Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life and Marketwatch.com

Is the market finally noticing the mounting challenges facing Netflix and the excessive risk in its stock? Based on recent price movement, the answer would be no. However, with Macquarie Capital recently downgrading Netflix to underperform, and others questioning NFLX’s valuation, the issues, which we highlighted long ago, that face the company are slowly coming to light. Those issues include: unprofitable international expansion, dwindling competitive advantages, and a sky-high stock valuation. For a long time, the market has largely ignored these concerns. When investors really finally accept the truth about this company and stock, Netflix (NFLX: $97/share) could be in for a big sell-off.

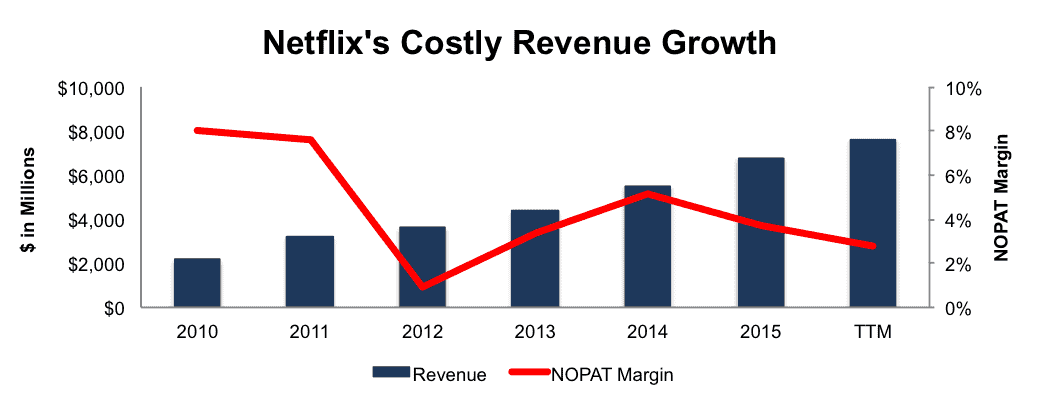

Issue #1: Declining Margins Equal Growing Losses

When we first placed Netflix in the Danger Zone in November 2013, we noted that the company’s margins were facing pressure from the decline in DVD memberships (most profitable segment) and the exorbitant costs of expanding internationally. This trend continues today as Netflix’s after-tax profit (NOPAT) margins have declined from 8% in 2010 to 3% over the last twelve months (TTM), per Figure 1. The deterioration in margins can be largely attributed to Netflix’s unprofitable international expansion, a concern we raised in May 2014. In fact, Netflix’s international streaming segment has recorded a negative contribution margin for the past 18 quarters. Worst of all, Netflix’s economic earnings, the true cash flows of the business, have declined from $137 million in 2010 to -$357 million TTM. Netflix’s profits are in a strong downward trend.

Figure 1: NOPAT Margin Clearly Trending Lower

Sources: New Constructs, LLC and company filings.

Sources: New Constructs, LLC and company filings.

