Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

In theory, share buybacks are an efficient mechanism for companies to return cash to shareholders when they believe the stock is undervalued and have more cash than profitable investment opportunities.

In practice, companies often buyback shares when their stock is at the highest point, and they sometimes pass up profitable investments or even go into debt to do the buybacks. The timing of buybacks can also be influenced more by when executives exercise their stock options than fundamental opportunity.

The issue comes primarily from the poor executive compensation practices in place throughout most of corporate America. Executives are consistently incentivized to hit targets related to non-GAAP EPS and other metrics that are easily manipulated and have little connection to long-term shareholder value.

There’s a much better way to incentivize the right kind of behavior from executives. Return on invested capital (ROIC) has a proven link to shareholder value[1] and cannot be manipulated or gamed in the same way. That’s why we’ve created a specific model portfolio of companies that link executive compensation to ROIC.

Relatively few companies tie executive compensation to ROIC. Here’s why:

- ROIC is difficult to accurately calculate in way that is comparable across companies, so few shareholders can use it reliably.

- ROIC targets are much more difficult to hit than other, easily manipulated metrics. Executives would rather have the malleable non-GAAP EPS performance targets because they can always fudge the numbers or buyback a bunch of shares towards the end of the year if it looks like they’re going to come up short.

- Compensation committees, which should be holding executives to a higher standard, often lack the independence, expertise, or engagement necessary to protect shareholder’s interests. They’re too often willing to go along with whatever top executives suggest.

Barring a drastic overhaul in corporate pay practices, companies will continue to destroy value via share buyback. Below, we present examples of good and bad buyback programs, and how executive compensation practices have impacted each.

Example of A Bad Buyback: CBS Corp (CBS)

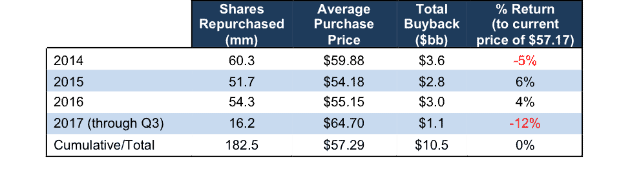

CBS Corp (CBS: $57/share) has been one of the most prolific companies in terms of buying back stock in recent years. As Figure 1 shows, the broadcaster has bought back 183 million shares (over 30% of the company) since 2014. The table also shows that all these buybacks have delivered meager gains to shareholders.

Figure 1: CBS Share Buybacks Since 2014

Sources: New Constructs, LLC and company filings.

The company has strongly signaled that buying back shares is now its primary aim. “Capital returns will continue to be our focus and our top priority going forward,” COO Joseph R. Ianniello told investors in the company’s 1Q14 conference call.

With capital return being a top priority, one would think CBS would at least buyback shares efficiently. Figure 1 shows that is not the case. Instead, the company has bought back a higher volume of shares when the stock is more expensive and bought back fewer when the stock is cheap (as it was in 2015).

Opportunity Cost of the Buyback

CBS has earned an average ROIC of just 5% over the past three years. However, that still handily beats out the 0% gain the company has earned on the 183 million shares it’s bought since 2014. Moreover, CBS’ ROIC had grown in four consecutive years prior to it ramping up its buyback program in 2014.

It would be one thing if there were no investment opportunities available in the broadcasting/publishing fields in which CBS operates, but we know that’s not true. CBS could be investing more heavily in new content or live sports rights to drive immediate profitability. Long-term, it could take strategic steps such as building out a bigger streaming platform.

Since the beginning of 2014, CBS has decreased its invested capital from $44.6 billion to $38.7 billion. Compare this divestment with Walt Disney (DIS), which has increased its invested capital from $73.2 billion to $86.9 billion going back to 2014, while improving ROIC from 10% to 11.4%. Disney has also engaged in limited share buybacks, but buybacks have not stopped it from investing in profitable growth opportunities.

Overall, the companies that CBS lists as its peer group[2] have increased their invested capital by 9% since the start of 2014. On a cap-weighted basis, these stocks are up an average of 27% since that date, while CBS has fallen by 9%.

Compensation Plan Misaligns Executives’ Incentives

Part of the issue for CBS and its shareholders is that the company’s executive compensation practices have incentivized the wrong sort of behavior. We can see several examples:

- Short-term bonuses are determined in part by Adjusted EPS, which the company can boost through buybacks that decrease the total share count

- The company directly rewards executives for buying back shares

- Part of long-term awards are tied to free cash flow, which in theory can be a good metric to target, but in practice for CBS has led to decreased investment (and even divestiture) to keep free cash flow higher

- CBS executives have timed the heaviest buybacks around the execution of their stock options. The company bought back the most stock in 2014 when its executives executed 10.6 million options. Meanwhile both buybacks and option executes decreased in 2015 and 2016.

