Recap from October Picks

Our Most Attractive Stocks (-4.3%) underperformed the S&P 500 (-2.2%) last month. Most Attractive Large Cap stock Juniper Networks (JNPR) gained 4% and Most Attractive Small Cap stock Heartland Financial U.S.A. (HTLF) was up 3%. Overall, 19 out of the 40 Most Attractive stocks outperformed the S&P 500 in October.

Our Most Dangerous Stocks (-4.7%) outperformed the S&P 500 (-2.2%) last month. Most Dangerous Large Cap stock Penske Automotive (PAG) fell by 12% and Most Dangerous Small Cap Stock The Providence Service Group (PRSC) fell by 21%. Overall, 26 out of the 40 Most Dangerous stocks outperformed the S&P 500 in October.

The successes of the Most Attractive and Most Dangerous stocks highlight the value of our forensic accounting as featured in Barron’s. Being a true value investor is an increasingly difficult, if not impossible, task considering the amount of data contained in the ever-longer annual reports. By analyzing key details in these SEC filings, our research protects investors’ portfolios and allows our clients to execute value-investing strategies with more confidence and integrity.

14 new stocks make our Most Attractive list this month and 17 new stocks fall onto the Most Dangerous list this month. November’s Most Attractive and Most Dangerous stocks were made available to members on November 3, 2016.

Our Most Attractive stocks have high and rising returns on invested capital (ROIC) and low price to economic book value ratios. Most Dangerous stocks have misleading earnings and long growth appreciation periods implied by their market valuations.

Most Attractive Stocks Feature for November: Winmark Corporation (WINA: $105/share)

Winmark Corp (WINA), franchisor of retail stores including Platos Closet and Play It Again Sports, is one of the additions to our Most Attractive stocks for November.

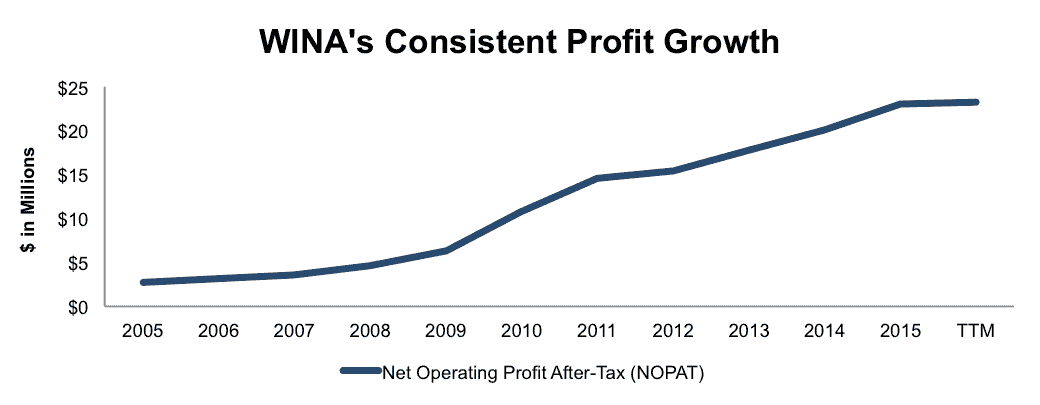

Over the past decade, Winmark Corp has grown after-tax profit (NOPAT) by 24% compounded annually, per Figure 1. The company’s NOPAT margin has improved from 10% in 2005 to 35% over the last twelve months (TTM) while its return on invested capital (ROIC) has improved from 14% in 2005 to a top-quintile 42% TTM.

Figure 1: Profit Growth Since 2005

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

Impacts of Footnotes Adjustments and Forensic Accounting

In order to derive the true recurring cash flows, an accurate invested capital, and an accurate shareholder value, we made the following adjustments to Winmark’s 2015 10-K:

Income Statement: we made $3 million of adjustments, with a net effect of removing $1 million in non-operating expenses (1% of revenue). We removed $1 million in non-operating income and $2 million in non-operating expenses. You can see all the adjustments made to WINA’s income statement here.

Balance Sheet: we made $21 million of adjustments to calculate invested capital with a net increase of $21 million. One of the largest adjustments was $13 million due to asset write-downs. This adjustment represented 32% of reported net assets. You can see all the adjustments made to WINA’s balance sheet here.

Valuation: we made $77 million of adjustments with a net effect of decreasing shareholder value by $76 million. One of the notable adjustments was the removal of $22 million due to outstanding employee stock options. This adjustment represents 5% of Winmark’s market cap. Despite the impact of these adjustments, WINA remains undervalued.