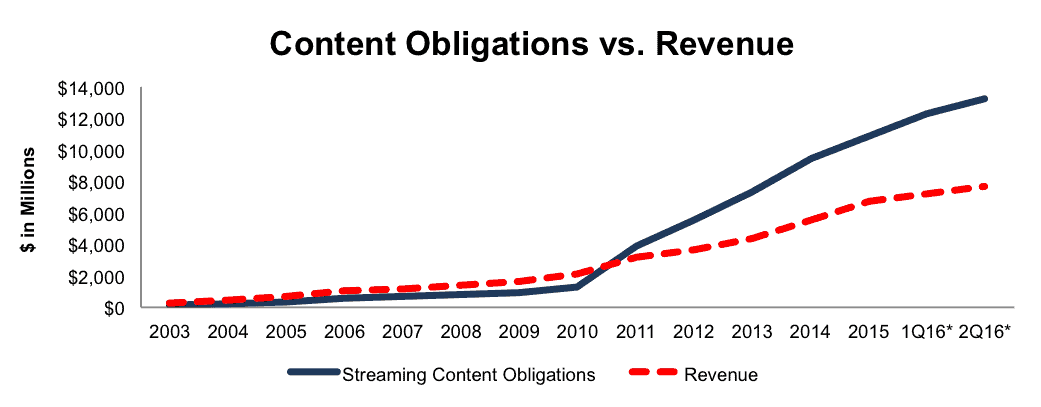

Issue #2: Unsustainable Content Costs

In April 2014 we pointed out the alarming rate at which Netflix’s streaming content obligations were growing. As more and more competition entered the market, licensing content became a larger and larger cost, as more firms were bidding up prices. Per Figure 2, from 2010-2015 Netflix’s streaming content costs have grown by 53% compounded annually while revenue has grown 26% compounded annually. As of 2Q16, streaming content obligations totaled $13.2 billion.

Figure 2: Content Obligation Growth Outpaces Revenue

*Revenue from the trailing twelve months

*Revenue from the trailing twelve months

Sources: New Constructs, LLC and company filings

More troubling than just the streaming content costs is the fact that Netflix’s expansion into original content has the firm operating more like a traditional TV network and less like the video streaming provider it once was. Netflix cannot afford to maintain a massive content library and create costly original programming for much longer, which brings us to our next issue: big time cash burn.

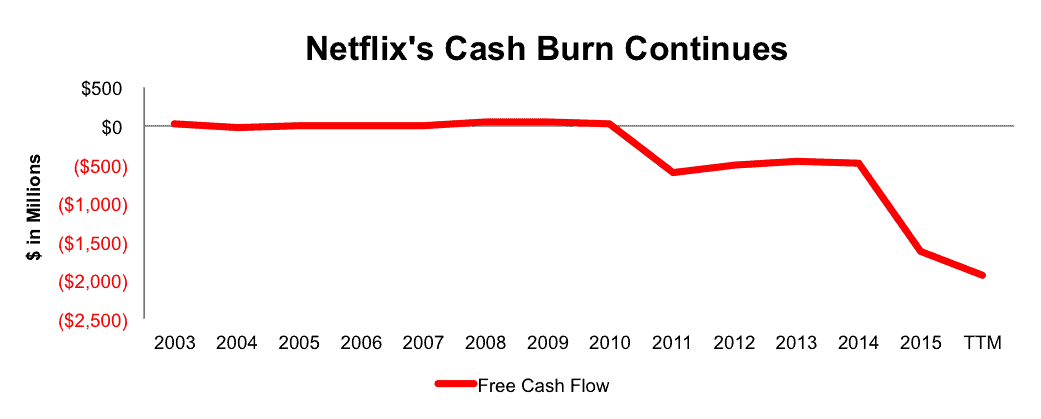

Issue # 3: Large Cash Burn

The last year Netflix generated positive free cash flow (FCF), was 2010, which happens to coincide with the year it began significantly increasing its content library, per Figure 2 above. Since then, Netflix has burned through cumulative $3.6 billion in cash, per Figure 3, and the cash burn is only accelerating. In 2015, NFLX’s FCF sat at -$1.6 billion and over the last twelve months FCF has worsened, to -$1.9 billion.

Note that Wall Street loves the big cash burn because it means it makes big money when Netflix raises more capital. Consequently, you should not be surprised to see positive ratings on NFLX from Wall Street analysts.

Figure 3: Netflix’s TTM Free Cash Flow Is -$1.9 Billion

Sources: New Constructs, LLC and company filings.

Sources: New Constructs, LLC and company filings.

For astute investors, the focus should be on the fact that original content has not only been costly, but also it has led to price increases that make Netflix less attractive when consumers choose a streaming service, which brings us to issue #4.

