13 new stocks made our Most Attractive list this month, while 11 new stocks joined the Most Dangerous list. We published November’s Most Attractive and Most Dangerous stocks to members on November 2, 2023.

October Performance Recap

Our Most Attractive Stocks (+1.7%) outperformed the S&P 500 (-1.6%) last month by 3.3%. The best performing large cap stock gained 28% and the best performing small cap stock was up 32%. Overall, 25 out of the 40 Most Attractive stocks outperformed the S&P 500.

Our Most Dangerous Stocks (-6.6%) outperformed the S&P 500 (-1.6%) as a short portfolio last month by 5.0%. The best performing large cap short stock fell by 23% and the best performing small cap short stock fell by 21%. Overall, 24 out of the 33 Most Dangerous stocks outperformed the S&P 500 as shorts.

The Most Attractive/Most Dangerous Model Portfolios outperformed as an equal-weighted long/short portfolio by 8.3%.

This report leverages our cutting-edge Robo-Analyst technology to deliver proven-superior[1] fundamental research and support more cost-effective fulfillment of the fiduciary duty of care.

All of our Most Attractive stocks have high (and rising) return on invested capital (ROIC) and low price to economic book value ratio. Most Dangerous stocks have misleading earnings and long growth appreciation periods implied by their market valuations.

Most Attractive Stocks Feature for November: Toll Brothers Inc. (TOL)

Toll Brothers (TOL: $80/share) is the featured stock from November’s Most Attractive Stocks Model Portfolio.

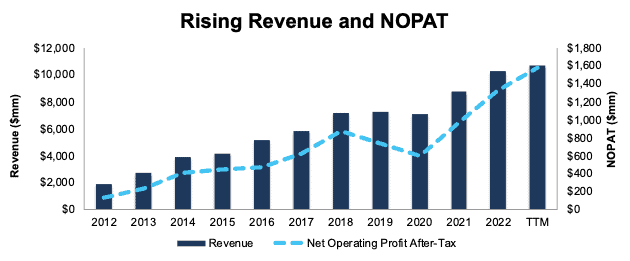

Toll Brothers has grown revenue by 18% compounded annually and net operating profit after tax (NOPAT) by 26% compounded annually since fiscal 2012. Toll Brothers’ NOPAT margin increased from 7% in fiscal 2012 to 15% in the trailing twelve months (TTM), and invested capital turns rose from 0.4 to 0.9 over the same time. Rising NOPAT margins and invested capital turns drive Toll Brothers’ return on invested capital (ROIC) from 2% in fiscal 2012 to 13% in the TTM.

Figure 1: Toll Brothers’ Revenue and NOPAT Since Fiscal 2012

Sources: New Constructs, LLC and company filings

Toll Brothers Is Undervalued

At its current price of $80/share, TOL has a price-to-economic book value (PEBV) ratio of 0.5. This ratio means the market expects Toll Brothers’ NOPAT to permanently decline by 50%. This expectation seems overly pessimistic for a company that has grown NOPAT by 26% compounded annually since fiscal 2012 and 12% compounded annually since fiscal 1998.

Even if Toll Brothers’ NOPAT margin falls to 10% (equal to its ten-year average compared to 15% over the TTM) and the company’s revenue grows just 4% (compared to five-year average of 12%) compounded annually through 2032, the stock would be worth $111/share today – a 39% upside. Should Toll Brothers grow profits more in line with historical levels, the stock has even more upside.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

Below are specifics on the adjustments we made based on Robo-Analyst findings in Toll Brothers’ 10-Qs and 10-Ks:

Income Statement: we made $367 million in adjustments, with a net effect of removing $1 million in non-operating income (<1% of revenue). Clients can see all adjustments made to Toll Brothers’ income statement on the GAAP Reconciliation tab on the Ratings page on our website.

Balance Sheet: we made $4.3 billion in adjustments to calculate invested capital with a net increase of $1.7 billion. One of the most notable adjustments was $1.7 billion in adjustments for asset write downs. This adjustment represents 21% of reported net assets. Clients can see all adjustments made to Toll Brothers’ balance sheet on the GAAP Reconciliation tab on the Ratings page on our website.

Valuation: we made $5.0 billion in adjustments, with a net decrease in shareholder value of $4.0 billion. The most notable adjustment was $4.1 billion in total debt. This adjustment represents 48% of Toll Brothers’ market value. Clients can see all adjustments to Toll Brothers’ valuation on the GAAP Reconciliation tab on the Ratings page on our website.

