Recap from September’s Picks

Our Most Attractive Stocks (+7.5%) outperformed the S&P 500 +2.6%) last month. Most Attractive Large Cap stock NetApp (NTAP) gained 14%. Most Attractive Small Cap stock Nova Measuring Instruments (NVMI) was up 28%. Overall, 31 out of the 40 Most Attractive stocks outperformed the S&P 500 in September.

Our Most Dangerous Stocks (+7.6%) underperformed the S&P 500 (+2.6%) as a short portfolio last month. Most Dangerous Large Cap stock MGM Resorts International (MGM) fell 10%. Most Dangerous Small Cap stock Trans World Entertainment (TWMC) fell by 18%. Overall, 11 out of the 40 Most Dangerous stocks outperformed the S&P 500 as short positions in September.

The successes of the Most Attractive and Most Dangerous stocks highlight the value of our Robo-Analyst technology, which helps clients fulfill the fiduciary duty of care when making investment recommendations[1].

13 new stocks made this month’s Most Attractive list and 11 new stocks fell onto this month’s Most Dangerous list. October’s Most Attractive and Most Dangerous stocks were made available to members on October 3, 2017.

Our Most Attractive stocks have high and rising returns on invested capital (ROIC) and low price to economic book value ratios. Most Dangerous stocks have misleading earnings and long growth appreciation periods implied by their market valuations.

Most Attractive Stocks Feature for October: Cirrus Logic, Inc. (CRUS, $55/share)

Cirrus Logic (CRUS), a manufacturer of specialized semiconductors, is the featured stock from October’s Most Attractive Stocks.

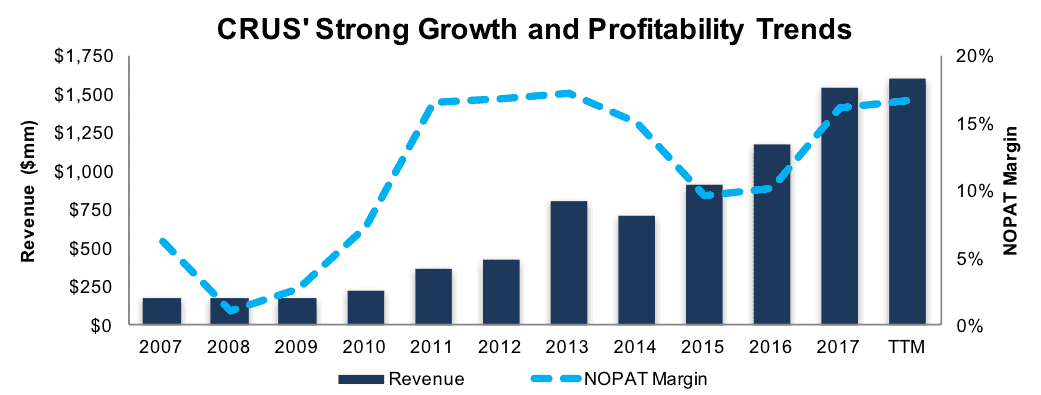

Over the past decade, revenue has grown 24% compounded annually while after-tax profits (NOPAT) have grown 36% compounded annually. Momentum has shown no signs of waning in more recent years. Since year-end 2014, revenue has grown 29% compounded annually while NOPAT has grown 32% compounded annually. Profit margins also continue to improve. CRUS’ NOPAT margin has risen from 6% in 2007 to 17% over the trailing twelve months (TTM). The firm’s current 18% ROIC (TTM) is top-quintile among our coverage universe.

