We published an update on this Danger Zone pick on October 14, 2024. A copy of the associated report is here.

We first put Affirm Holdings (AFRM: $21/share) in the Danger Zone in October 2021, reiterated our bearish opinion on the stock multiple times, and named it a Zombie Stock in September 2022. See all our reports on Affirm here.

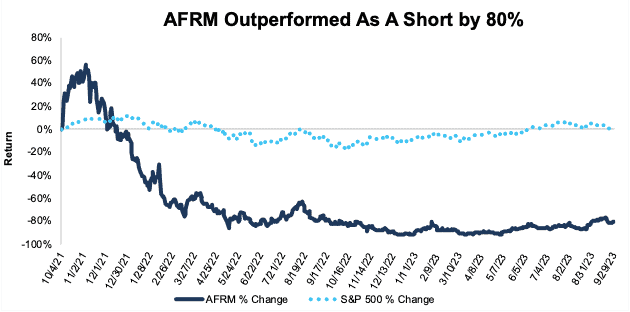

Since our original report AFRM is down 81% while the S&P 500 is down 1%, but the stock is up 120% year-to-date (YTD), movement that is untethered to reality. With a recently confirmed, yet undisclosed SEC investigation ongoing and the New York Fed’s recent findings that “those with lower credit scores and greater unmet credit needs make up a disproportionate share of all buy now pay later (BNPL) users”, the stock is looking increasingly overvalued. We believe that the company cannot meet the future cash flow expectations baked into its stock price.

Affirm Holdings’ Stock Could Fall Further Based on:

- revenue not growing fast enough to cover operating expenses,

- margin pressure and rising cash burn,

- unprofitable business in a profitable industry and

- a stock valuation that implies Affirm will grow gross merchandise volume (GMV) to nearly half of Amazon’s current GMV.

Figure 1: Affirm Outperformance As a Short From 10/4/21 Through 9/29/23

Sources: New Constructs, LLC

What’s Working

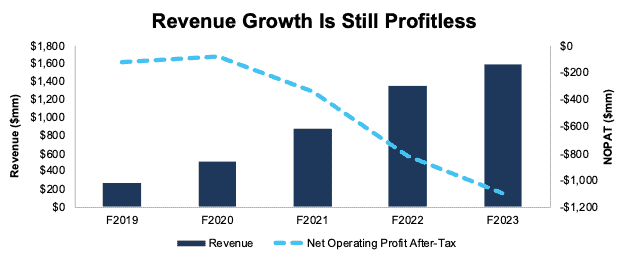

Affirm has successfully grown revenue, which has increased year over year (YoY) every year since fiscal 2019 (earliest data available in our system). The company has grown its GMV from $2.6 billion in fiscal 2019 to $20.2 billion in fiscal 2023, a 6.7x increase. In addition, the company’s active consumers grew from 2 million to 16 million, a 7x increase, over the same period.

While the top-line growth has certainly been impressive, the company has not made any progress on the bottom-line, as we’ll detail below in the “What’s Not Working” section.

What’s Not Working

Affirm Remains Unprofitable

Affirm’s net operating profit after tax (NOPAT) declined from -$124 million in fiscal 2019 to -$1.1 billion in fiscal 2023. Affirm’s NOPAT margin fell from -47% to -69% while its ROIC declined from -18% to -39% over the same period.

Falling NOPAT and ROIC highlight Affirm’s inefficient business model and the lack of rationality in the YTD stock price movement.

Figure 2: Affirm’s Revenue and NOPAT from Fiscal 2019 to Fiscal 2023

Sources: New Constructs, LLC and company filings

Zombie Stocks Are Inherently Risky

Companies with fast-depleting cash reserves are risky investments in any market. These risks are higher when the cost of raising capital increases. When we first named Affirm a Zombie Stock, we noted it had just 10 months until running out of cash. Cash burn increased in fiscal 2023. However, Affirm was able to raise new capital and lengthen its runway. In fiscal 2022, the company issued $1.7 billion in convertible senior notes for “general corporate purposes” and to fund “plans for future growth.”

Affirm now has 21 months of runway from the end of September 2023, based on its fiscal 2023 free cash flow (FCF) burn, which totals -$1.1 billion. More details in Figure 3. The fact remains that, without a significant improvement in operations, Affirm will run out of cash or have to raise expensive new capital.

Figure 3: Affirm Has a Short Runway to Avoid Bankruptcy

Sources: New Constructs, LLC and company filings.

