We closed this position on August 18, 2021. A copy of the associated Position Update report is here.

Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

Our IPO research aims to provide investors with more reliable fundamental research to evaluate upcoming IPOs.

At the midpoint ($9.7 billion) of its expected IPO price range, Compass’ (COMP: $9.7 billion valuation at midpoint of IPO price range) valuation implies it will disrupt the real estate business and generate 2x the revenue of the current largest U.S. brokerage, Realogy. Currently, the company looks more like a traditional brokerage with flashy marketing, whose only advantage is a virtually unlimited ability to burn cash. At the expected IPO valuation, the stock earns our Unattractive rating and is this week’s Danger Zone pick. SoftBank needs this IPO more than investors do.

Compass fails to generate any profits, and with minimal ability to cut costs (and remain competitive), it’s hard to make a straight-faced argument that the firm can justify a ~$10 billion valuation given its:

- “technological advances” are already standard in other real estate businesses

- competition has greater scale and is much more profitable

- valuation implies Compass will generate 2x the revenue of the current largest U.S. brokerage, Realogy, while significantly improving margins (achievements that rarely occur simultaneously)

Is Compass Really a Tech Firm?

Compass advertises its business as an “integrated software platform that helps agents operate with the sophisticated capabilities of a modern technology company…” based on these offerings:

- customer relationship management platform, driven by AI

- client prospecting recommendations, driven by AI

- marketing center to create digital ads, videos, listing presentations, newsletters and more

- virtual tours

- home valuation analysis, powered by AI

- digital ad campaigns and email marketing

Clearly, these “technologies” are not unique. They’re offered at many other firms. For instance, Keller Williams provides agents with its cloud-based Command, an AI driven platform that helps agents automate tasks and drive insights from Keller Williams’ existing consumer and sales data. Realogy (RLGY) offers agents the Realogy Productivity Hub, which provides CRM, transaction management, lead management, marketing, and more. Many other firms regularly use AI and data analytics to value and purchase homes to flip for quick profits.

As one New York real estate executive told Marker “they’re [Compass] a disruptor by capital, not innovation….They’re a brokerage that doesn’t offer anything different; they’re just better at selling an idea.”

Paying for Market Share Isn’t Sustainable

Without differentiated offerings, Compass’ success is largely due to access to large amounts of capital from SoftBank that allows it to burn more cash than its competitors. And, the firm has used this capital to buy, not earn, market share.

For example, as reported in The Wall Street Journal, Compass used generous incentives to attract agents, such as taking no cut of commissions on an agent’s first eight deals and fronting money for staging and cosmetic work. These practices can produce quick market share wins, but they are not sustainable. As one agent put it, “how are you going to turn a profit if you’ve given them (agents) almost all of their commission?”

Not surprisingly, Compass’ business practices haven’t led to any profits yet.

Can We Trust the Financials?

Investors should take Compass’ reported financial results with a grain of salt because the firm’s management notes a material weakness in internal controls over financial reporting. Specifically, the firm disclosed that it:

- “did not maintain formal accounting policies and procedures, and

- did not design, document, and maintain controls related to substantially all of our business processes to achieve complete, accurate and timely financing accounting.

- did not design and maintain effective controls over information technology, general controls or information systems and applications that are relevant to the preparation of the consolidated financial statements.”

The SEC does not require Compass to have an independent auditor provide an opinion on internal controls until its second annual filing following its IPO, so we’re glad the firm chose to disclose this information. However, the firm notes that it:

- “cannot assure the measures we have to date, and actions we may take in the future, will be sufficient to remediate the control deficiencies that led to our material weakness in our internal controls over financial reporting or that they will prevent or avoid potential future material weaknesses.”

What else is there to say? The risk that the firm’s financials are fraudulent and/or misleading is material.

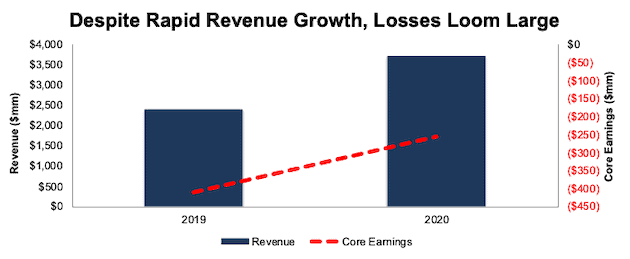

Revenue Growth Is Disruptor-Like…And So Are Losses

With a nearly two trillion-dollar total addressable market (existing U.S. home sales) and revenue growth of 56% year-over-year (YoY) in 2020, Compass fits the traditional tech-stock growth story. However, as with most recent IPOs, Compass loses lots of money. Core Earnings[1] remain negative though they improved from -$411 million in 2019 to -$253 million in 2020.