Figure 1: CRUS 10-Year Revenues and NOPAT Margin

Sources: New Constructs, LLC and company filings

Priced for Permanent Profit Decline

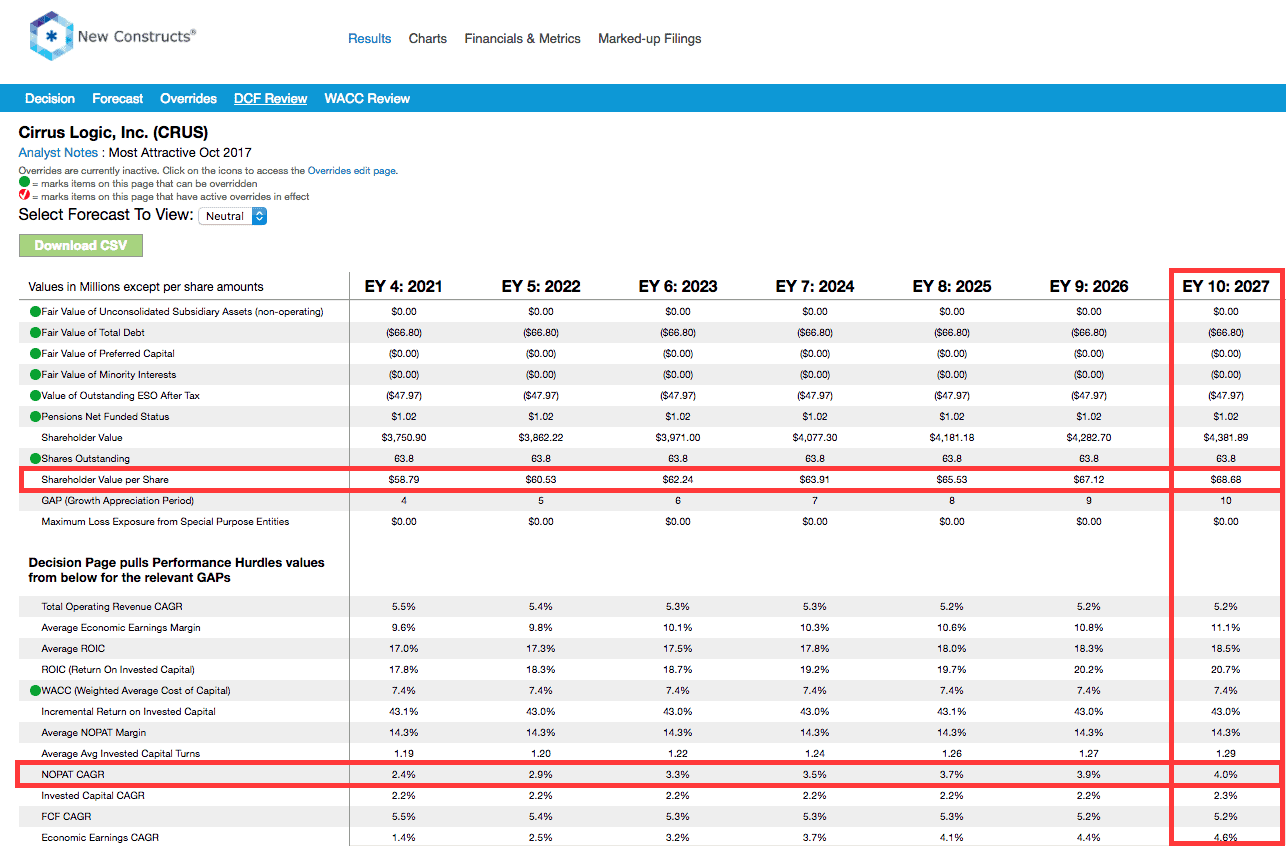

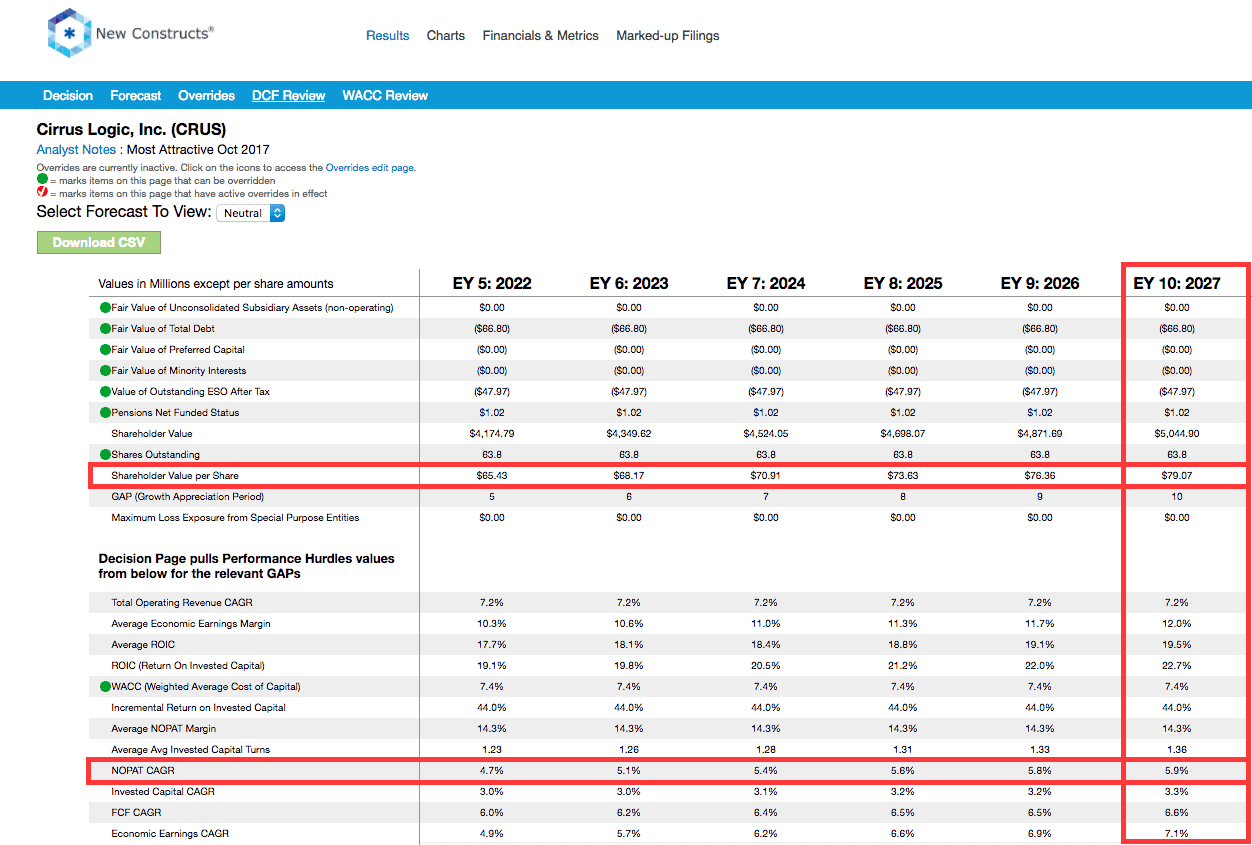

At its current price of $55/share, CRUS has a price-to-economic book value (PEBV) ratio of 0.9. This ratio means the market expects CRUS’ NOPAT to permanently decline by 10% from current levels. This expectation seems overly pessimistic for a firm that has generated 36% compound annual NOPAT growth over the past ten years and has shown no signs of losing momentum.

If CRUS can operate at its five-year average NOPAT margin of 14% (vs. 17% TTM), grow revenue 5% compounded annually, and grow NOPAT by 4% compounded annually over the next decade, the stock is worth $68/share today – a 25% upside. In a more optimistic scenario of 6% compound annual NOPAT growth over the next decade, the stock is worth $79/share today – a 44% upside.

{kind=link}

{kind=link}

Auditable Impact of Footnotes and Forensic Accounting Adjustments[1]