* As of 6/30/23

** To calculate “Months till Bankruptcy” we divided the TTM FCF burn, excluding acquisitions, by 12 to get the monthly cash burn. We then divide reported cash and equivalents and long-term investments in the most recent 10-K by the monthly cash burn.

Affirm Increasingly Burning Cash

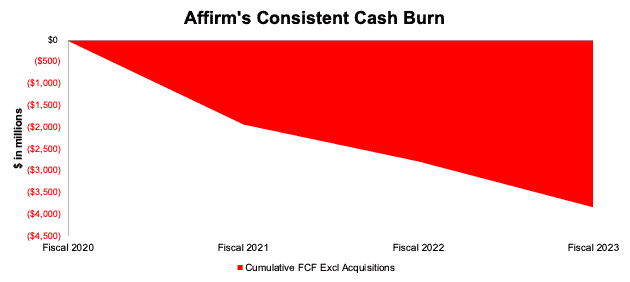

Affirm’s FCF has been negative on both an annual and quarterly basis in every year of our model. From fiscal 2020 through fiscal 2023, Affirm burned through a cumulative $3.8 billion in FCF excluding acquisitions. In fiscal 2023, the company’s cash burn sits at -$1.1 billion.

Figure 4: Affirm’s Cumulative Free Cash Flow: Fiscal 2020 Through Fiscal 2023

Sources: New Constructs, LLC and company filings

Competition Is More Profitable

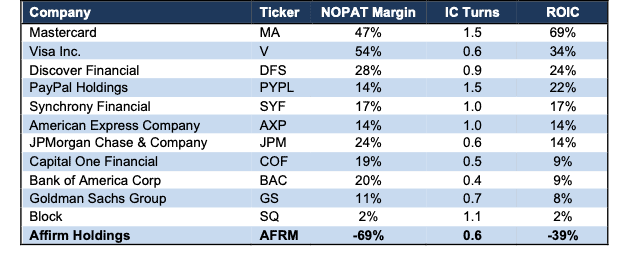

Affirm’s competitive position versus peers has worsened since our last report, as competitors introduce their own installment payment plans and other similar offerings. The company still has by far the worst profitability out of all its competitors within our coverage universe. In fiscal 2023, Affirm’s ROIC fell to its lowest level ever, -39%.

Per Figure 5, Affirm’s NOPAT margin, invested capital turns, and ROIC all rank below competitors such as Discover Financial (DFS), JPMorgan Chase & Company (JPM), Mastercard (MA), Visa Inc. (V), Block (SQ), PayPal (PYPL), and many more.

Figure 5: Affirm Profitability Vs. Competitors: TTM

Sources: New Constructs, LLC and company filings

Costs Are Still Growing Faster Than Revenues

In Affirm’s quest to take market share, it has adopted a growth-at-all-costs approach, which results in the highly negative margins pointed out above. Since fiscal 2019, Affirm has grown revenue 57% compounded annually. However, sales & marketing costs, general & administrative costs, and technology & data analytics costs have all grown faster, per Figure 6.

The situation isn’t getting any better, either. In fiscal 2023, S&M, G&A, and T&DA grew 20%, 2%, and 47% YoY respectively, while revenue grew 18% YoY.

Total operating costs reached 176% of revenue in fiscal 2023, which is up from an already high 148% of revenue in fiscal 2019.

Figure 6: Affirm Expense Growth Since 2019

Sources: New Constructs, LLC and company filings

Current Price Implies Affirm’s GMV Reaches Almost Half the GMV of Amazon

Below, we use our reverse discounted cash flow (DCF) model to analyze the future cash flow expectations baked into Affirm’s stock price. Affirm’s stock is priced as if the business will significantly improve profitability and also generate nearly half the GMV of Amazon, a feat that is highly unlikely. We also present additional DCF scenarios to highlight the downside risk in the stock if Affirm fails to achieve these overly optimistic expectations.

To justify its current price of $20/share, our model shows that Affirm would have to:

- immediately improve NOPAT margin to 11% (Goldman Sachs’ TTM NOPAT margin vs. Affirm’s -69% NOPAT margin in fiscal 2023) and

- grow revenue 28% (1.6x Affirm’s revenue growth in fiscal 2023 and above projected industry growth rate through 2030) compounded annually through fiscal 2031.

