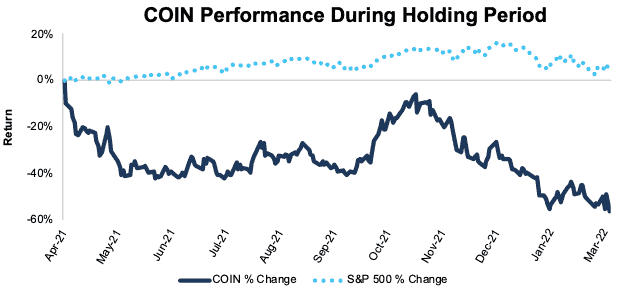

We first put Coinbase (COIN: $178/share) in the Danger Zone in March 2021 prior to its IPO. Since then, the stock is down 56% compared to a 5% gain for the S&P 500. Though the company set records across many of its chosen key performance metrics in 2021, sustained success looks unlikely. See our most recent report from May 2021 on Coinbase here.

We leverage more reliable fundamental data[1], shown to provide a new source of alpha, with qualitative research to pick this Danger Zone idea.

Coinbase’s Stock Could Fall Further Based On:

- difficult comps in 2022 given record crypto trading in 2021

- increasing reliance on transaction fees despite introducing new products/services

- guidance for 2022 implies a significant cut in profitability and very little clarity on user growth

- current valuation of the stock implies Coinbase will be larger than Charles Schwab – anything less, and the stock could have 35%+ downside

Figure 1: Danger Zone Outperformance of 61%: From 4/15/21 Through 3/4/22

Sources: New Constructs, LLC

What’s Working

Record crypto trading: in 2021, the market cap of all cryptocurrencies reached $2.3 trillion, up from $782 billion at the end of 2020. Bitcoin and Ethereum reached all-time high prices and drove Coinbase’s 2021:

- monthly transacting users (MTUs) up 4x over 2020

- trading volume up nearly 9x over 2020

- assets on platform up 3x over 2020

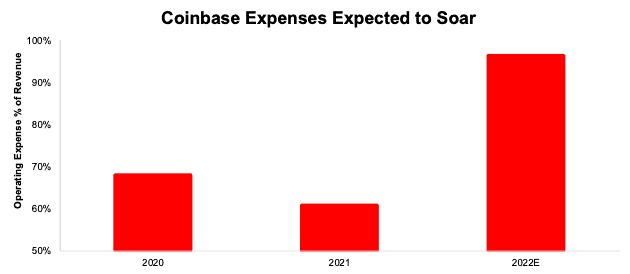

Operating expenses kept in check: often as small companies rapidly scale, they have trouble keeping expenses under control, but not Coinbase. Coinbase’s 2021 results revealed that operating expenses as a percent of revenue fell from 68% in 2020 to 61% in 2021, which helped drive the company’s net operating profit after-tax (NOPAT) margin from 25% to 32% over the same time. However, such cost control will not continue into 2022, as we’ll detail below.

What’s Not Working

Coinbase is growing more reliant upon transaction fees: In 2020, 86% of Coinbase’s revenue stemmed from its transaction revenue. Despite introducing new service-fee-generating products, Coinbase’s transaction revenue increased to 87% of revenue in 2021. As we’ve noted in our prior reports, transaction-based revenue will be more difficult to maintain moving forward, as competitors enter the market and drive transaction fees to zero. Not surprisingly, the amount of money Coinbase collects per transaction fell in 2021.

In 2021, Coinbase collected 0.41% of every transaction as revenue ($6.8 billion in transaction revenue on $1.7 trillion in trading volume). In 2020, Coinbase collected 0.57% of every transaction as revenue ($1.1 billion in transaction revenue on $193 billion in trading volume). We expect Coinbase to collect less and less revenue from each transaction as the market grows more mature.

2021 growth is not sustainable: 2021’s record performance, which was largely due to the rapid rise in crypto value and market cap, is not sustainable. Year-over-year (YoY) comps for Coinbase will likely be poor in 2022. This expectation is not just ours, but management’s as well. In its 4Q21 earnings call, management noted they expect both trading volume and retail MTU will be lower in 1Q22 compared to 4Q21.

Full-year 2022 guidance looks even worse than just lower 1Q22 volume and MTUs. For instance, Coinbase expects 2022 average transaction revenue per user (ATRPU) to be “pre-2021” levels, which while vague, certainly implies a decline. 2021 ATRPU was a record $64, while 2020 ATRPU was $45, and 2019 ATRPU was $34.