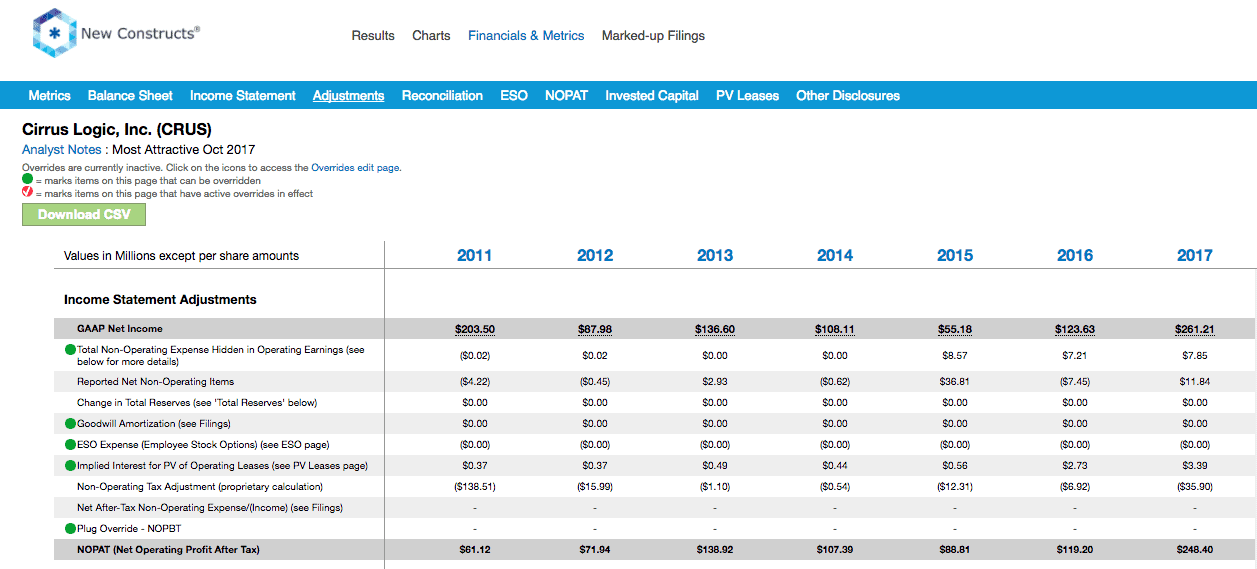

Our Robo-Analyst technology enables us to perform forensic accounting with scale and provide the research needed to fulfill fiduciary duties. In order to derive the true recurring cash flows, an accurate invested capital, and an accurate shareholder value, we made the following adjustments to Cirrus Logic’s (CRUS) 2017 10-K:

Income Statement: we made $85 million of adjustments, with a net effect of removing $13 million in non-operating income (<1% of revenue). We removed $49 million in non-operating income and $36 million in non-operating expenses. You can see all the adjustments made to CRUS’s income statement here.

{kind=link}

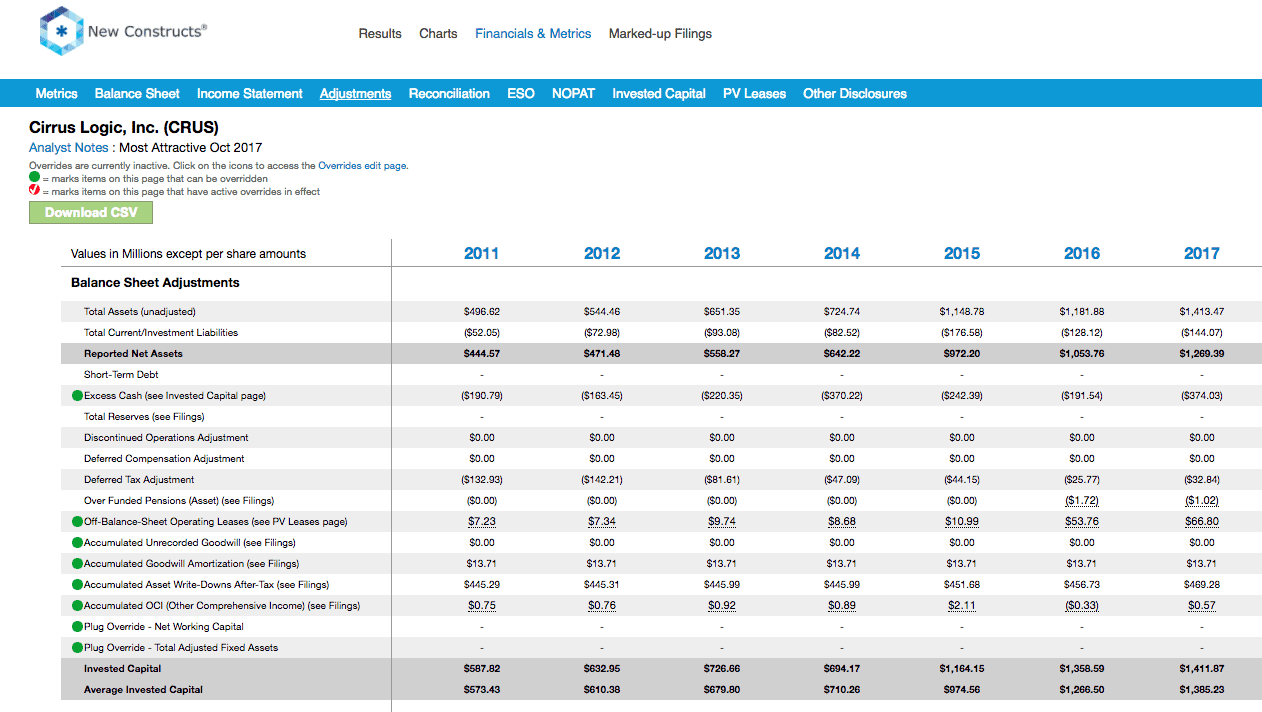

Balance Sheet: we made $986 million of adjustments to calculate invested capital with a net increase of $116 million. One of the largest adjustments was $39 million due to asset write-downs. This adjustment represented 37% of reported net assets. You can see all the adjustments made to CRUS’s balance sheet here.

