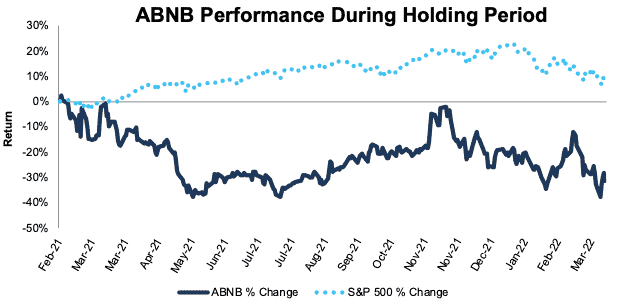

We first put Airbnb (ABNB: $145/share) in the Danger Zone in February 2021. Since then, the stock is down 31% compared to an 8% gain for the S&P 500. Though the company set records across many of its top-line performance metrics in 2021, the likelihood of the company achieving the cash flow expectations baked in the stock price remain very low.

We leverage more reliable fundamental data[1], shown to provide a new source of alpha, with qualitative research to pick this Danger Zone idea.

Airbnb’s Stock Could Fall Further Based on:

- continued cash burn despite growing the top line

- expected decline in average daily rate (ADR) will pressure margins

- guidance for 2022 implies a pullback from 2021, but the stock is priced for the opposite

- current valuation of the stock implies Airbnb will be larger than Booking (BKNG), Expedia (EXPE), Trip.com (TCOM), and TripAdvisor (TRIP) combined. Anything less and the stock could have 66%+ downside

Figure 1: Danger Zone Outperformance of 39%: From 2/10/21 Through 3/11/22

Sources: New Constructs, LLC

What’s Working

Record top-line metrics: In 2021, Airbnb saw record results in its top-line metrics, as consumers returned to travelling after 2020 pandemic lockdown measures had kept most at home. Specifically, (each figure year-over-year [YoY]):

- nights and experiences booked grew 56% in 2021

- gross booking value (GBV) grew 96% in 2021

- revenue grew 77% in 2021

- average daily rate (ADR) was up 20% in 4Q21

- adjusted EBITDA (while not a reliable measure of profits) was positive $1.6 billion, up from -$251 million in 2020 and -$253 million in 2019

Expenses kept under control: Airbnb laid off 25% of its workforce in 2020, and the resulting cost savings were maintained through 2021. As a result Airbnb achieved its first positive net operating profit after-tax (NOPAT) margin since going public. However, based on management’s guidance, we do not expect a further improvement in margins in 2022.

What’s Not Working

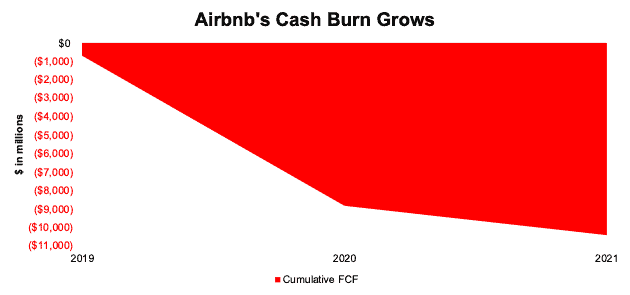

Still burning cash: Despite lower operating expenses as a percent of revenue in 2021 (compared to both 2019 and 2020), Airbnb still burned through $1.6 billion in free cash flow (FCF) in 2021. Over the past three years, Airbnb burned a cumulative $10.4 billion in FCF.

Figure 2: Airbnb’s Cumulative Free Cash Flow: 2019-2021

Sources: New Constructs, LLC and company filings

2021 positive conditions not likely to repeat: For investors hoping for another year like last year for Airbnb, we, and management, recommend pumping the brakes. In its 2022 guidance, management not only pointed out that “forecasting several quarters out remains challenging given continued COVID-related uncertainties”, but also recommended indexing 2022 growth to 2019, rather than 2021. In other words, 2021 was exceptional.

First, consumers delayed travel in the beginning of 2021, which drove abnormally higher bookings in Q2. Going forward, management expects a return to historical seasonality, which means more volatility in Airbnb’s results, and chances for earnings misses moving forward.

Second, Airbnb benefited from more bookings in North America, which per management, has a higher ADR than other geographic regions. In 2022, management expects ADR to fall from 2021 levels as international travel returns and Asia-Pacific removes some of the more stringent COVID-19 restrictions.

While not a reliable measure of profits, we can still glean valuable insights from management’s guidance for the direction of adjusted EBITDA. Given the expected decline in ADR noted above, management expects adjusted EBITDA margin to be in line with 2021. In other words, don’t expect an improvement in profitability in 2022.

