Instead of our usual weekly sell/short call, we are going to open 2015 with two of our favorite stocks for the upcoming year. These stocks have strong growth potential in the coming year, and are attractively valued, trading below their economic book values.

Investors who aren’t paying attention to our Danger Zone reports are in the Danger Zone this week. As 2014 comes to a close, we’d like to highlight a few of the many examples in which our weekly Danger Zone stock reports saved investors from serious price declines.

The Berkshire Focus Fund (BFOCX) is in the Danger Zone this week due to its poor holdings. Looking into this mutual fund’s holdings reveals a number of stocks with the potential to blow up, including some companies recently placed in the Danger Zone themselves.

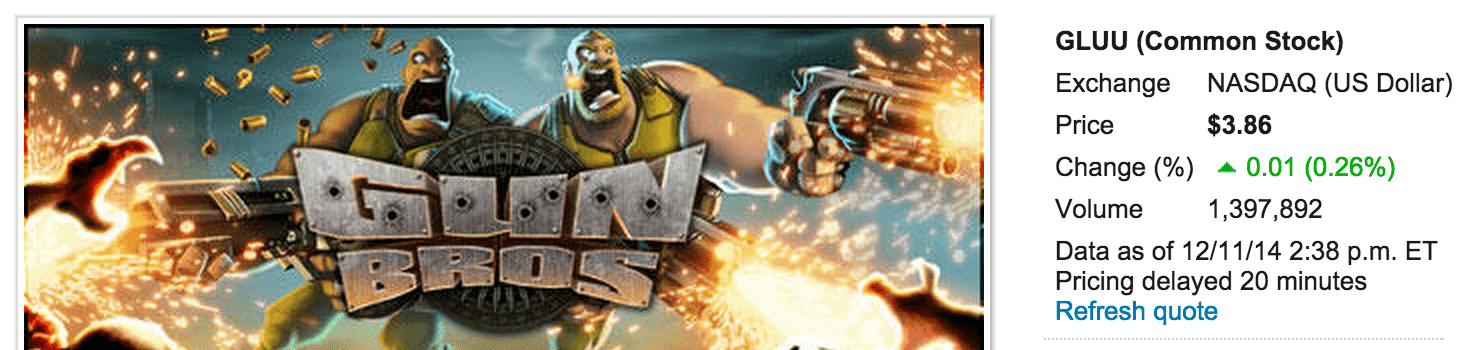

New Constructs’ patented system for reversing accounting distortions performs the due diligence for you on over 3000 stocks, so that you can avoid pitfalls in the headlines like GLUU.

In the past, generating profit growth was not a problem for VeriFone. However, new technologies in the marketplace put VeriFone’s outsized profitability to an end in 2013.

The Barnes Group is in the Danger Zone this week. The Barnes Group’s financial performance has been mediocre at best, but exposure to the global economic slowdown means the stock is too risky for investors to hold or buy. Listen to David Trainer discuss our Danger Zone pick within with Chuck Jaffe of Money Life and MarketWatch.com.

Revlon (REV) is the Danger Zone this week. This makeup company has been fading fast since 2010. Expensive acquisitions and a marketing reboot have boosted the top line while destroying cash flow.

Salesforce.com is a company that has grown rapidly in recent years. While some view their revenue growth as a good sign for investors, others are concerned about the company's mounting losses and falling cash flows. In this report, David Trainer and André Rouillard delve deeper into the financials of Salesforce.com and uncover some concerning trends that investors need to be aware of. From unprofitable acquisitions to hidden debt and liabilities, this report paints a different picture of Salesforce.com than the one many investors are used to. Read on to find out why the authors believe this stock could be headed for a fall.

Oxford Industries (OXM: $62/share) is in the Danger Zone this week.

Oxford is a clothing retailer that sells clothing under the Lilly Pulitzer, Tommy Bahama, and Ben Sherman brands. Over the

Universal Technical Institute (UTI: $10/share), already down 30% in 2014, is likely to drop another 50% as investors factor in its unreasonably high valuation, steadily declining enrollment and how often for-profit education is not profitable for its customers and industry.

While MarineMax's stock suffered along with the company’s earnings during the financial crisis, it rebounded far too high on the back of overstated earnings. The only thing growing as fast as the artificially inflated earnings is the company’s debt.

While this stock has been much-hyped by the Motley Fool, Sierra Wireless has been unable to grow profits or earn positive returns on capital over any meaningful amount of time and the stock’s valuation already reflects alarmingly high expectations for future profit growth.