The firm’s Core Earnings margin improved from -17% in 2019 to -7% in 2020 while its return on invested capital (ROIC) improved from -28% to -18% over the same time.

Figure 1: Compass’ Revenue & Core Earnings: 2019-2020

Sources: New Constructs, LLC and company filings

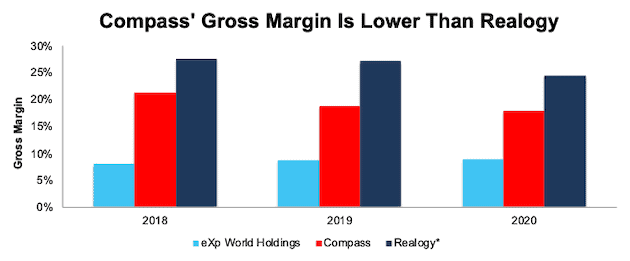

Cost Structure Is Clearly Brokerage-Like

Compass’ “technology” platform has not resulted in any cost savings that result in superior margins.

Per Figure 2, Compass’ gross margin (revenue minus commissions as percent of revenue) fell from 21% in 2018 to 18% in 2020 and ranks below the largest brokerage in the industry, Realogy.

eXp World Holdings (EXPI), a “cloud-based” brokerage (no offices, operates over the internet) had gross margins of 9% in 2020 and could be a better comparison for Compass’ future margins. eXp notes in its 10-K that it “offers agents and brokers a higher split of commissions generated from transactions than most traditional brokerages”, which negatively impacts its gross margin. As long as Compass is in the business of competing for agents, its gross margins will suffer relative to the competition.

Without complimentary business lines, such as franchise fees or title services, Compass must bring on more agents to maintain its rapid revenue growth. To date, the primary way it has attracted more agents is through more lucrative commissions splits. It’s hard to see how the firm will improve its gross margin as long as it is trying to grow.

Figure 2: Gross Margin: Compass vs. eXp and Realogy: 2018-2020

Sources: New Constructs, LLC and company filings

*Realogy’s gross margin calculated as a percentage of commission income, not total revenue, which includes service and franchise fees.

Catch-22: Lose Money or Lose Market Share

We think part of the reason SoftBank wants to sell Compass is that the company now finds itself in a catch-22:

- turn a profit (by cutting agent incentives) and lose market share

Or - grow market share and never turn a profit

We do not believe the firm can continue to grow market share and achieve profitability. We think this business concept has run its course. There’s not a good argument for how the business improves from here. So, SoftBank is hoping to sell now at a higher price before the rest of the market catches on.

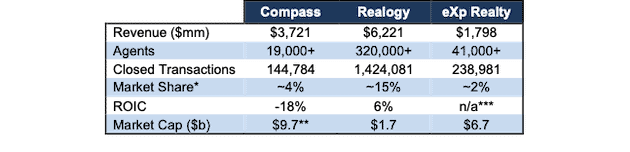

Compass Lacks Scale Against Main Competition

Compass notes in its S-1 that it is the largest “independent” (not owned by a larger brokerage group) real estate brokerage by gross transaction value (GTV) with ~4% of the U.S. home sale total addressable market (TAM)[2]. However, Realogy is the largest real estate brokerage group and holds ~15% of the U.S. home sale TAM while eXp holds ~2%.

Measuring market share using GTV, which represents the total dollar value of homes sold, aids Compass’ growth story as GTV is directly impacted by average home sales price. With an average sale price over $1 million in 2020, Compass maintains a higher GTV with less transactions than a firm with a lower sales price but more transactions, such as eXp. For reference, eXp’s average sales price was just over $302,000.

If, instead of GTV, we look at total transactions, we see that eXp closed nearly 239,000 transactions in 2020 compared to Compass’ ~145,000. Realogy group closed more than 1.4 million transactions between its franchise and brokerage businesses in 2020. Going forward, Compass may find it more difficult to grow GTV at such a rapid pace without even faster growth in total transactions as it expands beyond its initial and unusually higher priced markets of New York, Los Angeles, the Hamptons, or San Francisco.

Market share calculations aside, Compass also generates less revenue than Realogy and employs less agents than both Realogy and eXp. Most importantly, Realogy generates a return on invested capital (ROIC) that is significantly higher than Compass. However, investors have clearly bought into Compass’ (and eXp’s) “tech-story”, as Compass’ valuation is nearly 6x higher than Realogy. Figure 3 illustrates the excessive optimism baked into its valuation.