On the user front, management notes that it is highly uncertain of how many users Coinbase will have in 2022. The company guided for anywhere from 5-15 million average retail MTUs, which implies either a YoY decline of 40% at the low end or a YoY increase of 79% at the high end. The midpoint would imply 19% YoY growth in average retail MTUs. Such a wide range suggests management is not very confident in MTU growth.

Investors should also expect Coinbase’s profitability to nearly disappear in 2022. Using management’s guidance for operating expenses, including a more than doubling of technology & development and general & administrative expenses, we find that Coinbase’s 2022 expected operating expenses will rise to 96% of 2022 revenue (based on consensus estimate). Figure 2 illustrates the rapid increase expected in Coinbase’s operating expenses, which will drive down profit margins.

Figure 2: Coinbase’s Operating Expenses: 2020 through 2022E

Sources: New Constructs, LLC and company filings

Coinbase Is Still Priced to Be the Largest Exchange in the World

Despite COIN falling 56% since the opening price on its IPO date, the stock is still significantly overvalued. Below, we use our reverse discounted cash flow (DCF) model to illustrate the lofty expectations for future cash flows implied by Coinbase’s current valuation.

To justify its current price of $178/share, Coinbase must:

- maintain a 21% NOPAT margin (equal to Nasdaq’s [NDAQ] 2021 margin and despite expected drop in 2022) and

- grow revenue by 15% compounded annually through 2028 (compared to consensus estimates of 3% CAGR from 2021-2024)

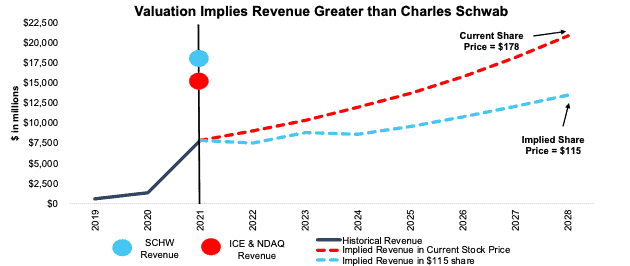

In this scenario, Coinbase would earn $21 billion in revenue by 2028, which is a 39% greater than Intercontinental Exchange and Nasdaq’s combined 2021 revenue, 10% greater than Charles Schwab’s (SCHW) 2021 revenue, and 42% of the TTM revenue of the 10 largest Financial & Commodity Market Operators[2].

If Coinbase maintained transaction revenue at 87% of revenue and fees at 0.41% of trading volume (as outlined above), this scenario implies that trading volume on Coinbase’s platform would be $4.4 trillion in 2028, which would equal 31% of the total cryptocurrency trading volume in 2021. For reference, Coinbase’s trading volume was 12% of cryptocurrency trading volume in 2021.

35%+ Downside if Consensus is Right

We review an additional DCF scenario to highlight the downside risk should Coinbase’s profitability align with traditional exchanges and revenue grows at consensus rates.

If we assume Coinbase’s:

- NOPAT margin falls to 21% (equal to Nasdaq’s 2021 margin),

- revenue grows at consensus rates in 2022, 2023, and 2024 (-4%, 17%, and -3%[3]), and

- revenue grows 12% each year from 2025-2028, then

COIN is worth just $115/share today – a 35% downside. Should 2022’s expected drop in profitability last longer than one year, or cryptocurrency see a ceiling on trading volumes, the downside is even larger.

Figure 3 compares Coinbase’s implied future revenue in this scenario to its historical revenue as well as Charles Schwab’s 2021 revenue and the combined 2021 revenues of Intercontinental Exchange and Nasdaq.

Figure 3: Coinbase’s Historical and Implied Revenue: DCF Valuation Scenarios

Sources: New Constructs, LLC and company filings

Each of the above scenarios also assumes Coinbase’s invested capital equals 10% of revenue in each year. This growth in invested capital is under half the change in invested capital as a percent of revenue in both 2020 and 2021. If we assume Coinbase’s invested capital increases at a similar rate to 2020 and 2021, the downside risk is even larger.

Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

This article originally published on March 7, 2022.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, sector, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Our research utilizes our Core Earnings, a more reliable measure of profits, as proven in Core Earnings: New Data & Evidence, written by professors at Harvard Business School (HBS) & MIT Sloan and published in The Journal of Financial Economics.

[2] Companies in this group include Cboe Global Markets (CBOE), CME Group (CME), Deutsche Boerse AG (DBOEF), Fidelity National Information Services (FIS), Interactive Brokers Group (IBKR), Intercontinental Exchange (ICE), MarketAxess Holdings (MKTX), Nasdaq Inc. (NDAQ), Tradeweb Markets (TW), and Virtu Financial (VIRT).

[3] Consensus estimates based on twenty analyst estimates in 2022 and 2023 and eight analyst estimates in 2024.