In this scenario, Affirm’s revenue would reach $11.4 billion in fiscal 2031, or over 7 times higher than the company’s fiscal 2023 revenue. In this scenario, Affirm’s NOPAT would also reach $1.3 billion in fiscal 2031 compared to the company’s -$1.1 billion in fiscal 2023.

If we assume Affirm maintains a revenue per GMV rate of just under 8% (equal to fiscal 2023, down from 9% in fiscal 2022), then this scenario implies Affirm’s GMV in fiscal 2031 equals $145 billion, which is also 7 times Affirm’s fiscal 2023 GMV.

For context, Amazon’s (AMZN) 2022 (calendar year) U.S. GMV was $368 billion. In other words, Affirm would need to generate almost half the GMV of Amazon simply to justify its current valuation.

We are still, if not even more, skeptical of any buy now pay later (BNPL) firm ever achieving such high merchandise volume, especially while drastically improving margins given the intense competition in the market. Also, keep in mind, the number of companies that grow revenue by 20%+ for such a long period are also “unbelievably rare”, making the expectations in Affirm’s share price look even more unrealistic.

There’s 57%+ Downside if Consensus Growth is Realized

If we assume Affirm:

- immediately improves NOPAT margin to 6% (3x Block’s 2% NOPAT margin) and

- grows revenue by consensus estimates in fiscal 2024 (19%), 2025 (23%), and 2026 (25%), and

- grows revenue by 26% (projected industry growth) compounded annually through fiscal 2031, then

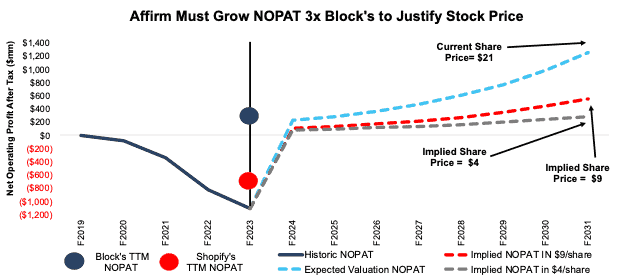

the stock would be worth just $9/share today – a 57% downside to the current price.

This scenario implies that Affirm generates $8.6 billion in revenue in fiscal 2031, which would be over 5.4x its TTM revenue. In this scenario, Affirm would also generate $551 million in NOPAT in fiscal 2031, when the company hasn’t even recorded a single year or quarter with a positive NOPAT.

There’s 79%+ Downside if Margins Capped by Competition

Lastly, if we assume Affirm:

- immediately improves NOPAT margin to 4% (Block’s highest ever margin) through fiscal 2031,

- grows revenue at consensus rates in fiscal 2024, 2025, and 2026, and

- grows revenue 20% in each year thereafter through fiscal 2031, then

the stock would be worth just $4/share today – an 79% downside to the current price. This scenario still implies that Affirm generates $7.2 billion in revenue (over 4.5x TTM revenue) and $288 million in NOPAT (compared to -$1.1 billion in fiscal 2023) in fiscal 2031.

Figure 7 compares Affirm’s implied future NOPAT in these scenarios to its historical NOPAT. We also include the TTM NOPAT for Shopify (SHOP) and Block (SQ) for reference.

Figure 7: Affirm’s Historical and Implied NOPAT: DCF Valuation Scenarios

Sources: New Constructs, LLC and company filings

Stock is Still Not Worth $1

Each of the above scenarios assume Affirm grows revenue, NOPAT, and FCF without increasing working capital or fixed assets. This assumption is highly unlikely but allows us to create best-case scenarios that demonstrate the high level of expectations embedded in the current valuation. For reference, Affirm’s invested capital has grown 43% compounded annually since fiscal 2019. If we assume Affirm’s invested capital increases at a similar rate in the DCF scenarios above, the downside risk is even larger.

Given that the performance required to justify its current price is overly optimistic, we dig deeper to see if Affirm is worth buying at any price. The answer is no.

The company owes $52 million in total debt, has $229 million in outstanding employee stock option liabilities, and has no excess cash. Affirm has an economic book value, or no growth value, of -$28/share. In other words we do not think equity investors will ever see $1 of economic earnings under normal operations, which means the stock would be worth $0 today.

This article was originally published on October 2, 2023.

Disclosure: David Trainer, Kyle Guske II, Italo Mendonça, and Hakan Salt receive no compensation to write about any specific stock, sector, style, or theme.

Questions on this report or others? Join our Society of Intelligent Investors and connect with us directly.