This report is one of a series on the adjustments we make to GAAP data so we can measure shareholder value accurately. This report focuses on an adjustment we make to our calculation of economic book value and our discounted cash flow model.

We’ve already broken down the adjustments we make to NOPAT and invested capital. Many of the adjustments in this third and final section deal with how adjustments to those two metrics affect how we calculate the present value of future cash flows. Some adjustments represent senior claims to equity holders that reduce shareholder value while others are assets that we expect to be accretive to shareholder value.

Adjusting GAAP data to measure shareholder value should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

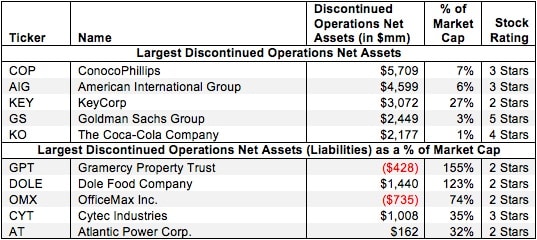

In earlier reports, we discussed how discontinued operations inflate operating profit (NOPAT) and balance sheets. There is one last adjustment we must make involving discontinued operations: adding net assets from discontinued operations to shareholder value. Because discontinued operations are parts of a company being held for sale, the value of the net assets from these discontinued operations approximate the cash the company will receive from the sale. This cash will then be available for distribution to shareholders.

You can find our aforementioned report on discontinued operations removed from operating profit here, and our report on discontinued operations removed from invested capital here.