{kind=link}

Valuation: we made $346 million of adjustments with a net effect of increasing shareholder value by $116 million. The largest adjustment to shareholder value was $67 million in off-balance sheet operating leases. This adjustment represents 2% of CRUS’s market cap.

Most Dangerous Stocks Feature: AstraZeneca PLC (AZN, $35/share)

AstraZeneca PLC (AZN), the 10th largest pharmaceutical firm by market cap, is the featured stock from October’s Most Dangerous Stocks.

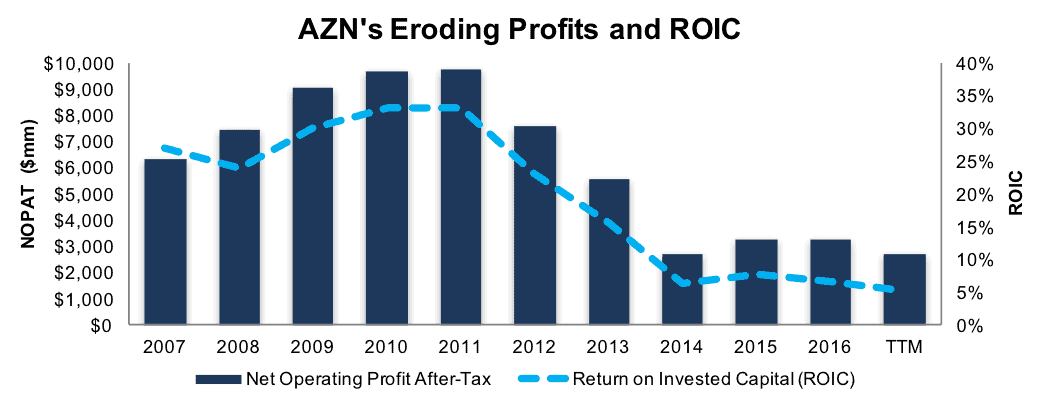

Over the past decade, AZN’s revenues have declined 3% compounded annually while after-tax profits (NOPAT) have declined 9% compounded annually. The impact of shrinking revenues has been magnified by a significant drop in NOPAT margin from 22% in 2007 to 12% TTM. Since year-end 2014, the revenue decline has accelerated to 6% compounded annually. NOPAT has remained flat, however, due to a modest rebound in NOPAT margin from the 10% low in 2014. AZN’s ROIC has declined from 27% in 2007 to 5% TTM.