Most Dangerous Stocks Feature: Dril-Quip Inc. (DRQ)

Dril-Quip (DRQ: $22/share) is the featured stock from November’s Most Dangerous Stocks Model Portfolio.

Dril-Quip’s NOPAT has fallen from $127 million in 2012 to -$81 million over the TTM. The company’s NOPAT margin has fallen from 17% in 2012 to -21% in the TTM, while invested capital turns fell from 0.9 to 0.4 over the same time. Falling NOPAT margins and invested capital turns drive Dril-Quip’s ROIC from 16% in 2012 to -8% over the TTM.

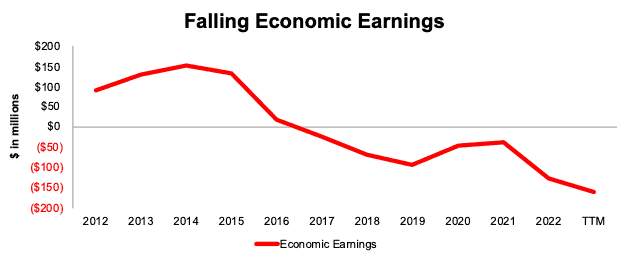

Dril-Quip’s economic earnings, the true cash flows of the business which take into account changes to the balance sheet, have fallen from $90 million in 2012 to -$161 million over the TTM.

Figure 2: Dril-Quip’s Economic Earnings Since 2012

Sources: New Constructs, LLC and company filings

DRQ Provides Poor Risk/Reward

Despite its poor fundamentals, Dril-Quip’s stock is priced for significant profit growth, and we believe the stock is overvalued.

To justify its current price of $22/share, Dril-Quip must improve its NOPAT margin to 6% (up from -21% over the TTM) and grow revenue by 11% compounded annually through 2032. In this scenario, Dril-Quip’s NOPAT would equal $62 million in 2032, up from its TTM NOPAT of -$81 million. We think these expectations are overly optimistic. For reference, Dril-Quip hasn’t generated a margin as high as 6% since 2017.

Even if Dril-Quip improves its NOPAT margin to 3% and grows revenue 8% compounded annually through 2032, the stock would be worth no more than $10/share today – a 55% downside to the current stock price.

Each of these scenarios also assumes Dril-Quip can grow revenue, NOPAT, and FCF without increasing working capital or fixed assets. This assumption is unlikely but allows us to create best case scenarios that demonstrate the high expectations embedded in the current valuation.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

Below are specifics on the adjustments we made based on Robo-Analyst findings in Dril-Quip’s 10-Qs and 10-K:

Income Statement: we made $102 million in adjustments, with a net effect of removing $60 million in non-operating income (15% of revenue). Clients can see all adjustments made to Dril-Quip’s income statement on the GAAP Reconciliation tab on the Ratings page on our website.

Balance Sheet: we made $578 million in adjustments to calculate invested capital with a net increase of $66 million. One of the most notable adjustments was $169 million in other comprehensive income. This adjustment represented 19% of reported net assets. Clients can see all adjustments made to Dril-Quip’s balance sheet on the GAAP Reconciliation tab on the Ratings page on our website.

Valuation: we made $113 million in adjustments to shareholder value with a net increase of $91 million. The most notable adjustment to shareholder value was $12 million in operating leases. This adjustment represents 2% of Dril-Quip’s market value. Clients can see all adjustments to Dril-Quip’s valuation on the GAAP Reconciliation tab on the Ratings page on our website.

This article was originally published on November 10, 2023.

Disclosure: David Trainer, Kyle Guske II, Hakan Salt, and Italo Mendonça receive no compensation to write about any specific stock, style, or theme.

Questions on this report or others? Join our Society of Intelligent Investors and connect with us directly.

[1] Our research utilizes our Core Earnings, a more reliable measure of profits, as proven in Core Earnings: New Data & Evidence, written by professors at Harvard Business School (HBS) & MIT Sloan and published in The Journal of Financial Economics.

2 replies to "Featured Stocks in November’s Most Attractive/Most Dangerous Model Portfolios"

When T.D. Ameritrade was operating, I used the New Construct accounting to evaluate stocks. After Schwab purchased/merged T.D., we no longer have access to NewContrct. I contacted Schwab with the facts that

I felt that New Construct would be a valuable addition to their list of financial companies evaluating stocks.

Would you please ask your CEO and/or sales team to contact Schwab. Maybe Schwab would purchase your

research.

Thank you

Hello! Appreciate your positive feedback. We’re eager to collaborate with Schwab and have expressed interest before. Your input on the value of New Constructs via TDA is valuable. Let’s hope others share similar sentiments with Schwab. Cheers!