Slowing growth by itself is not a problem if the stock is priced accordingly. However, Airbnb’s valuation, even after falling, does not reflect stagnant profitability and slowing growth. Details below.

Airbnb Still Priced to be the Largest Lodging Business

Despite ABNB falling 33% since its 52-week high, the stock is still significantly overvalued. Below, we use our reverse discounted cash flow (DCF) model to illustrate the lofty expectations for future cash flows implied by Airbnb’s current valuation.

To justify its current price of $145/share, Airbnb must:

- improve NOPAT margin to 20% (more than 2x 2021 margin and greater than Booking’s 2021 NOPAT margin of 17%) and

- grow revenue by 30% compounded annually through 2030 (greater than consensus estimates of 24% CAGR from 2021-2024

In this scenario, Airbnb would earn nearly $65 billion in revenue in 2030, which is 11x Airbnb’s 2021 revenue, 6x Booking’s 2021 revenue, and 3x the trailing-twelve-month (TTM) combined revenue of Booking, Expedia, Trip.com, and TripAdvisor. At Airbnb’s TTM take rate, or the revenue generated per GBV (total sales on the platform), the scenario above implies ABNB achieves $505 billion in gross booking value in 2030. For reference, the entire global hotel and other travel accommodation market was worth an estimated $802 billion in 2021.

Note that companies that grow revenue by 20%+ compounded annually for such a long period are unbelievably rare. Accordingly, we see the cash flows expectations in Airbnb’s share price as unrealistically high, which indicates downside risk is much larger than upside potential.

ABNB Has 48%+ Downside: If we assume Airbnb’s:

- NOPAT margin improves to 20%,

- revenue grows at consensus rates in 2022, 2023, and 2024 (32%, 20%, and 21%), and

- revenue grows by 21% (continuation of consensus) each year from 2025-2030, then

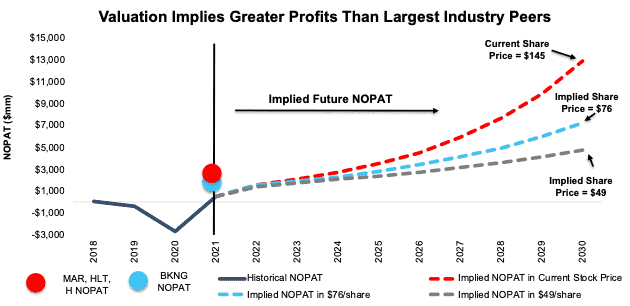

ABNB is worth just $76/share today – a 48% downside. Airbnb would still earn $36 billion in revenue in 2030, which is 6x its 2021 revenue, 3x Booking’s 2021 revenue, and 1.6x the combined 2021 revenue of hotel giants Marriott (MAR), Hilton (HLT), and Hyatt (H). Additionally, this scenario implies Airbnb generates $7.2 billion in NOPAT, which is 14x its 2021 NOPAT, 4x Booking’s 2021 NOPAT, and 1.6x Booking’s highest ever NOPAT, which was earned in 2018.

ABNB Could Have 66%+ Downside: Should 2022’s expected flatlining of profitability or ADRs remain lower for longer than expected, the downside is even larger. If we assume Airbnb’s:

- NOPAT margin improves to 18% (double 2021 NOPAT margin),

- revenue grows at consensus rates in 2022, 2023, and 2024 (32%, 20%, and 21%), and

- revenue grows by 15% each year from 2025-2030, then

ABNB is worth just $49/share today – a 66% downside. In this scenario, Airbnb would still earn $27 billion in revenue in 2030, which is 4x its 2021 revenue and nearly 2x Booking’s highest ever revenue, which was achieved in 2019. This scenario also implies Airbnb generates $4.7 billion in NOPAT, which is 9x its 2021 NOPAT and 2.5x Booking’s 2021 NOPAT.

Figure 3 compares Airbnb’s implied future NOPAT in this scenario to its historical NOPAT as well as Booking’s 2021 NOPAT and the combined 2021 NOPAT of Marriott, Hilton, and Hyatt.

Figure 3: Airbnb Historical and Implied NOPAT: DCF Valuation Scenarios

Sources: New Constructs, LLC and company filings

Each of these scenarios also assumes Airbnb can grow revenue, NOPAT, and free cash flow (FCF) without increasing working capital or fixed assets. This assumption is unlikely but allows us to create best-case scenarios that demonstrate how high expectations embedded in the current valuation are. For reference, Airbnb’s invested capital has grown 377% compounded annually since 2019.

Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

This article originally published on March 14, 2022.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, sector, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Our research utilizes our Core Earnings, a more reliable measure of profits, as proven in Core Earnings: New Data & Evidence, written by professors at Harvard Business School (HBS) & MIT Sloan and published in The Journal of Financial Economics.