Figure 3: Compass vs. Realogy – Disconnect in Scale vs. Valuation

Sources: New Constructs, LLC and company filings

*Market share calculated as transaction volume (reported by Real Trends) divided by two times (to account for the sell-side and buy-side of each transaction) the aggregate dollar value of U.S. existing home sales reported by NAR.

**Based on midpoint of IPO price range

***eXp is not under coverage so we have not calculated its ROIC.

Profitability Lags Non-Traditional Peers Too

Competition doesn’t stop with just Realogy either, as Compass competes with the likes of Keller Williams, Re/Max, Berkshire Hathaway HomeServices, the rest of the estimated 86,000 brokerages and internet centric firms such as eXp World Holdings, Redfin (RDFN), Zillow Group (ZG), and another Softbank-backed competitor Opendoor (OPEN).

Per Figure 4, Compass’ net operating profit after-tax (NOPAT) margin ranks below each of its main competitors. Its invested capital turns, a measure of balance sheet efficiency, are much higher than all three in the group, which is noteworthy. However, capital efficiency is not enough to offset poor operational efficiency, as Compass’ ROIC ranks last among its competition.

Negative profitability and limited room to cut expenses means, barring an unforeseen change in its business model, Compass is unlikely to best peers.

Figure 4: Fundamental Profitability Metrics: Compass vs. Competitors: TTM

Sources: New Constructs, LLC and company filings

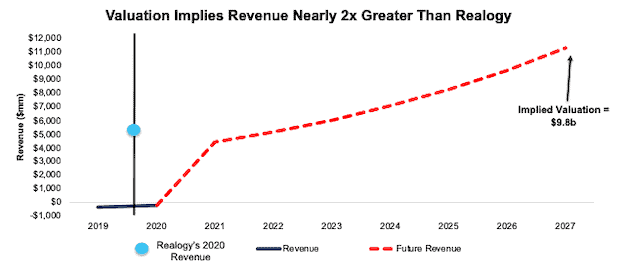

Appraising Compass’ Valuation

To start, Compass’ economic book value, or no growth value, is -$15/share, which further illustrates the excessive optimism baked into its expected IPO valuation.

Our reverse discounted cash flow (DCF) model shows that COMP’s expected IPO valuation implies the company will triple its current market share and generate almost 2x the revenue of the current largest U.S. brokerage, Realogy.

IPO Priced for Perfect Execution

Investors looking to buy Compass at its expected IPO valuation are betting Compass is able to maintain double-digit revenue growth while also improving margins (two things that rarely occur simultaneously).

Specifically, to justify its expected IPO valuation, Compass must:

- immediately improve its NOPAT margin to 5%, which is well above its current -6% and slightly below Realogy’s 7% margin, which benefits from higher margin franchise and title/services segments, and

- grow revenue by 17% compounded annually for the next seven years, which is nearly double Realogy’s consensus estimate revenue CAGR from 2020-2022 (9%)

See the math behind this reverse DCF scenario. In this scenario, Compass’ implied revenue in 2027 is $11.3 billion, or nearly two times Realogy’s 2020 revenue. Its implied GTV would be $461 billion[3], which equates to ~12% of the 2020 U.S. home sale TAM[4]. For reference, Realogy, the largest U.S. brokerage group, held 15% of the home sale TAM in 2020. We think such a scenario is unlikely, given Compass’ limited ability to cut costs and grow market share at the same time.

Figure 5 compares the firm’s historical revenue to its implied revenue in this scenario.

Figure 5: Historical Revenue vs. DCF Implied Revenue

Sources: New Constructs, LLC and company filings

Compass’ market share in this scenario would remain below Realogy’s despite nearly double the revenue due to Realogy’s franchise operations. Franchises contribute to Realogy’s GTV, which increases its market share. However, the royalty fees franchises pay to Realogy as revenue are less than the revenue Realogy would generate from each home sale at one its company owned brokerages. Accordingly, Realogy is able to grow its market share as measured by GTV without a commensurate increase in its overall revenue.

44% (Or More) Downside Risk if Compass Is Not Perfect

If Compass’ disruptor “tech story” fails to fully materialize, the downside risk is huge.