Compare CBS’ compensation practices to Disney’s, where the company links a significant portion of annual bonuses to ROIC targets. Disney’s compensation structure incentivizes executives to look for ROIC-enhancing investment opportunities rather than just plowing all available cash into buybacks.

Positive Example: Lear Corp (LEA)

Lear Corp (LEA) began buying back shares heavily in 2013, when the stock was trading in the mid-50’s per share. Since the start of 2013, Lear has retired over 30 million shares (39% of outstanding shares) with a net spend of $2.9 billion at an average price of $90.74/share. With the stock at $174/share today, Lear has earned a roughly 92% return on its investment in its own shares.

Buybacks have not stopped Lear from investing in its business either. Since the start of 2013 Lear has increased its invested capital by over 70%, from $4.2 billion to $7.2 billion while maintaining an ROIC well above industry-average.

Lear’s strong ROIC and disciplined buyback strategy makes sense, as 2/3 of long-term executive bonuses are tied to ROIC. By incentivizing efficient capital allocation, the board ensures that executives invest in profitable business opportunities where available and return capital to investors when shares trade at a discount.

The combination of buying back shares and profitable investment has helped Lear increase its stock price by 275% since the start of 2013.

Current Buyback Red Flag: T-Mobile (TMUS)

Wireless carrier T-Mobile (TMUS) recently announced its first ever buyback program, a $1.5 billion authorization that accounts for 8% of open market shares at the current price (64% of TMUS is held by Deutsche Telecom). The announcement came after the collapse of merger talks with rival Sprint (S).

The buyback plan comes at a bad time, as TMUS has had no shortage of profitable investment opportunities in recent years. Since 2014, the company has increased its invested capital by 25% while improving its ROIC from 2% to 5%. Over the past twelve months, TMUS has generated positive economic earnings for the first time since 2013.

Despite its improvement in profitability, TMUS does not have a great deal of cash to spend on buybacks. Since 2014, its free cash flow is negative $12 billion. The company currently has over $40 billion in debt (including $9.5 billion in off-balance sheet debt). Spending money on buybacks will further leverage the company and undermine its ability to invest in value-creating growth opportunities.

In order to achieve long-term profitability, TMUS needs to invest more. The telecom industry is fundamentally about scale. The four largest (by revenue) telecom companies under coverage – AT&T (T), Verizon (VZ), China Mobile (CHL), and Nippon Telegraph and Telephone (NTTYY) – earned more than $30 billion in economic earnings over the past twelve months. The remaining 40 companies recorded cumulative economic losses of $6.7 billion.

The Sprint merger was T-Mobile’s effort to gain the scale necessary to profitably compete with AT&T and Verizon. Without that merger, T-Mobile will need a significant amount of new investment to keep up with industry leaders. It can’t afford to spend money it doesn’t have on buybacks.

On top of the strategic problems, TMUS is buying back shares at an expensive valuation. In order to justify its current price of ~$63/share, the company must maintain 2016 margins and grow NOPAT by 10% compounded annually for the next eight years.

TMUS seems to be falling prey to the overvaluation trap. The company plans to buy back shares to prop up an inflated valuation rather than invest in the growth opportunities it needs to create value and justify its valuation.

Unsurprisingly, TMUS does not link executive compensation to ROIC. Instead, a significant portion of executives’ restricted share units are tied to total shareholder return from 2016 to 2019, while annual bonuses are tied to metrics such as adjusted EBITDA and free cash flow. TMUS executives are incentivized to buy back stock to prop up the price for the next couple years rather than make the long-term investments that could hurt their annual metrics.

Current Buyback That Could Create Value: Walmart (WMT)

On the positive side, Walmart (WMT) recently announced a $20 billion buyback (7% of market cap) to take place over the next two years. WMT links 50% of long-term executive bonuses to ROIC, so we have faith in the company’s capital allocation decisions.

In addition to a track record of responsible capital allocation, WMT has ample resources to fund its buyback. The company generated $20 billion in free cash flow in 2017, and it has generated at least $10 billion in free cash flow for each of the past five years. WMT can easily fund its buyback program while still making the investments necessary to continue the impressive growth of its e-commerce efforts.

WMT also has an attractive valuation. At its current price of ~$97/share, WMT has a price to economic book value (PEBV) ratio of 1.0. That valuation implies that the market expects WMT to never grow NOPAT above its current level. WMT is smart to take advantage of this opportunity to retire a significant portion of its outstanding shares at a cheap price.

With plenty of resources, a cheap stock, and the mechanisms in place to ensure management is incentivized to be responsible stewards of shareholder capital, we like the odds for WMT’s buyback to create value for its investors.

This article originally published on December 18, 2017.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Ernst & Young’s recent white paper, “Getting ROIC Right”, proves the superiority of our research and analytics.

[2] Discover Communications (DISCA), Time Warner (TWX), Twenty-First Century Fox (FOXA), Viacom (VIAB), Disney (DIS) and Comcast (CMSCA) per CBS’s most recent proxy statement.