Figure 2: AZN 10-Year NOPAT and ROIC

Sources: New Constructs, LLC and company filings

AZN Presents Significant Valuation Risk

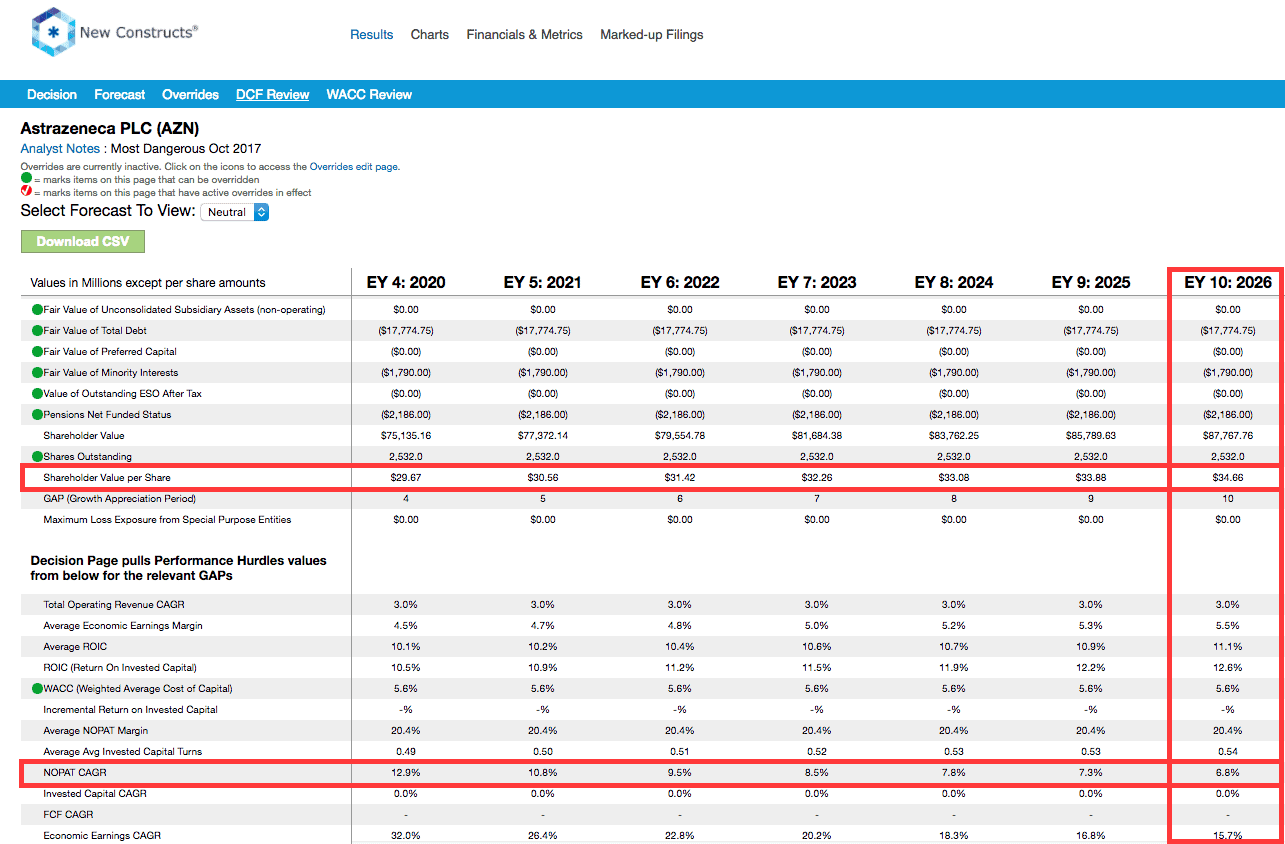

At the end of 2012, AZN’s stock traded at a 0.4 PEBV ratio, which meant the market was (accurately) pricing in a 60% decline in NOPAT. Since that time, AZN’s NOPAT (TTM) is down 64%. However, AZN’s stock price is 46% higher than the end of 2012. AZN now trades at a PEBV ratio of 3.2. This ratio means the market expects AZN’s NOPAT to grow to 320% of current levels, or roughly $8.6 billion vs. $2.7 billion TTM. This level of optimism seems unwarranted in light of AZN’s financial performance over the past decade and TTM period.