Despite Share Increase, WINA Remains Undervalued

The market has rewarded Winmark for its consistent improvement to the business’ fundamentals and shares are up over 100% over the past five years. In spite of this increase, shares remain undervalued. At its current price of $105/share, WINA has a price-to-economic-book value (PEBV) ratio of 1.1. This ratio means the market expects WINA’s NOPAT to grow by only 10% of the remainder of its corporate life. Such an expectation seems awfully low for a company that has grown profits by over 20% compounded annually for the past decade. If Winmark can maintain 2015 margins of 33% (compared to 35% TTM) and grow NOPAT by just 7% compounded annually for the next decade, the stock is worth $182/share today – a 73% upside.

Most Dangerous Stocks Feature: Mack-Cali Realty (CLI: $25/share)

Mack-Cali Realty (CLI), real estate firm involved in the leasing, acquisition, development, and construction of real estate properties, is one of the additions to our Most Dangerous stocks for November.

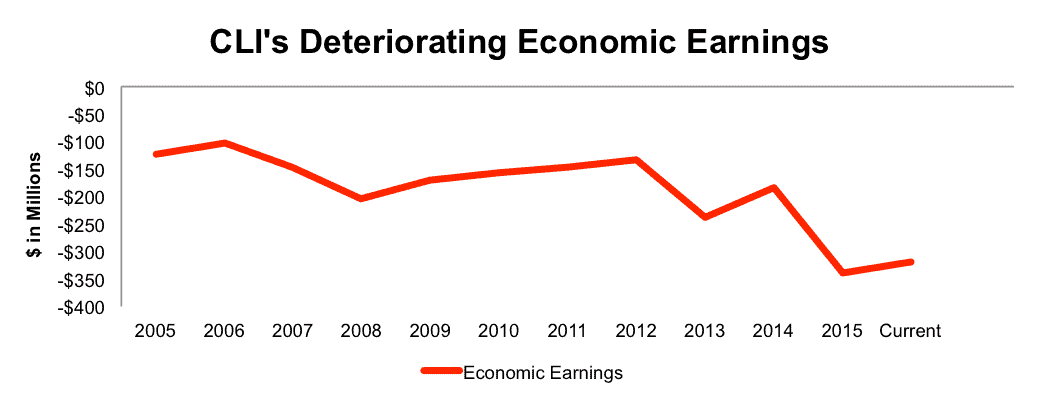

CLI’s economic earnings, the true cash flows of the business, have declined from an already -$124 million in 2005 to -$318 million TTM, per Figure 2. The company’s ROIC has fallen from 6% in 2005 to a bottom-quintile 0% TTM and its NOPAT margin has fallen from 37% to -3% over the same time.

Figure 2: 10 Year Decline In Economic Earnings

Sources: New Constructs, LLC and company filings

Impacts of Footnotes Adjustments and Forensic Accounting

In order to derive the true recurring cash flows, an accurate invested capital, and an accurate shareholder value, we made the following adjustments to Mack-Cali’s 2015 10-K:

Income Statement: we made $130 million of adjustments, with a net effect of removing $83 million in non-operating expense (14% of revenue). We removed $24 million in non-operating income and $106 million in non-operating expenses. You can see all the adjustments made to CLI’s income statement here.

Balance Sheet: we made $162 million of adjustments to calculate invested capital with a net increase of $35 million. One of the largest adjustments was $56 million due to midyear acquisitions. This adjustment represented 1% of reported net assets. You can see all the adjustments made to CLI’s balance sheet here.

Valuation: we made $2.7 billion of adjustments with a net effect of decreasing shareholder value by $2.7 billion. There were no adjustments that increased shareholder value. Apart from total debt, which includes off-balance sheet operating leases, a notable adjustment was $199 million in minority interests. This adjustment represents 9% of Mack-Cali’s market cap.

Fundamental Deterioration Leaves Shares Overvalued

Despite the deterioration in economic earnings, CLI is up over 25% over the past two years. Such a large increase in share price without a subsequent increase in profitability makes CLI significantly overvalued. To justify its current price of $26/share CLI must immediately achieve 17% NOPAT margins (average of last five years, compared to -3% TTM) and grow revenue by 15% compounded annually for the next 11 years.

Even if CLI can achieve a 17% NOPAT margin and grow revenue by 10% compounded annually (well above the 4% consensus for 2016 & 2017) for the next decade, the stock is only worth $4/share today – an 84% downside. This scenario also assumes CLI can grow NOPAT/free cash flow without spending on working capital or fixed assets. This assumption is unlikely but allows us to create a very optimistic scenario. For reference, CLI’s invested capital has grown on average $14 million (2% of 2015 revenue) per year over the past decade.

This article originally published here on November 8, 2016.

Disclosure: David Trainer, Kyle Guske II, and Kyle Martone receive no compensation to write about any specific stock, style, or theme.

Click here to download a PDF of this report.

Scottrade clients get a Free Gold Membership ($588/yr value) as well as 50% discounts and up to 20 free trades ($140 value) for signing up to Platinum, Pro or Unlimited memberships. Login or open your Scottrade account & find us under Quotes & Research/Investor Tools.