Let’s take a look at the impact of a slightly less optimistic scenario than above on the valuation of COMP. Specifically, if we assume Compass:

- immediately improves its NOPAT margin to 4% (average between Zillow and Realogy) and

- grows revenue by 10% compounded annually for the next decade, which is slightly above Realogy’s consensus estimate revenue CAGR from 2020-2022 (9%), then

the stock is worth just $5.5 billion today – a 44% downside to the firm’s expected IPO valuation. See the math behind this reverse DCF scenario. In this scenario, Compass’ implied GTV would be $393 billion[5], which equates to ~10% of the 2020 U.S. home sale TAM. In other words, even if Compass’ can more than double its current market share, the stock’s value is well below the expected IPO valuation.

Each of the above scenarios also assumes Compass is able to grow revenue, NOPAT, and FCF without increasing working capital or fixed assets. This assumption is highly unlikely but allows us to create best-case scenarios that demonstrate the expectations implied to justify its IPO valuation.

Public Shareholders Have No Rights

A risk of investing in Compass, as with many recent IPOs, is the fact that that the shares sold provide little to no voting power.

Compass is going public with three separate share classes, each with different voting rights. Compass’ IPO listing is for Class A shares, with one vote per share. Class B shares provide no votes per share. Class C shares provide 20 votes per share and are held entirely by Chairman and Chief Executive Officer Robert Reffkin. Other notable Class A holders include Softbank’s Vision Fund and DG Urban-C, which hold ~35% and 9% of Class A shares, respectively.

Compass notes that “the multi-class structure of our common stock will have the effect of concentrating voting power with Robert Reffkin…which will limit your ability to influence the outcome of matters submitted to our stockholders for approval…” After IPO, Robert Reffkin will hold 46% of the total voting power. Softbank’s Vision Fund and DG Urban-C will hold 19% and 5% of the voting power respectively.

Non-GAAP EBITDA Overstates Profitability

Unsurprisingly, Compass’ chosen non-GAAP metric, adjusted EBITDA, shows a much rosier picture of the firm’s operations than GAAP net income. Adjusted EBITDA allows management significant leeway in excluding material costs in its calculation. For example, Compass’ adjusted EBITDA calculation removes stock-based compensation expense, acquisition related expenses, and more.

Compass’ adjusted EBITDA in 2020 removes $115 million (3% of revenue) in expenses including $43 million in stock-based compensation expense. After removing these items, Compass reports adjusted EBITDA of -$156 million in 2020. Meanwhile, economic earnings, the true cash flows of the business, are much lower at -$298 million.

While Compass’ adjusted EBITDA follows the same trend in economic earnings over the past two years, investors need to be aware that there is always a risk that adjusted EBITDA could be used to manipulate earnings going forward.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

Fact: we provide superior fundamental data and earnings models – unrivaled in the world.

Proof: Core Earnings: New Data and Evidence, forthcoming in The Journal of Financial Economics.

Below are specifics on the adjustments we make based on Robo-Analyst findings in Compass’ S-1:

Income Statement: we made $52 million of adjustments, with a net effect of removing $40 million in non-operating expenses (1% of revenue). You can see all the adjustments made to Compass’ income statement here.

Balance Sheet: we made $154 million of adjustments to calculate invested capital with a net increase of $78 million. The most notable adjustment was $36 million in midyear acquisitions. This adjustment represented 3% of reported net assets. You can see all the adjustments made to Compass’ balance sheet here.

Valuation: we made $1.5 billion of adjustments with a net effect of decreasing shareholder value by $1.5 billion. There were no adjustments that increased shareholder value. The largest adjustment to shareholder value was $1 billion in outstanding employee stock options. This adjustment represents 10% the midpoint of Compass’ IPO price range. See all adjustments to Compass’ valuation here.

This article originally published on March 29, 2021.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Only Core Earnings enable investors to overcome the inaccuracies, omissions and biases in legacy fundamental data and research, as proven in Core Earnings: New Data & Evidence, a forthcoming paper in The Journal of Financial Economics written by professors at Harvard Business School (HBS) & MIT Sloan.

[2] U.S. home sale TAM defined as two times (to account for the sell-side and buy-side of each transaction) the aggregate dollar value of U.S. existing home sales as reported by the National Association of Realtors (NAR)

[3] Calculated by taking the implied revenue in 2027 and dividing by Compass’ 2020 revenue as a percent of 2020 GTV, which equaled 2.5%.

[4] Implied share of 2020 home sale TAM calculated by taking implied GTV divided by two times (to account for the sell-side and buy-side of each transaction) the aggregate dollar value of U.S. existing home sales as reported by NAR.

[5] Calculated by taking the implied revenue in 2030 and dividing by Compass’ 2020 revenue as a percent of 2020 GTV, which equaled 2.5%.