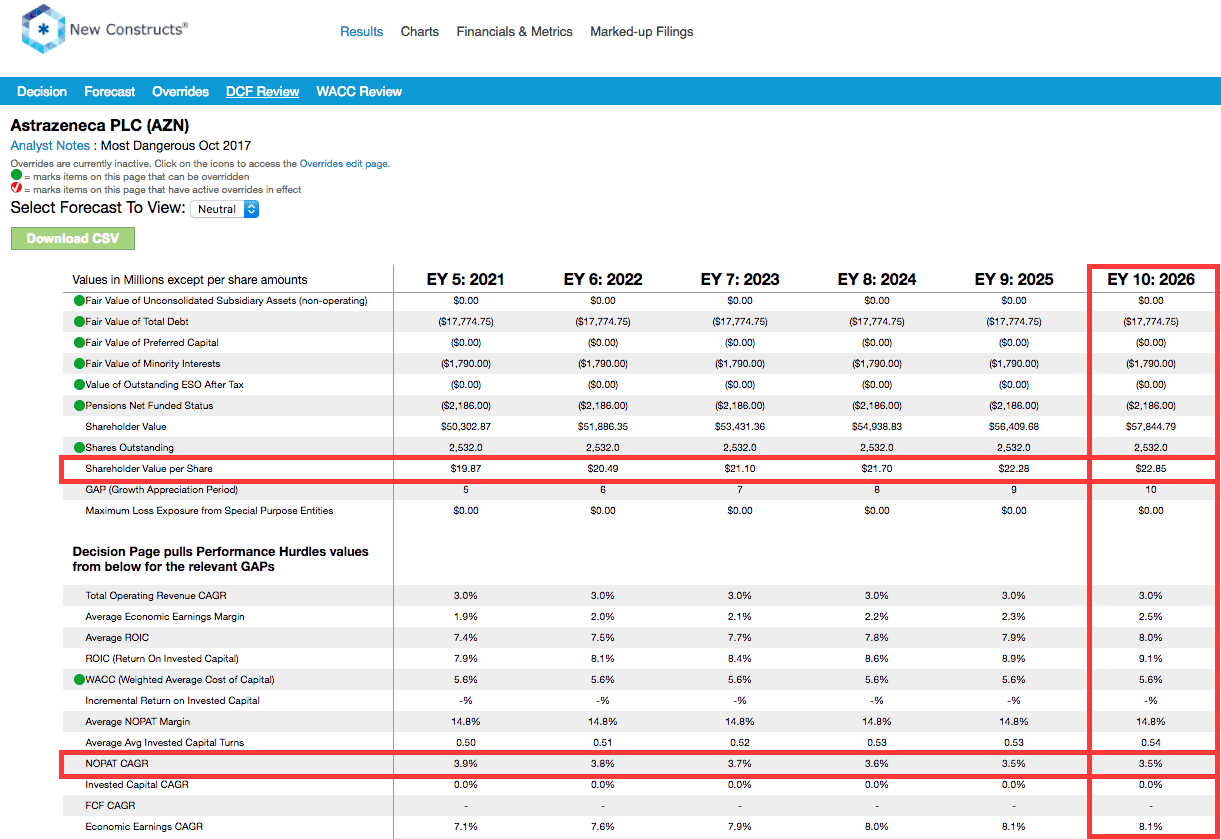

To justify its current price of $35/share, AZN must immediately improve NOPAT margins to the ten-year average of 20% (compared to 12% TTM), grow revenue 3% compounded annually, and grow NOPAT 7% compounded annually over the next decade. Even if AZN improves NOPAT margin to 15%, grows revenue by 3% compounded annually, and grows NOPAT by 4% compounded annually over the next decade, the stock is worth only $23/share today – 34% downside.