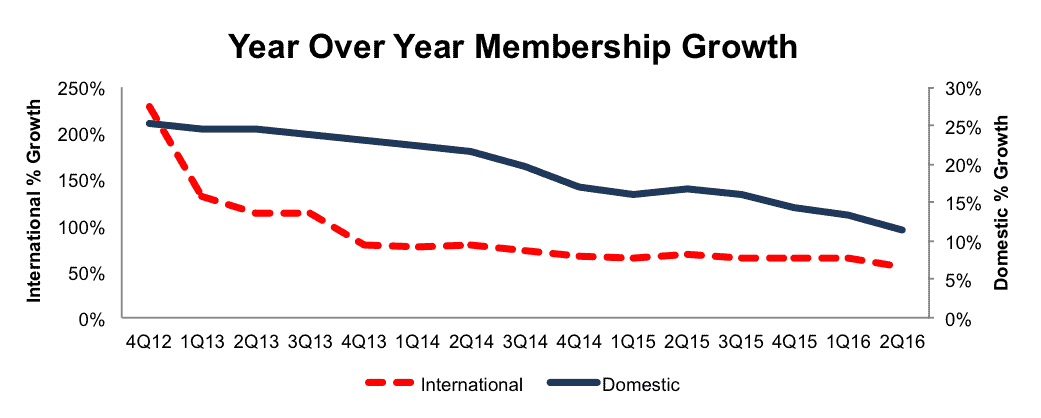

Issue #4: Membership Growth Continues To Slow

When Netflix reported its 2Q16 results, many investors (and Netflix management) were left disappointed by the company’s subscriber growth. However, market saturation and a slowing down in membership growth is nothing new, as it has been a concern of ours since October 2014. As can be seen in Figure 4, the year-over-year (YoY) growth in memberships, both domestic and international is in a long-term downtrend. While international members grew 55% YoY in 2Q16, that is down from 68% YoY in 2Q15, and 78% YoY in 2Q14. Similarly, domestic members grew 11% YoY in 2Q16, down from 17% YoY in 2Q15 and 22% YoY in 2Q14.

Figure 4: Netflix’s Membership Growth Rates

Sources: New Constructs, LLC and company filings.

Sources: New Constructs, LLC and company filings.

The root cause of the slowing memberships at least in 2Q16, according to Netflix management, is not due to competition, but rather the media coverage of Netflix’s un-grandfathering of prices making consumers believe Netflix was raising prices again. Regardless, there’s no denying that competition and pricing are inextricably linked, and when combined, could provide the biggest roadblock to Netflix ever achieving the success and profits implied by its current valuation.

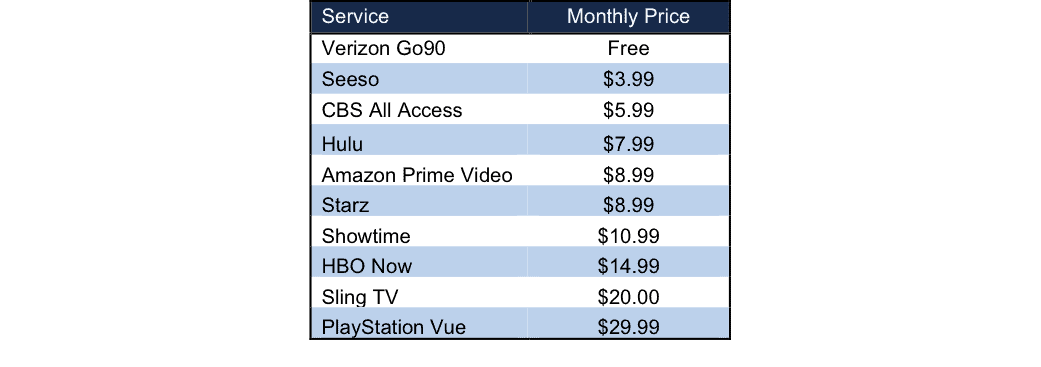

Issue #5: Streaming Video Has Become A Commodity

When we first covered Netflix, back in 2013, we mainly focused on two competitors in the streaming video segment, Amazon Prime and Hulu. Since then, the streaming video market has drastically changed, and Netflix has lost much of the competitive advantage it once held. Today, the market is highly fragmented, with many firms competing for consumers’ business. Figure 5 lists just some of Netflix’s biggest competitors along with their monthly prices.

Figure 5: Netflix’s Numerous Competitors

Sources: New Constructs, LLC and company filings.

Sources: New Constructs, LLC and company filings.

