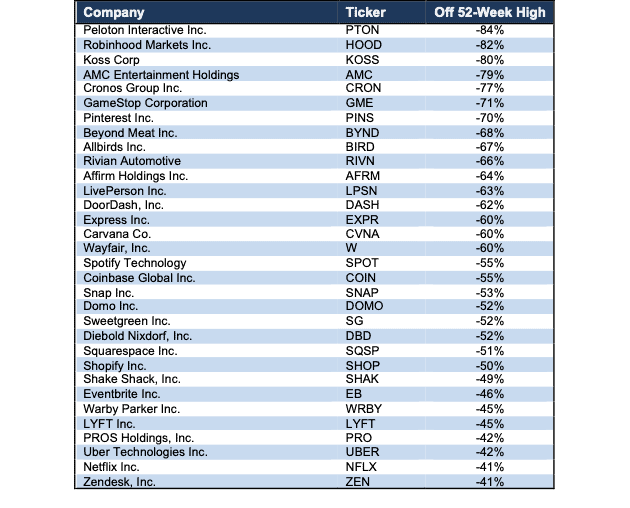

We continue to post an exceptional hit rate on spotting overvalued stocks. Currently, 62 out of our 65 Danger Zone stock picks are down from their 52-week highs by more than the S&P 500. Figure 1 lists the open Danger Zone picks that are down at least 40% from their 52-week highs. Our Focus List Stocks: Short Model Portfolio, the best-of-the-best of our Danger Zone picks, outperformed the S&P 500 as a short portfolio by 36% in 2021 with 29 out of our 31 picks outperforming the index.

This report highlights one particularly dangerous falling knife: Wayfair (W: $140/share). We highlight four other falling knives in other reports published today: Allbirds (BIRD: $12/share) here, Sweetgreen (SG: $31/share) here, Carvana (CVNA: $150/share) here, and Shake Shack (SHAK: $64/share) here. Each of these stocks have dropped at least 40% from all-time highs, yet still carry at least 40% additional downside risk.

Figure 1: Danger Zone Picks Down >40% From 52-Week High – Performance through 2/4/22

Sources: New Constructs, LLC

Falling Knife: Wayfair (W): Down 61% from 52-Wk High & 44%+ Downside Remaining

We first put Wayfair in the Danger Zone in March 2015 and most recently reiterated our thesis in January 2021. Since our most recent report, the stock has outperformed the S&P 500 as a short by 64% and the stock could fall another 44%.

While Wayfair benefited greatly from work-from-home and the accelerated shift to online shopping during COVID-19, the improvements to its business are already fading, along with demand for its products. We detail the competitive challenges Wayfair faces in our previous report here.

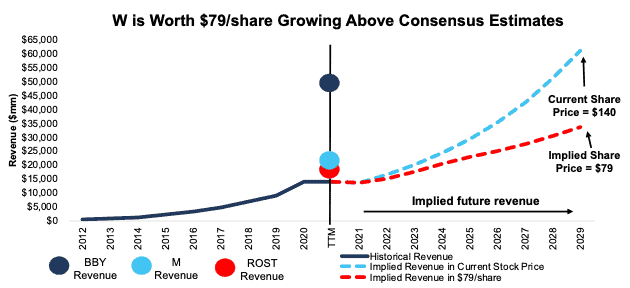

Valuation Implies Revenue 3x Higher Than Industry Peers eBay, Williams-Sonoma, & Overstock

When we use our reverse discounted cash flow (DCF) model to analyze the expectations implied by the stock price, we can show that Wayfair is significantly overvalued.

To justify its current price of ~$140/share, Wayfair must:

- immediately improve its NOPAT margin to 2.8%, (equals company’s best margin ever, achieved in 2020, which has already fallen to -1.7% in 3Q21 and 1.5% over the TTM) and

- grow revenue by 18% compounded annually for the next nine years (vs. average consensus estimate of 7% compound annual growth from 2020-2023).

In this scenario, Wayfair’s revenue in 2028 would reach $61.2 billion, which is 59% of Target’s TTM revenue and 3x the combined TTM revenue of online retailers eBay (EBAY), Williams-Sonoma (WSM), and Overstock.com (OSTK). Wayfair’s revenue in this scenario would also be greater than the TTM revenue of Ross Stores (ROST), Macy’s (M), and even Best Buy (BBY), among others.

This scenario also implies Wayfair grows NOPAT from $390 million in 2020 (only year of positive NOPAT in Wayfair’s history) to $1.7 billion in 2029, which is 1.6x greater than Williams-Sonoma’s TTM NOPAT and 61% of eBay’s TTM NOPAT.

Companies that grow revenue by anywhere near 20%+ compounded annually for such a long period are unbelievably rare, which make the expectations in Wayfair’s share price even more unrealistic, and indicate downside risk is much larger.

44% Downside if Wayfair Grows Slightly Faster Than Consensus

We review an additional DCF scenario to highlight the downside risk if Wayfair’s revenue grows more closely to consensus estimates.

If we assume Wayfair’s:

- NOPAT margin improves to 3% and

- revenue grows by 10% compounded annually over the next nine years (slightly above consensus CAGR of 7% from 2020-2023), then

the stock is worth just $79/share today – a 44% downside to the current price. This scenario still implies that Wayfair generates $33.5 billion in revenue (over 2x TTM revenue) and $938 million in NOPAT (over 4x TTM NOPAT and 88% of Williams-Sonoma’s TTM NOPAT) in 2029.

Figure 2 compares Wayfair’s implied future revenue in these three scenarios to its historical revenue. We also include the TTM revenue for Best Buy, Macy’s, and Ross Stores.

Figure 2: Wayfair’s Historical and Implied NOPAT: DCF Valuation Scenarios

Sources: New Constructs, LLC and company filings.

Each of the above scenarios also assumes Wayfair is able to grow revenue, NOPAT, and free cash flow without increasing working capital or fixed assets. This assumption is highly unlikely but allows us to create best-case scenarios that demonstrate how high expectations embedded in the current valuation are. For reference, Wayfair’s invested capital has increased by an average of $70 million over the past five years.

Fundamental Research Provides Clarity in Frothy Markets

2022 has quickly shown investors that fundamentals matter and stocks don’t only go up. With a better grasp on fundamentals, investors have a better sense of what and when to buy and sell – and – know how much risk they take when they own a stock at certain levels. Without reliable fundamental research, investors have no reliable way of knowing whether a stock is expensive or cheap.

As shown above, disciplined, reliable fundamental research shows that even after plummeting, Allbirds, Sweetgreen, Carvana, Wayfair, and Shake Shack still hold significant downside.

This article originally published on February 7, 2022.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.