{kind=link}

{kind=link}

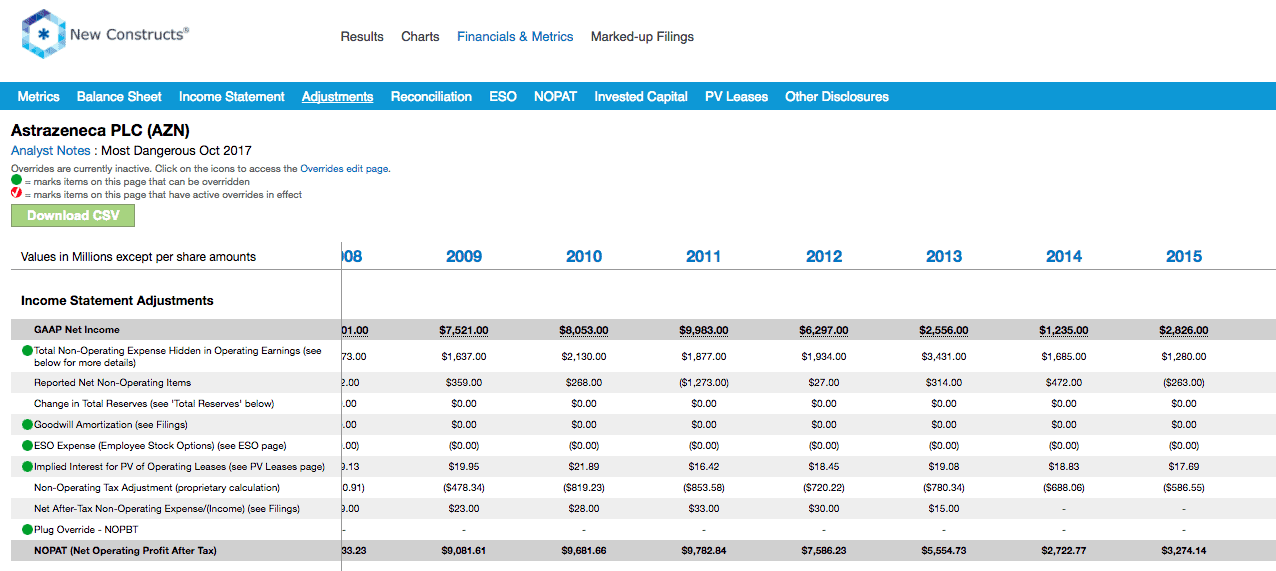

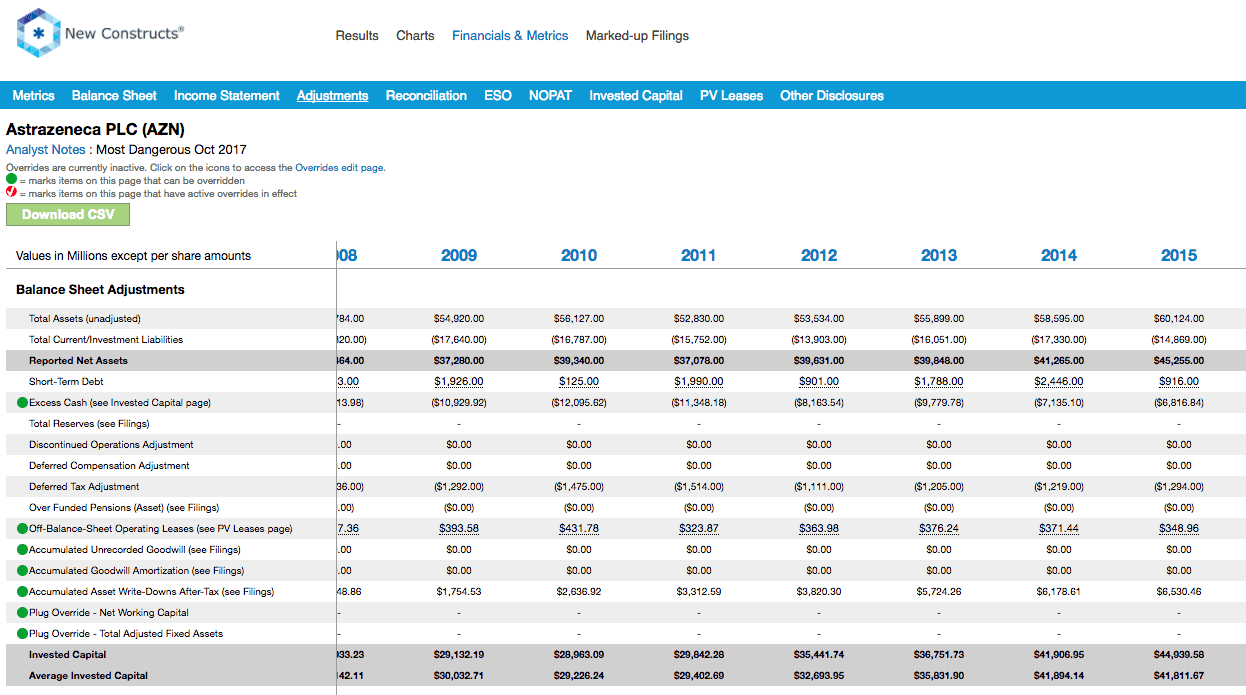

Impacts of Footnotes Adjustments and Forensic Accounting[1]

Our Robo-Analyst technology enables us to perform forensic accounting with scale and provide the research needed to fulfill fiduciary duties. In order to derive the true recurring cash flows, an accurate invested capital, and an accurate shareholder value, we made the following adjustments to AstraZeneca PLC’s 2016 10-K:

Income Statement: we made $5.9 billion of adjustments, with a net effect of removing $154 million in non-operating income (6% revenue). We removed $3.0 billion in non-operating income and $2.9 billion in non-operating expenses. You can see all the adjustments made to AZN’s income statement here.

{kind=link}

Balance Sheet: we made $17.5 billion of adjustments to calculate invested capital with a net increase of $1.2 billion. One of the largest adjustments was $6.7 billion due to asset write-downs. This adjustment represented 14% of reported net assets. You can see all the adjustments made to AZN’s balance sheet here.

{kind=link}

Valuation: we made $28 billion of adjustments with a net effect of decreasing shareholder value by $1.2 billion. Aside from adjusted total debt of $18 billion, the largest adjustment to shareholder value was $2.8 billion in deferred tax liabilities. This adjustment represents 3% of AZN’s market cap.

This article originally published on October 12, 2017.

Disclosure: David Trainer, Kyle Guske II, and Kenneth James receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

Click here to download a PDF of this report.

[1] Ernst & Young’s recent white paper, “Getting ROIC Right”, proves the superiority of our research and analytics.