This list doesn’t include newer services such as YouTube Red, the potential for Facebook Live, or even Twitter beginning to stream live NFL, MLB, and NHL games. Not to mention, services like Amazon Video allow for subscription add-ons, such as Showtime or Starz. Hulu has announced plans to offer users the ability to stream live programming, including sports and news in 2017. It’s also worth noting that Hulu is part-owned by major cable providers Disney (DIS), Twenty First Century Fox (FOXA), Comcast (CMCSA), and Time Warner (TWX), which means Hulu has major backing and, potentially, access to a lot of high quality original content.

Most importantly, though, the increase in competition leaves limited pricing power, not only at Netflix, but also across the market. With so many video delivery platforms, the service has become commoditized, with new features or original content the only differentiator. Unfortunately, such original content has not enabled Netflix to increase pricing, as showcased by its previous struggles to raise price.

- When Netflix hiked prices in 2011, the service lost nearly 1 million subscribers.

- In May 2014, Netflix raised prices for new customers and 3Q14 results revealed subscriber additions came in well below expectations.

- In 2Q16, when “grandfathered” customers saw their monthly prices rise, Netflix’s subscriber growth once again fell well short of expectations.

It’s clear that the price of Netflix has a large impact on its membership growth, a trend exacerbated by the increase in competition and commoditization of the offering. If Netflix tries to raise prices, consumers have more options than ever to take their business. If Netflix cannot dramatically raise its prices, the stock is dramatically overvalued.

Issue #6: NFLX Valuation Is Unrealistically Optimistic

We’ve previously called Netflix one of the most overvalued stocks in the market and investors’ willingness to overlook the deterioration of the firm’s fundamentals means that statement remains true today. Even if Netflix maintains TTM pre-tax margins (3.6%) and can grow NOPAT by 22% compounded annually for the next decade, the stock is worth only $24/share today – a 75% downside. To further illustrate just how overvalued NFLX remains, we quantify three scenarios for the improvement in margins, subscribers, and/or revenue that is required to justify NFLX’s current price of $97/share. For reference, Netflix currently has just over 83 million members and earned a 3.6% pre-tax margin over the last twelve months.

Scenario 1: If we assume that Netflix maintains its current price structure, its current pre-tax margins (3.6% TTM), and can grow revenue by consensus estimates in EY1 & EY2 and by 26% thereafter (average of last five years), the company must grow NOPAT by 24% compounded annually for the next 19 years to justify its current price of $97/share. In this scenario, Netflix would generate of $534 billion in revenue (19 years from now), which at current subscription prices implies the company’s user base will be 4.5 billion. The world population is estimated to be 7.4 billion.

Scenario 2: If we assume that Netflix adopts a strategy that improves margins by doubling prices but at the expense of revenue growth, the current expectations are still overly optimistic. If Netflix can increase pre-tax margins to 13.2% (highest in company history, 2010), and grow revenue by 13% (half the five year average), the company must grow NOPAT by 17% compounded annually for 29 years to justify its current price. In this scenario, Netflix would be generating over $228 billion in revenue 29 years from now, which at double current subscription prices implies the company’s user base will be 954 million.

Scenario 3: Even if we assume Netflix is able to drastically improve margins through price increases without any impact on revenue growth, shares are still overvalued. If Netflix can achieve 13.2% pre-tax margins and grow revenue by consensus estimates in EY1 & EY2 and by 26% thereafter, the company must grow NOPAT by 39% compounded annually for the next nine years to justify the current price. In this scenario, Netflix would generate over $67 billion in revenue 9 years from now, which at double current subscription prices implies the company’s user base will be 282 million.

Each of these scenarios also assumes Netflix is able to grow revenue and NOPAT without spending on working capital or fixed assets, an assumption that is unlikely, but allows us to create a very optimistic scenario. For reference, NFLX’s invested capital has grown on average $926 million (14% of 2015 revenue) per year over the last five years. No matter which way you look at this stock’s valuation, NFLX is priced beyond perfection. Given the litany of challenges facing the company, the downside risk to this stock looms large.

Figure 6 summarizes three potential scenarios for the profit growth needed to justify $97/share.

Figure 6: Valuation Scenarios for NFLX

Sources: New Constructs, LLC and company filings.

This article originally published here on September 19, 2016.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, sector, style, or theme.

Scottrade clients get a Free Gold Membership ($588/yr value). Login or open your Scottrade account & find us under Quotes & Research/Investor Tools.